A Look At SQM (NYSE:SQM) Valuation As New Ivanhoe Electric Copper Alliance Takes Shape

Sociedad Quimica y Minera de Chile S.A. Sponsored ADR Pfd Series B SQM | 83.21 | +1.70% |

Sociedad Química y Minera de Chile (NYSE:SQM) has entered a copper exploration collaboration with Ivanhoe Electric in northern Chile, funded initially with US$9 million and structured around potential 50/50 joint ventures on qualifying deposits.

This copper collaboration follows a sharp 45.03% 90 day share price return and an 84.72% 1 year total shareholder return. However, the recent 7 day share price pullback of 13.25% suggests some of that momentum may be cooling in the short term.

If this copper move has caught your attention, it may be worth seeing what else is happening in the space by checking our 7 top copper producer stocks identified by the Simply Wall St screener.

With SQM shares up strongly over the past year and trading only about 4.6% below the US$74.06 analyst price target, plus an indicated 13.17% intrinsic discount, you have to ask: Is this a genuine opportunity, or is the copper growth already reflected in the price?

Most Popular Narrative: 4.3% Undervalued

With Sociedad Química y Minera de Chile last closing at $70.82 against a most followed fair value estimate of $74.00, the narrative implies modest upside that hinges on how lithium and related projects play out over time.

Expansion of lithium production capacity in Australia (Mt. Holland and Kwinana refinery reaching full capacity) and Chile, along with investments in new projects like Salar Futuro, supports long-term volume growth and higher revenue potential for SQM over the next several years.

Curious what kind of revenue, margin and earnings profile that capacity build is aiming for, and what future earnings multiple underpins $74.00? The narrative spells out the growth rates, profitability jump and valuation reset it assumes, plus how an 8% to 9% discount rate ties those cash flows back to today.

On this view, the current $70.82 price sits a touch below the $74.00 fair value, with the discount rate of about 8.58% and higher revenue growth assumptions working against a more cautious margin outlook. The fair value also leans on a richer future P/E multiple than earlier estimates, reflecting updated expectations around lithium pricing, volumes and SQM's earnings mix across lithium, iodine and specialty nutrients.

Result: Fair Value of $74 (UNDERVALUED)

However, you still have to factor in lithium price volatility and the Codelco partnership terms, either of which could challenge the earnings and valuation assumptions behind that US$74 fair value.

Another View On SQM's Valuation

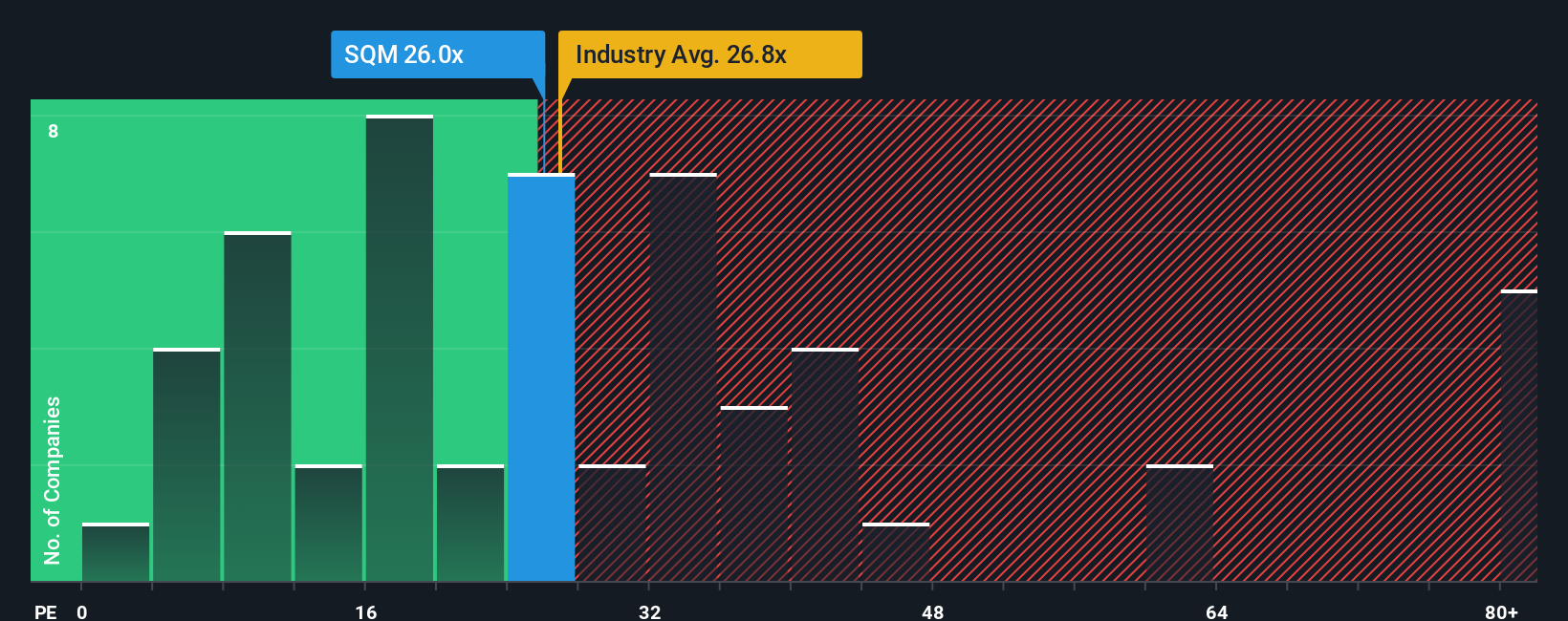

The fair value work you saw earlier leans on cash flows and discount rates, but the market is currently pricing SQM at a P/E of 38.6x. That is richer than the US Chemicals industry at 24.9x, the peer average at 24.2x, and even its own 31.2x fair ratio. This points to meaningful valuation risk if sentiment cools.

With the share price already stretching well above those comparison points, the question is whether you see enough earnings strength and lithium support to justify paying this valuation, or whether this is where you start demanding a wider margin of safety.

Build Your Own Sociedad Química y Minera de Chile Narrative

If you prefer a different interpretation of the numbers or like working through the assumptions yourself, you can build a custom SQM story in under three minutes, starting with Do it your way.

A great starting point for your Sociedad Química y Minera de Chile research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If SQM is on your radar, do not stop here; the screener can surface other opportunities that might fit your style even better.

- Target potential mispricings by reviewing our 55 high quality undervalued stocks that combine quality fundamentals with prices the screener flags as attractive.

- Protect your downside by checking 81 resilient stocks with low risk scores, focused on companies the screener marks with lower overall risk scores.

- Get ahead of the crowd by scanning the screener containing 25 high quality undiscovered gems that the screener highlights as high quality yet still under the radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.