A Look At Seagate Technology Holdings (STX) Valuation After Earnings Beat And Strong AI Data Center Demand

Seagate Technology STX | 0.00 |

Seagate Technology Holdings (STX) is back in the spotlight after its latest quarterly results topped earnings and revenue estimates, supported by strong data center demand tied to AI and newer storage products.

The stock’s recent rally has been intense, with a 21.0% 1 month share price return and a 131.8% 3 month share price return, alongside a very large 1 year total shareholder return, as investors react to AI driven storage demand and recent earnings beats.

If Seagate’s surge has you rethinking where growth could come from next, this is a good moment to look across AI infrastructure plays via the 47 AI infrastructure stocks.

With Seagate now trading around US$879.80 after a very strong run, the key question is whether recent AI optimism and upgraded growth targets leave room for mispricing or if the market is already baking in the next leg of expansion.

Most Popular Narrative: 14.2% Overvalued

With Seagate closing at $879.80 against a narrative fair value of about $770.43, the most followed storyline in the market is already baking in a lot of optimism, backed by ambitious projections for growth and margins that stretch several years out.

The growing demand for mass capacity storage driven by the cloud CapEx investment cycle and data center build-outs for AI transformation is likely to elevate Seagate's revenue streams. This increased demand aligns with ongoing cloud infrastructure expansion, suggesting positive impacts on earnings.

Curious what kind of revenue curve and margin profile could support that higher fair value, even with a lower future P/E baked in? The narrative leans on aggressive top line expansion, a sharp step up in profitability, and a compression in the multiple that still implies a premium earnings profile. The mix of these assumptions is what really drives the gap between today’s price and that $770.43 figure.

Result: Fair Value of $770.43 (OVERVALUED)

However, trade policy changes and competitive pressure from SSD and QLC NAND could quickly challenge the bullish storage narrative that underpins those fair value assumptions.

Another View: Cash Flows Paint a Different Picture

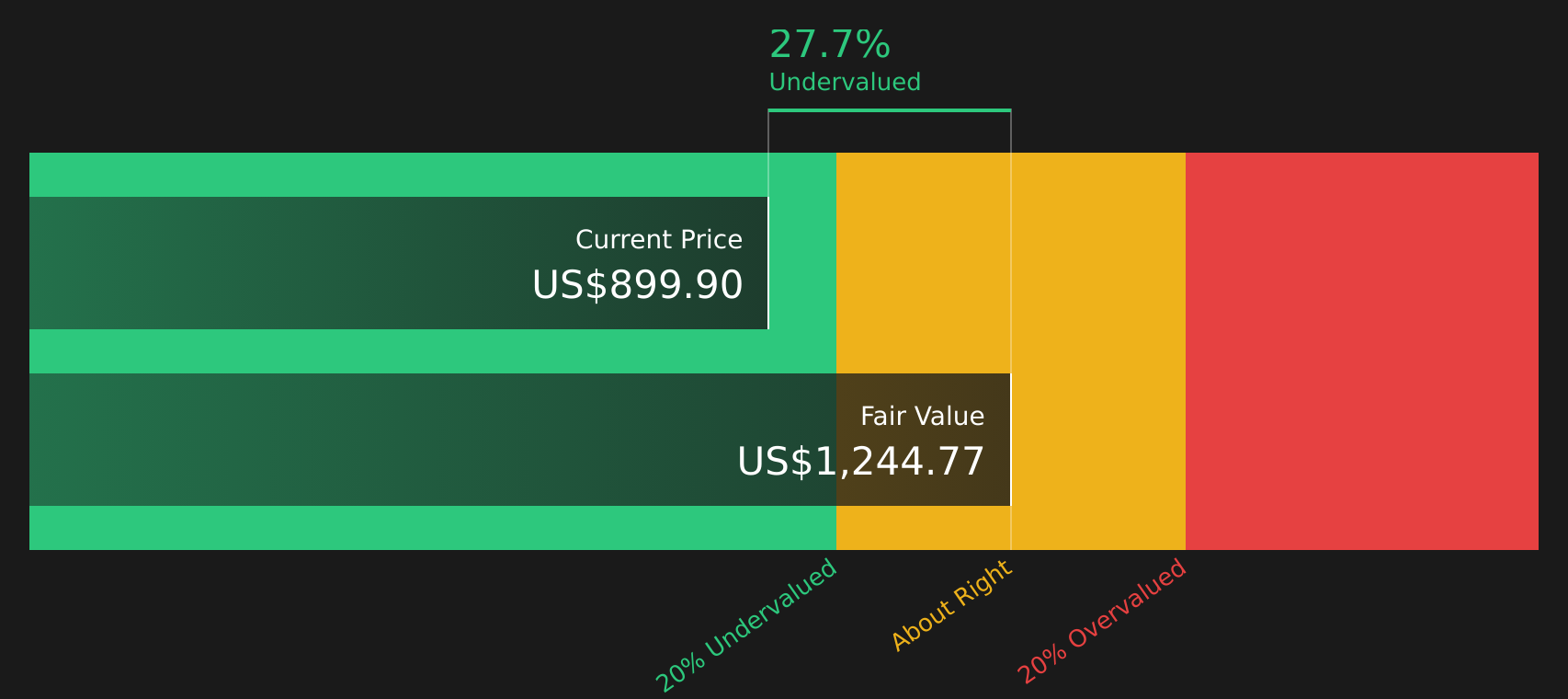

While the analyst narrative flags Seagate as about 14.2% overvalued against a US$770.43 fair value, the SWS DCF model tells a different story, with a future cash flow value of US$1,293.75 versus the current US$879.80 share price. That gap points to a very different risk reward trade off. Which lens do you trust more?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Seagate Technology Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 46 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If the mixed signals in this article leave you on the fence, act while the data is fresh. Weigh both sides by checking the 3 key rewards and 2 important warning signs.

Looking for more investment ideas?

Do not stop with one stock. The screener can surface fresh opportunities that match your style so you are not relying on a single AI infrastructure story.

- Target resilient portfolios by checking out 63 resilient stocks with low risk scores that may help smooth the ride when markets get choppy.

- Hunt for potential bargains by scanning 46 high quality undervalued stocks that combine solid fundamentals with prices that may not reflect their underlying strength.

- Round out your watchlist by exploring the screener containing 22 high quality undiscovered gems before everyone else starts paying attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.