A Look At Star Bulk Carriers (SBLK) Valuation After Strong Q1 Results And Higher Dividend

Star Bulk Carriers Corp. SBLK | 0.00 |

Star Bulk Carriers (SBLK) is back in focus after releasing first quarter 2026 results, reporting revenue of US$281.15 million and net income of US$58.53 million, along with a declared quarterly dividend of US$0.50 per share.

Recent price action suggests building momentum, with a 1 day share price return of 3.52%, a year to date share price return of 45.64%, and a 1 year total shareholder return of 77.34%. This reflects how investors are reacting to the stronger quarterly earnings and dividend update.

If this kind of move has you thinking about what else might be setting up, it could be a good time to run your eye over 33 power grid technology and infrastructure stocks

With earnings stronger than last year, a higher dividend in place, and the stock sitting about 10% below the average analyst price target, is Star Bulk still undervalued or already pricing in future growth?

Most Popular Narrative: 20.4% Overvalued

Against the latest close at $28.21, the most followed narrative pegs fair value at $23.43, using a discount rate of 11.04% and detailed long term forecasts.

The analysts have a consensus price target of $21.86 for Star Bulk Carriers based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $24.0, and the most bearish reporting a price target of just $18.3.

Curious what kind of revenue path, margin lift and future earnings multiple underpin that $23.43 fair value and updated targets? The underlying narrative leans on shifting growth assumptions, richer profitability, and a valuation reset that only makes sense when you see how the moving pieces fit together.

Result: Fair Value of $23.43 (OVERVALUED)

However, the story can change quickly if dry bulk demand stays weak, or if Star Bulk's aging, leveraged fleet faces higher compliance and financing costs than expected.

Another Lens on Value

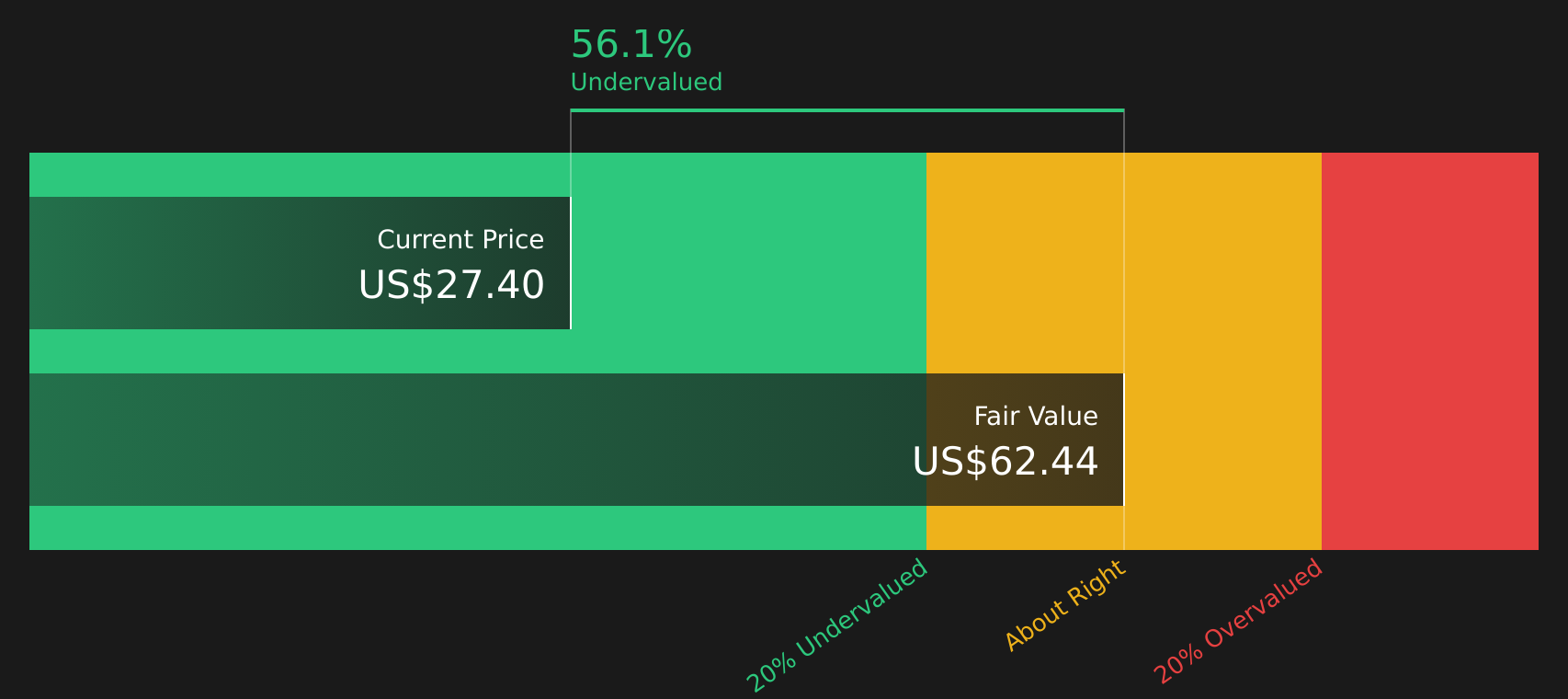

While the narrative fair value of $23.43 suggests Star Bulk Carriers is overvalued at $28.21, the SWS DCF model points the other way, with an estimated future cash flow value of $48.08, or about 41% above the current price. Which story do you think better fits the risk and return trade off here?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Star Bulk Carriers for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 47 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Given the mixed signals on value and the balance of risks and rewards, it makes sense to move fast and test the data for yourself. Start by weighing the 2 key rewards and 3 important warning signs.

Looking for more investment ideas?

If Star Bulk has your attention, do not stop here. Some of the most interesting opportunities sit just outside the obvious choices.

- Target dependable income streams by checking out 10 dividend fortresses that could support a steady dividend focused approach.

- Spot potential value opportunities early by scanning screener containing 22 high quality undiscovered gems before they land on everyone else's radar.

- Prioritise resilience under pressure by reviewing 62 resilient stocks with low risk scores designed to keep portfolio volatility in check.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.