A Look At Rollins (ROL) Valuation After Saela Outperformance And Strong Q3 2025 Metrics

Rollins, Inc. ROL | 53.93 | +0.82% |

Why Rollins (ROL) is Back in Focus After the Saela Deal

Rollins (ROL) is drawing fresh attention after commentary that its Saela Holdings acquisition outperformed expectations, with Q3 2025 revenue and free cash flow showing year-over-year improvement while the stock trades at a premium P/E.

That backdrop helps explain why investors have pushed Rollins’ 90 day share price return to 11.31% and its 1 year total shareholder return to 31.32%. This signals firm momentum rather than fading interest at the current US$63.11 share price.

If this kind of steady compounding appeals to you, it could be worth broadening your search with fast growing stocks with high insider ownership to see what other companies investors with skin in the game are backing.

With Rollins trading close to its analyst price target and carrying a premium P/E, the key question now is whether the Saela boost still leaves upside on the table or if the market is already pricing in future growth.

Most Popular Narrative: 2.2% Undervalued

With Rollins last closing at US$63.11 against a narrative fair value of US$64.53, the current premium P/E takes on extra context for anyone tracking upside.

They point to the company’s non cyclical, essential pest control services as a key driver of earnings stability across macro environments, supporting a premium valuation multiple versus more economically sensitive business services peers.

Curious what justifies paying up for a business services name at this level. The narrative leans on recurring demand, firmer margins, and a richer future earnings multiple. Want to see how those moving parts combine into that fair value line.

Result: Fair Value of $64.53 (UNDERVALUED)

However, there are still pressure points to watch, including higher operating costs from fleet or tariffs, and any slowdown in residential demand that could test these upbeat assumptions.

Another Angle on Rollins’ Valuation

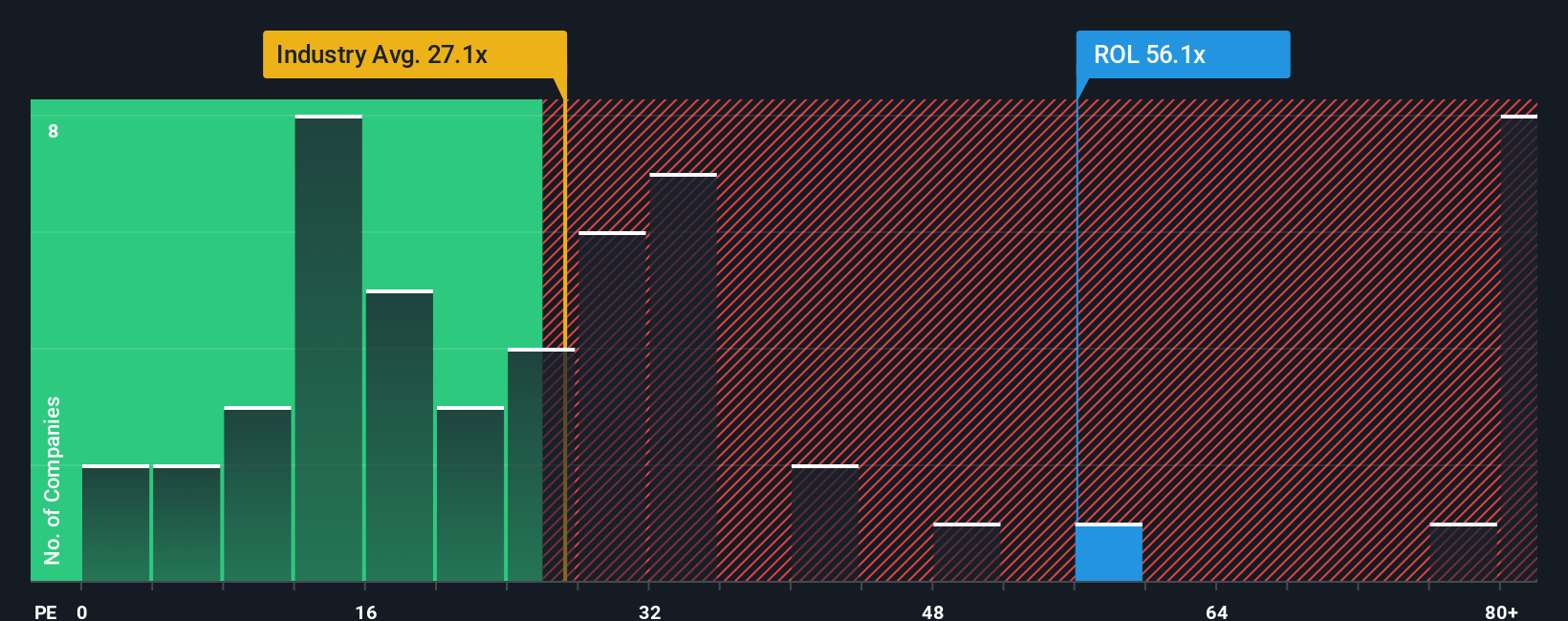

While the narrative fair value suggests Rollins is about 2.2% undervalued, the earnings multiple tells a tougher story. The current P/E of 58.9x stands well above both the Commercial Services industry at 26x and a fair ratio of 28.4x. This points to meaningful valuation risk if sentiment cools.

Build Your Own Rollins Narrative

If this framework does not quite match your view, or you would rather lean on your own research and data, you can build a custom narrative in just a few minutes with Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Rollins.

Looking for more investment ideas?

If Rollins has sharpened your thinking, do not stop here. Broaden your watchlist with focused stock ideas built from live fundamentals and clear, comparable metrics.

- Spot potential value gaps by checking out these 872 undervalued stocks based on cash flows where prices and cash flow expectations can look out of sync.

- Explore opportunities in automation and data tools by scanning these 24 AI penny stocks for companies tied to real-world AI adoption.

- Look for steadier income streams by reviewing these 13 dividend stocks with yields > 3% that already offer yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.