A Look At Shift4 Payments (FOUR) Valuation After Mixed Analyst Moves And Global Blue Integration Progress

Shift4 Payments FOUR | 42.76 | +0.35% |

Recent trading in Shift4 Payments (FOUR) is being shaped by mixed analyst sentiment around its expansion plans, the ongoing integration of the Global Blue acquisition, and management’s confidence in reaching a sizeable free cash flow run rate.

At a share price of US$66.00, Shift4’s 1-day share price return of 3.12% and 30-day share price return of 1.88% sit against a weaker 90-day share price return of 13.45% and a 1-year total shareholder return of 43.83%. This suggests recent momentum has picked up after a tougher year for holders, as investors weigh analyst downgrades against management’s free cash flow ambitions, the Global Blue integration and new large merchant wins.

If you are looking beyond a single payments name, this could be a good time to scan high growth tech and AI opportunities using our high growth tech and AI stocks.

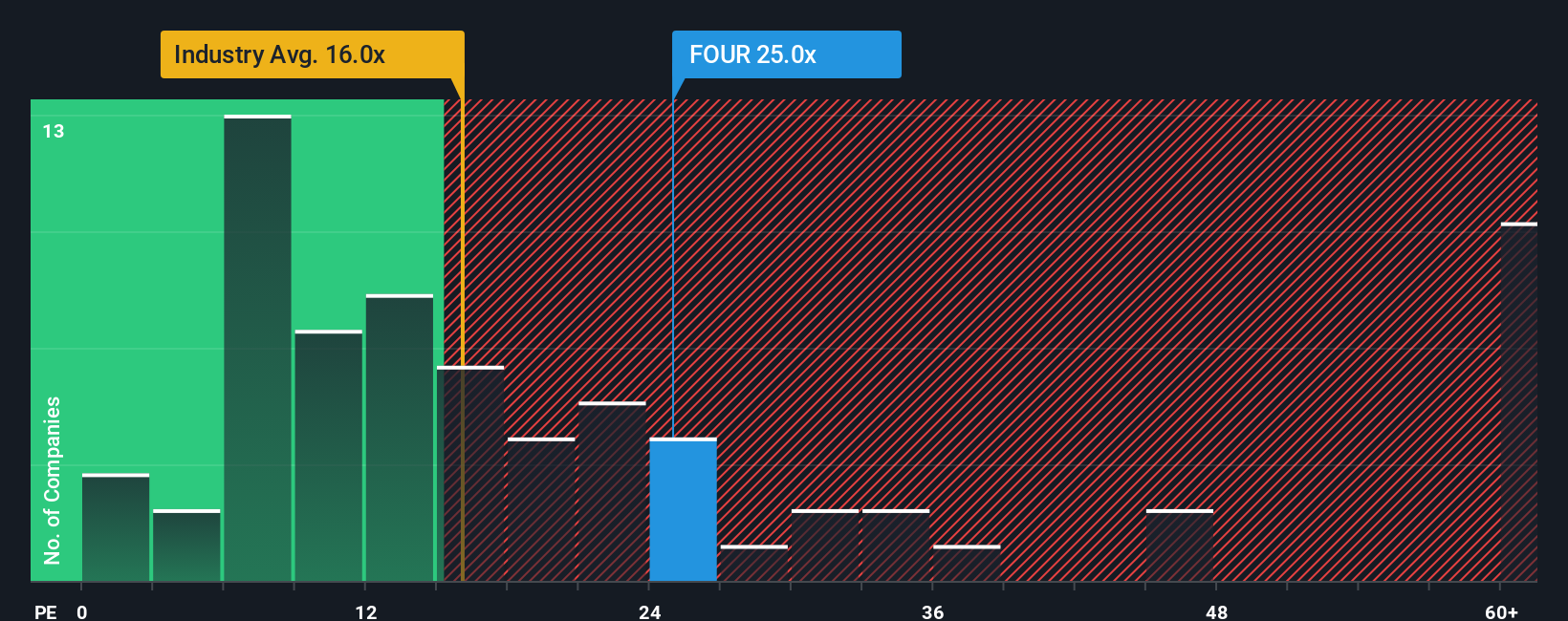

With FOUR trading at US$66.00 and sitting at a sizeable discount to the average analyst price target of US$88.83, the key question is whether the stock is still mispriced or if the market already reflects its future growth.

Most Popular Narrative: 31.1% Undervalued

At a last close of $66.00 versus a narrative fair value of $95.86, the widely followed view sees a large valuation gap anchored in long term growth and margin assumptions.

The broad adoption and integration of value added services (such as unified software and POS solutions like SkyTab) is driving higher merchant adoption internationally and domestically, supporting an increase in net spreads and boosting recurring, higher margin revenue streams.

Want to see what this recurring revenue push really implies for potential future earnings, margins, and valuation multiples? The narrative leans on ambitious growth expectations, richer profitability, and a specific earnings profile to explain that fair value gap. Curious which assumptions matter most and how they compare over time? Read on and test those numbers against your own view.

Result: Fair Value of $95.86 (UNDERVALUED)

However, you also need to weigh execution risk around the Global Blue and Smartpay integrations, as well as the impact of higher leverage and potential future dilution.

Another View: What The P/E Ratio Is Telling You

That $95.86 fair value comes from long term earnings assumptions, but the current P/E of 27x paints a different picture. It is higher than the US Diversified Financial industry at 14.8x and above the 23.8x fair ratio, which points to valuation risk if expectations slip.

Build Your Own Shift4 Payments Narrative

If you look at the data and reach a different conclusion, or prefer to test the assumptions yourself, you can build a tailored view in a few minutes using Do it your way.

A great starting point for your Shift4 Payments research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If you stop with just one company, you could miss opportunities sitting in plain sight, so widen your search and pressure test your ideas across more sectors.

- Spot potential mispricings early by scanning these 875 undervalued stocks based on cash flows that may offer more attractive entry points based on current cash flow expectations.

- Tap into future tech themes by reviewing these 24 AI penny stocks that link artificial intelligence growth stories with listed companies you can actually research.

- Target higher income potential by checking out these 12 dividend stocks with yields > 3% that pair yield above 3% with detailed fundamentals in one place.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.