A Look at Schrödinger's Valuation After Major Catalyst Breakthrough and Expanded Copernic Partnership

Schrodinger SDGR | 0.00 |

Schrödinger (SDGR) just cleared a major technical milestone in its partnership with Copernic Catalysts, as their Neptune ammonia synthesis catalyst outperformed competitors in yield. This result could significantly impact the economics and efficiency of industrial-scale ammonia production.

Schrödinger’s recent technical success with Copernic Catalysts comes at a time when the stock’s momentum is showing tentative improvement. After a dip earlier this month, the share price has rebounded and finished at $21.04 with a 2.19% 30-day return and a year-to-date gain of 3.14%. Long-term holders have seen a 16.95% total shareholder return over the past year. However, returns over longer time horizons remain muted, signaling some cautious optimism building around new growth opportunities.

If this breakthrough in industrial innovation has you curious about what’s possible elsewhere, it might be the perfect moment to broaden your investing approach and discover See the full list for free.

With shares still trading at a meaningful discount to analyst targets and ongoing growth in both revenue and major technical achievements on display, is Schrödinger undervalued at current levels, or has the market already factored in these future gains?

Most Popular Narrative: 22.9% Undervalued

Schrödinger’s most widely followed valuation narrative sets its fair value far higher than the current price, suggesting a sizable gap for potential upside. With the last close at $21.04 and a consensus fair value of $27.30, this substantial difference forms the basis of the prevailing narrative among analysts.

Strong pipeline advancement and early clinical success, such as positive Phase I data for SGR-1505, positions the company to secure additional milestone payments, royalties, and out-licensing deals. This creates potential for substantial long-term revenue growth and more predictable future cash flows.

Want to see what powers this bold price target? The narrative hinges on ambitious growth in both revenue and profits, painting a path to profitability that defies current losses. There is more beneath the surface; discover how much future performance is baked into this valuation.

Result: Fair Value of $27.30 (UNDERVALUED)

However, persistent software margin pressures and ongoing volatility in biotech funding could challenge the optimistic outlook on Schrödinger’s valuation narrative.

Another View: Is the Discount Real?

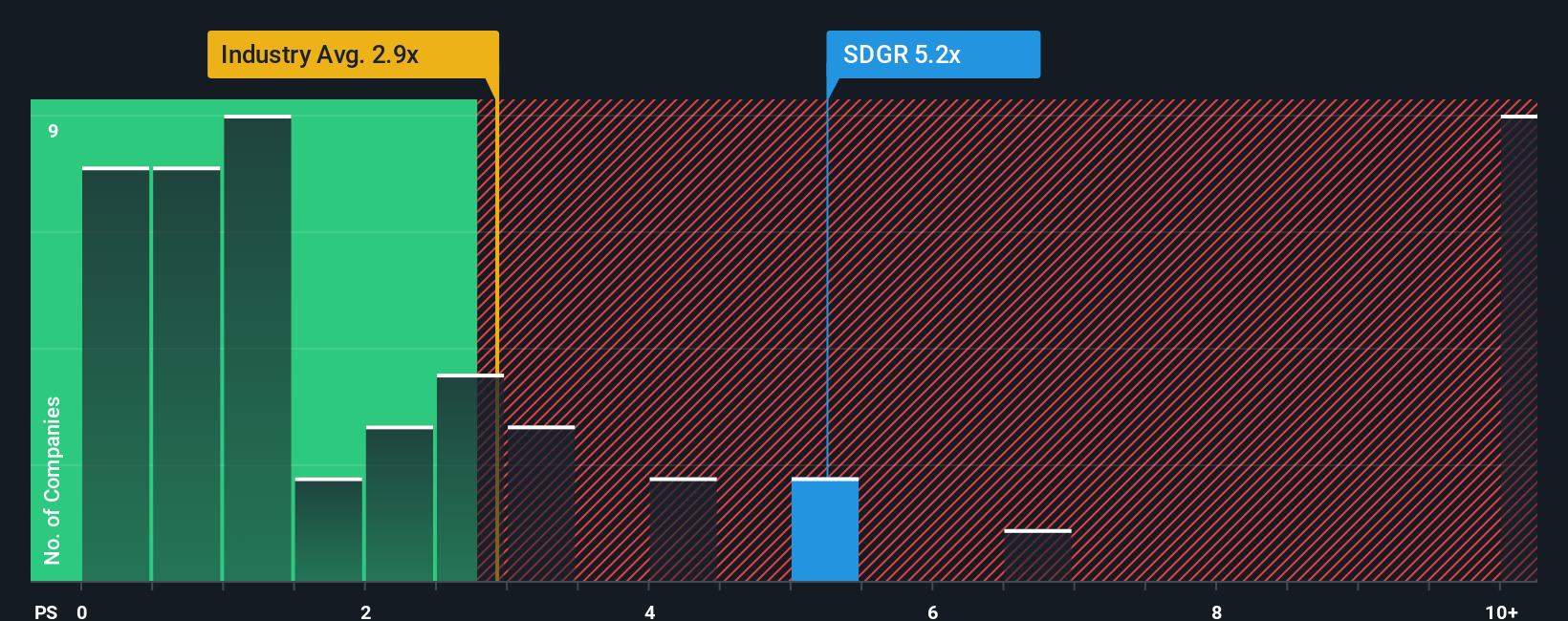

While the consensus points to Schrödinger being undervalued, a look at its price-to-sales ratio raises caution. Shares trade at 6.5 times sales, well above the peer average of 2.4x and the industry average of 3.4x. The market’s fair ratio is estimated at just 2.9x. This suggests investors are paying a steep premium. Could this signal higher risk if growth falls short, or is the company truly set for outsized gains?

Build Your Own Schrödinger Narrative

If you have a different perspective or want to follow your own line of research, you can assemble your own narrative in just a few minutes. Do it your way

A great starting point for your Schrödinger research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

Expand your watchlist and seize tomorrow’s winners. These handpicked stock groups could give you an edge before the next wave of growth takes off.

- Boost your passive income by targeting companies with above-average payouts found in these 22 dividend stocks with yields > 3%.

- Find innovation at the intersection of healthcare and machine learning among these 33 healthcare AI stocks delivering breakthroughs for patient outcomes.

- Position your portfolio for exponential progress with these 28 quantum computing stocks powering the next leap in computing and industry disruption.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.