A Look At StubHub Holdings (STUB) Valuation As Shares Rebound And DCF Signals Possible Upside

StubHub Holdings Incorporation Class A STUB | 0.00 |

StubHub Holdings stock reaction and recent performance

StubHub Holdings (STUB) has drawn investor attention after recent trading, with the stock last closing at $9.73. The move comes as the company reports annual revenue of $1,793.63 million alongside a net loss of $1,923.97 million.

After a mixed few months, StubHub Holdings has seen a 36.08% 30 day share price return, although the year to date share price return is still down 31.91%. This suggests recent momentum is rebuilding from a weaker start to the year.

If this rebound has you rethinking where growth could come from next, it may be worth widening your watchlist to include 20 top founder-led companies

With StubHub trading at $9.73 against an analyst price target of $13.27 and an indicated intrinsic discount of around 76%, the key question is whether this gap signals a buying opportunity or whether markets already reflect future growth.

Most Popular Narrative: 59.8% Undervalued

StubHub Holdings latest close at $9.73 sits well below the most followed fair value estimate of $24.18. This estimate is built using a 10.05% discount rate and long term earnings forecasts.

Growing demand for live experiences globally, combined with the company’s expanding international footprint in regions like Asia and Latin America, positions StubHub to capture more cross border event tourism and increase earnings leverage as fixed costs are spread over higher GMS.

Want to see what has to happen for that gap to close? The narrative focuses on rapid revenue expansion, margin repair and a future earnings multiple that undercuts many entertainment peers.

Result: Fair Value of $24.18 (UNDERVALUED)

However, this depends on regulatory trends and StubHub’s push for market share, as tougher rules or weaker marketing efficiency could quickly challenge the bullish case.

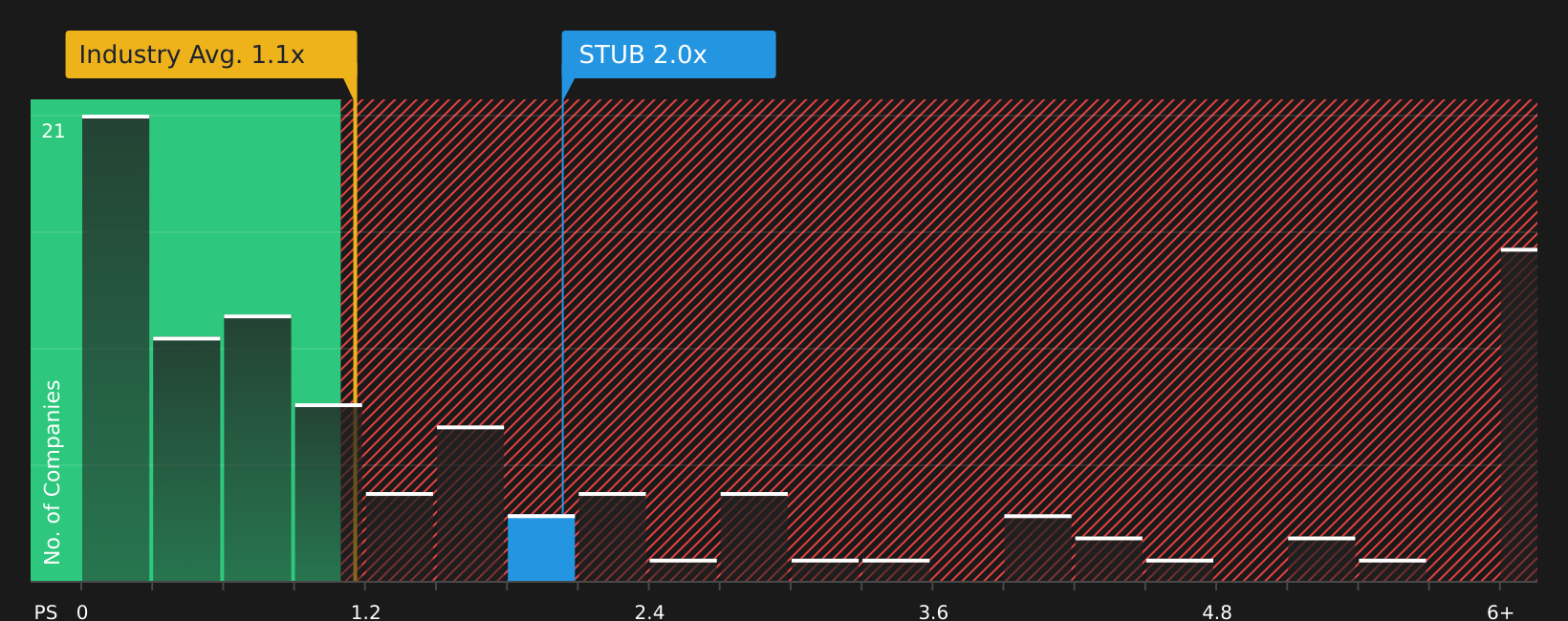

Another view: market pricing versus fair ratio

While the DCF work points to StubHub trading well below an estimated future cash flow value of $40.70 per share, the current P/S of 2x paints a different picture. It sits above the US Entertainment industry at 1.3x, yet below peers at 3.2x and its own fair ratio of 3x. That mix suggests both upside potential and the risk that sentiment stays cautious for longer than expected. Which signal do you trust more right now?

Next Steps

With sentiment split between upside and caution, this is a good moment to move quickly, test the assumptions against the numbers, and weigh the 2 key rewards.

Looking for more investment ideas?

If StubHub has sharpened your focus, do not stop here. Broadening your watchlist across quality, value and resilience can reveal opportunities you would otherwise miss.

- Target quality at a fair price by scanning a curated set of 46 high quality undervalued stocks that combine fundamentals with the potential for a better entry point.

- Prioritise resilience by checking out 65 resilient stocks with low risk scores that score well on stability so sudden shocks are less likely to catch you off guard.

- Spot potential future standouts early using the screener containing 21 high quality undiscovered gems before the crowd starts paying close attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.