A Look At StandardAero (SARO) Valuation After First CFM LEAP Engine Restoration Milestone

StandardAero, Inc. SARO | 26.26 | +0.04% |

StandardAero (SARO) has completed and delivered its first CFM LEAP engine performance restoration shop visit at its San Antonio facility. This marks a milestone that broadens its LEAP aftermarket offering for a growing global customer base.

At a share price of $30.57, StandardAero has a 90 day share price return of 24.83% and a 1 year total shareholder return of 15.01%, suggesting recent momentum has strengthened after some near term softness.

If this engine program news has you thinking about where else growth in aviation and related technologies might show up, you can use our screener of 32 robotics and automation stocks as a starting point for further research ideas.

With the shares trading at $30.57, a value score of 1, and an intrinsic discount of about 4%, is StandardAero still an underappreciated aftermarket player, or are markets already pricing in future growth?

Most Popular Narrative: 13.9% Undervalued

StandardAero's most followed narrative pegs fair value at $35.50 versus the current $30.57, framing the aftermarket story around earnings power over the next few years.

Accelerating LEAP engine inductions, a growing backlog and expanding OEM authorized repair content position StandardAero to scale toward roughly $1 billion of LEAP revenue in the next few years. This is expected to support sustained double digit top line growth and higher earnings as the program turns margin positive in 2026.

Curious what has to happen for that LEAP ramp to justify a higher valuation? The narrative leans heavily on improving margins and compounded earnings. Want to see the full set of assumptions that ties those moving parts to a $35.50 fair value?

Result: Fair Value of $35.50 (UNDERVALUED)

However, this hinges on LEAP and CFM56 programs turning margin positive as planned, and on parts shortages easing rather than turning into a longer term drag.

Another View: Earnings Multiple Sends A Different Signal

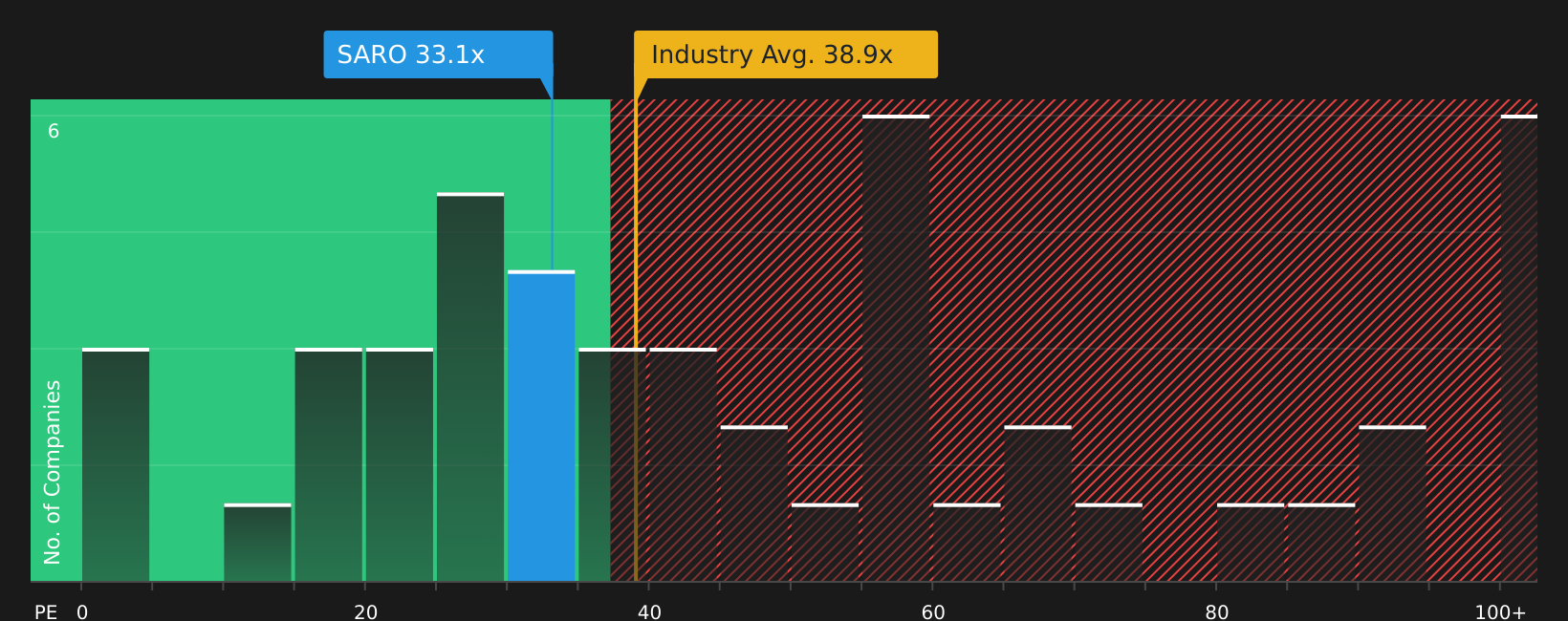

While the SWS DCF model suggests StandardAero is modestly undervalued, the current P/E of 55.1x tells a different story when you stack it against the US Aerospace & Defense industry at 40.7x, peers at 50.1x and a fair ratio of 33.2x. Is the market already paying up for the growth story and therefore raising the risk if expectations slip?

Build Your Own StandardAero Narrative

If parts of this story do not quite line up with your view, or you simply prefer to work from the raw data, you can build and stress test your own StandardAero thesis in just a few minutes, starting with Do it your way.

A great starting point for your StandardAero research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If StandardAero is on your radar, do not stop there. A few targeted stock lists can quickly widen your opportunity set and help you spot what others might overlook.

- Target income first and filter for companies with generous payouts using our list of 13 dividend fortresses that could help anchor the yield side of your portfolio.

- Hunt for quality at a sensible price by scanning 54 high quality undervalued stocks that pair solid fundamentals with valuations that may leave room for upside.

- Prioritise resilience by reviewing 83 resilient stocks with low risk scores that screen well on balance sheet strength and business risk so you are not relying on just one name.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.