A Look At Starbucks (SBUX) Valuation As Same Store Sales And Margins Face Ongoing Pressure

Starbucks Corporation SBUX | 90.37 | -0.07% |

Starbucks (SBUX) is back in focus after reports of continued same store sales declines and thinner operating margins, while options traders show unusually active, mixed positioning around the coffee chain’s near term outlook.

At a share price of US$90.56, Starbucks has posted a 30 day share price return of 6.10% and a 90 day share price return of 9.29%, yet its 1 year total shareholder return is roughly flat at a 0.11% decline. This suggests recent momentum is building after a softer longer term period as investors weigh weaker same store sales, thinner margins and the mixed options activity.

If Starbucks’ recent volatility has you thinking about diversification, this could be a useful moment to scan other consumer facing names through fast growing stocks with high insider ownership.

So with flat one year returns, modest recent gains, and concerns around softer same store sales and margins already on the table, is Starbucks quietly undervalued here, or is the market already baking in whatever growth comes next?

Most Popular Narrative: 3.8% Undervalued

With Starbucks closing at US$90.56 against a widely followed fair value of about US$94.13, the current setup leans slightly below that narrative mark while hinging on execution of its turnaround plans.

The Back to Starbucks strategy aims to improve partner engagement and reduce turnover, which is expected to enhance the customer experience and drive higher quality transactions, potentially increasing revenue and net margins. The rollout of the Green Apron service model, focusing on labor rather than equipment, is expected to improve throughput and reduce service times, leading to increased transaction growth, potentially impacting revenue and margins.

Curious how a service model tweak, higher projected earnings and a richer future P/E all feed into that fair value math? The full narrative lays out the exact growth, margin and valuation assumptions behind that US$94.13 figure.

Result: Fair Value of $94.13 (UNDERVALUED)

However, a 1% comparable store sales decline and a 450 basis point operating margin contraction from labor investments could quickly challenge that undervalued narrative if pressures persist.

Another View: Multiples Paint A Richer Picture

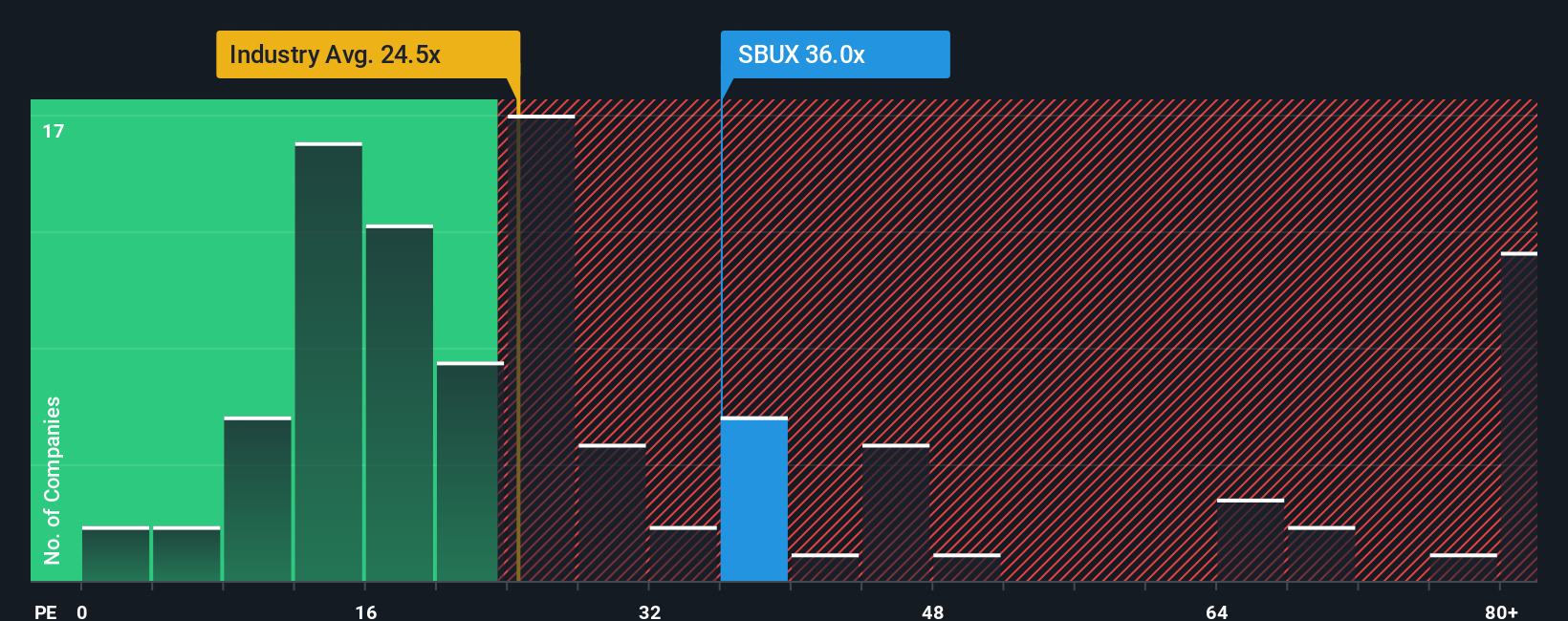

That 3.8% “undervalued” fair value story runs into a very different signal when you look at Starbucks’ current P/E of 55.5x. That is above the US Hospitality industry at 21.6x, above peer average at 49.7x, and well ahead of a 39.1x fair ratio the market could move towards over time.

If earnings or sentiment reset toward that fair ratio, today’s price could prove full rather than cheap. The question for you is whether Starbucks can grow into this premium or whether the multiple eventually needs to blink first.

Build Your Own Starbucks Narrative

If you see the story differently or want to test your own assumptions against the numbers, you can create a custom Starbucks view in just a few minutes, then Do it your way

A great starting point for your Starbucks research is our analysis highlighting 1 key reward and 5 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Before you move on, consider taking a moment to explore a few additional ideas that might complement or challenge your view on Starbucks.

- Scan for income possibilities and assess whether any of these 13 dividend stocks with yields > 3% suit the role you want dividends to play in your portfolio.

- Explore potential long term growth themes by checking out these 25 AI penny stocks that are connected to developments in artificial intelligence.

- Focus on value oriented opportunities by reviewing these 884 undervalued stocks based on cash flows that currently trade below what their cash flows may imply.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.