A Look At Seagate Technology Holdings (STX) Valuation After Its Earnings Beat And Raised Guidance

Seagate Technology Holdings PLC STX | 0.00 |

Why Seagate’s latest earnings are back in focus

Seagate Technology Holdings (STX) is back on many investors’ screens after reporting better than expected quarterly earnings and lifting its forward guidance, with demand linked to AI and data center storage playing a central role.

The latest earnings beat and higher guidance come after a sharp re-rating, with the share price up 59.76% over the past month and a very large 1-year total shareholder return, suggesting strong momentum rather than fading enthusiasm.

If you are curious what else is benefiting from AI-related demand, this could be a good moment to scan the market using our screener of 38 AI infrastructure stocks

With Seagate now trading close to, and in some cases above, recent analyst targets after a very large 1 year total shareholder return, the key question is whether today’s price still leaves room for upside or if the market is already fully pricing in future growth.

Most Popular Narrative: 20% Overvalued

At a last close of $579.03 versus a narrative fair value of about $483.07, the current price sits meaningfully above that central estimate, so the key question is which growth and profitability assumptions justify this gap.

The growing demand for mass capacity storage driven by the cloud CapEx investment cycle and data center build outs for AI transformation is likely to elevate Seagate's revenue streams. This increased demand aligns with ongoing cloud infrastructure expansion, suggesting positive impacts on earnings.

Curious what is baked into that fair value? The narrative leans on faster revenue expansion, thicker margins, and a richer earnings base years from now. The exact mix might surprise you.

Result: Fair Value of $483.07 (OVERVALUED)

However, this upbeat AI storage story could be knocked off course if competing SSD or QLC NAND solutions gain share, or if trade policy shifts disrupt customer demand.

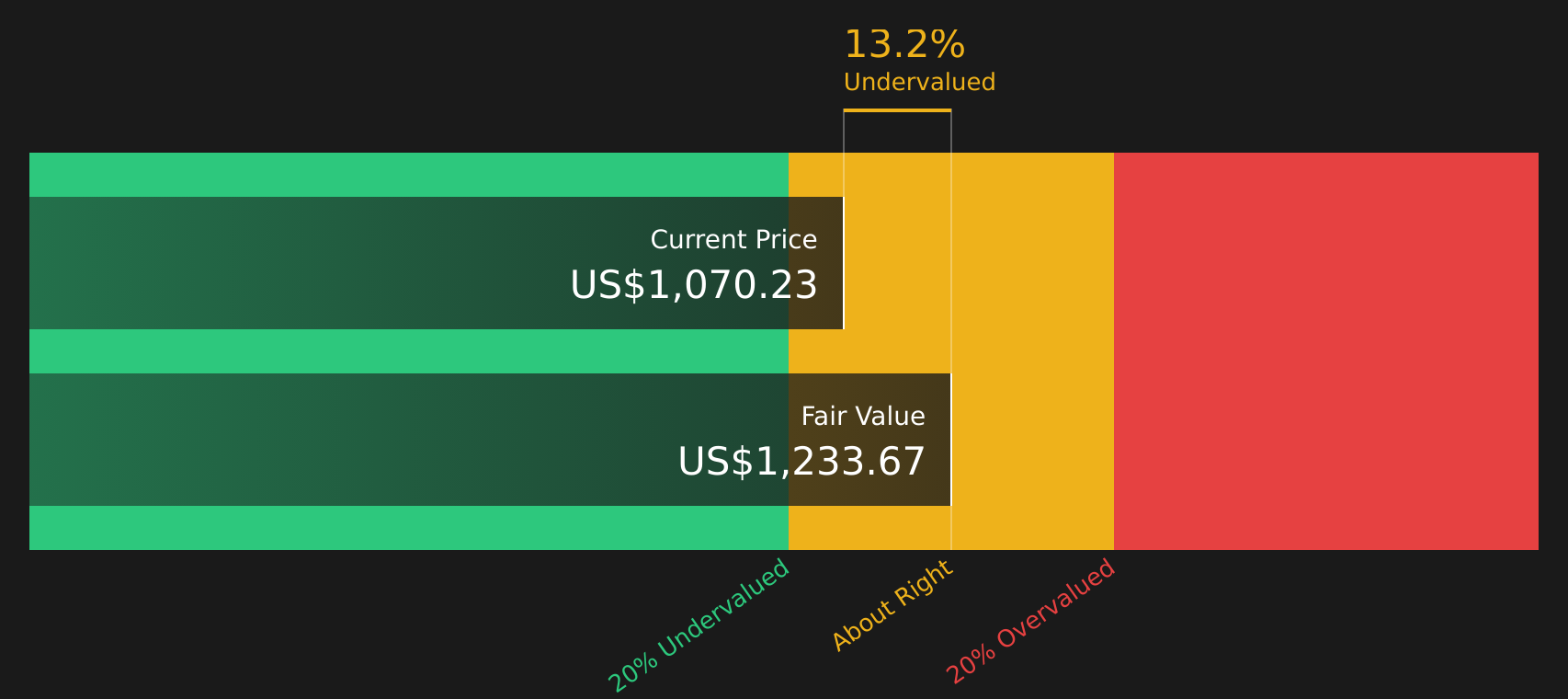

Another View: Cash Flows Paint A Different Picture

The narrative-based fair value suggests Seagate is overvalued at $579.03 versus $483.07, but the SWS DCF model points in the other direction. On that approach, the shares trade about 6.4% below an estimated future cash flow value of $618.90. This raises an obvious question: are earnings multiples or cash flows giving you the more useful anchor here?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Seagate Technology Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 53 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With a story that mixes enthusiasm around AI demand and concern about potential headwinds, it makes sense to review the numbers and narrative yourself, weigh both sides quickly, and use the 3 key rewards and 2 important warning signs to form your own view.

Looking for more investment ideas?

If Seagate has caught your attention, do not stop here. Use the Simply Wall Street Screener to uncover other stocks that could fit your portfolio goals.

- Target dependable cash generators by scanning companies with strong fundamentals using the solid balance sheet and fundamentals stocks screener (44 results).

- Spot potential value opportunities before they are crowded with the help of the 53 high quality undervalued stocks.

- Build a stream of income that works for you by checking out the 14 dividend fortresses.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.