A Look At SiteOne Landscape Supply (SITE) Valuation After Recent Share Price Weakness

SiteOne Landscape Supply, Inc. SITE | 0.00 |

Event context and recent stock performance

SiteOne Landscape Supply (SITE) has drawn investor attention after recent trading showed a 13.4% decline over the past week, alongside a similar pullback of about 12.9% over the past 3 months.

This short term weakness comes against a backdrop of modest year to date total return of about 0.4% and 1 year total return of roughly 3.1%, which may prompt investors to reassess what they are paying for the business.

With the share price at $125.61 and a 7 day share price return of about a 13.4% decline, recent momentum looks weak compared with a modest 1 year total shareholder return of roughly 3.1%, which may hint that expectations or perceived risk are resetting.

If this kind of pullback has you thinking about where else growth or resilience could be hiding, it may be worth scanning 17 top founder-led companies

So after this pullback, with SiteOne trading around $125.61 and some growth in revenue and net income on the table, is the recent weakness offering you an entry point, or is the market already pricing in future gains?

Most Popular Narrative: 4.3% Undervalued

According to the most followed narrative on SiteOne, a fair value of about $131.30 sits slightly above the recent $125.61 share price, which sets up a measured case for modest undervaluation rather than a deep value story.

In a market often dominated by tech narratives and consumer hype, SiteOne Landscape Supply (NYSE: SITE) operates in a space that is far more grounded, literally. Landscaping, irrigation, and outdoor materials may not grab headlines, but they sit at the intersection of long-term housing trends, climate adaptation, and consumer spending on livable space. That combination has quietly made SiteOne one of the more resilient names tied to the outdoor economy.

What supports that fair value gap? According to yiannisz, the narrative leans on steady revenue progress, improving profit margins, and a premium earnings multiple that assumes those trends hold. This brings those moving parts together into one price tag.

Result: Fair Value of $131.30 (UNDERVALUED)

However, the story can break if housing and construction activity softens further or if irrigation and outdoor projects slow, putting pressure on recent revenue and profit growth.

Another way to look at value

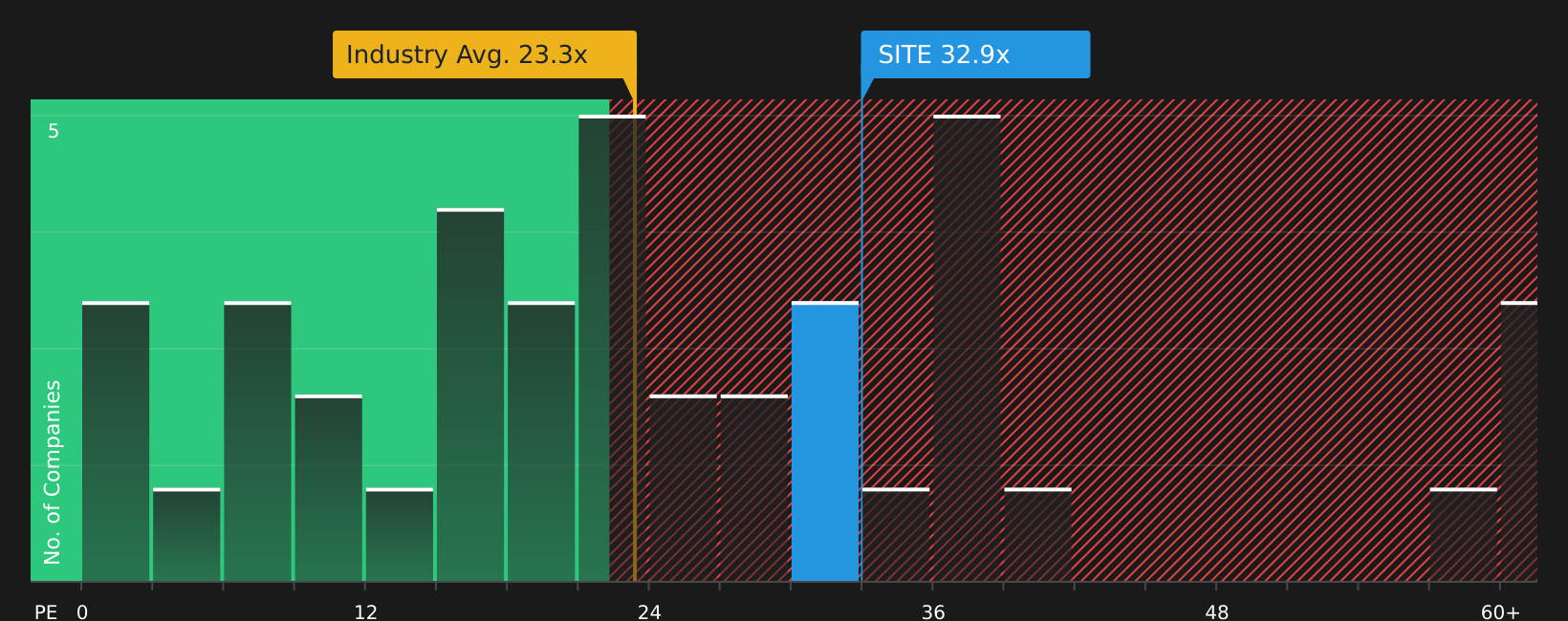

The narrative points to a modest 4.3% discount to fair value, but the earnings multiple tells a different story. SiteOne trades on a P/E of 36.5x, compared with 22.8x for peers, 24.3x for the US Trade Distributors industry, and a fair ratio of 30.6x. This tilts the picture toward valuation risk rather than a clear bargain. Is this premium simply the price of quality, or a gap that could eventually narrow?

Next Steps

With sentiment mixed and valuation signals pulling in different directions, it makes sense to review the underlying data yourself and not rely on headlines alone. If you want a quick snapshot of what the market currently views as positives, start by checking the 4 key rewards

Looking for more investment ideas?

Do not stop at one company. The sooner you scan a wider set of quality ideas, the better chance you have of spotting opportunities before the crowd.

- Target resilience and focus on businesses with strong finances by reviewing the solid balance sheet and fundamentals stocks screener (44 results).

- Hunt for potential mispricing and see which companies currently stand out in the 50 high quality undervalued stocks.

- Prioritize steady income and assess companies offering meaningful payouts using the 13 dividend fortresses.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.