A Look At Sun Communities (SUI) Valuation After Full Year Revenue Growth And Net Loss

Sun Communities, Inc. SUI | 129.25 | +1.47% |

Why Sun Communities Is Back on Investors’ Radar

Sun Communities (SUI) is back in focus after releasing full year results showing revenue of about US$3.24b alongside a net loss of US$345.4m, prompting a closer look at its fundamentals and recent share price performance.

The recent full year figures and net loss have landed against a period of rebuilding momentum, with the 1 year total shareholder return of 11.61% outpacing the more muted 3 year total shareholder return of a 4.18% decline. Shorter term share price gains suggest sentiment has improved as investors reassess risk and potential income resilience around the current US$126.11 level.

If Sun Communities has you rethinking where you want exposure to property linked income, it could be worth broadening your search to fast growing stocks with high insider ownership.

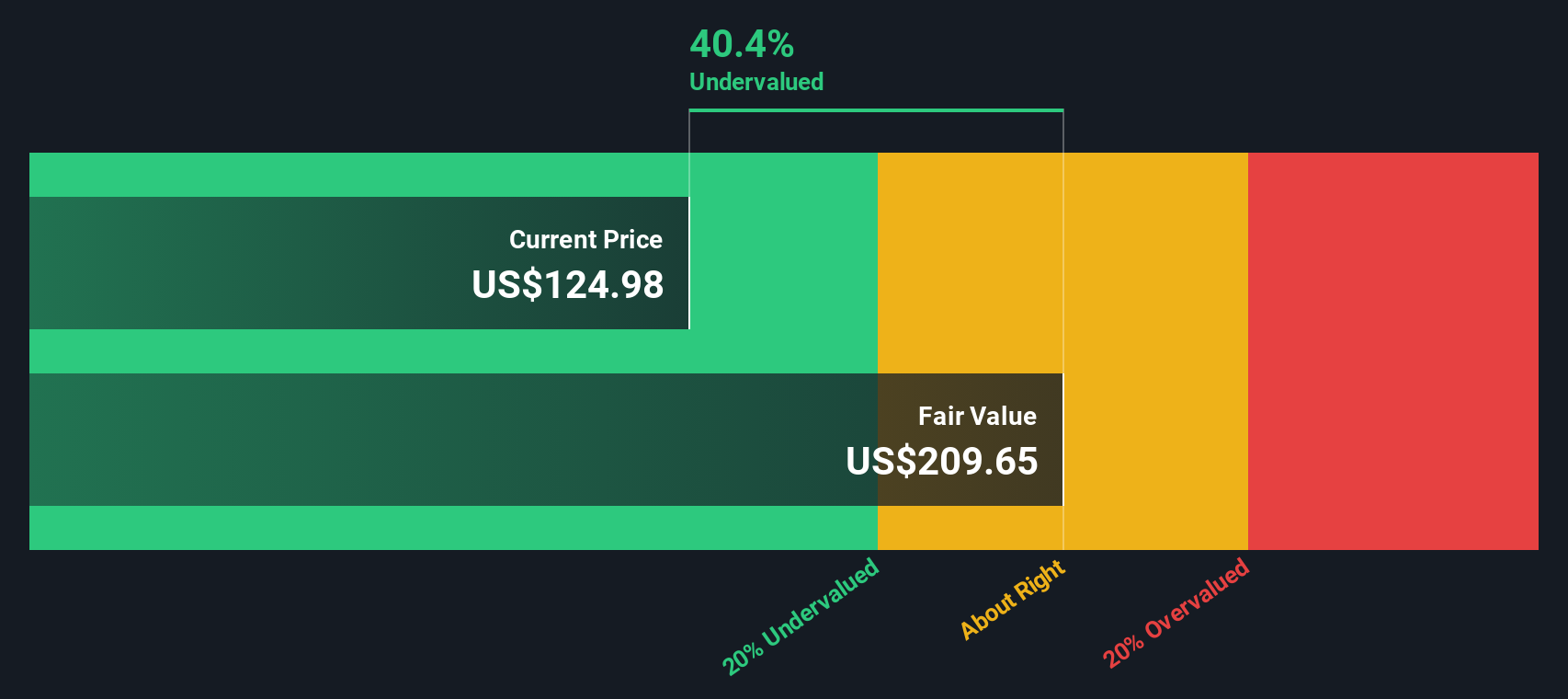

With the share price sitting around US$126.11, a value score of 4 and an indicated intrinsic discount of about 39%, the key question is whether Sun Communities is still undervalued or whether the market is already pricing in future growth.

Most Popular Narrative: 9.7% Undervalued

With Sun Communities last closing at US$126.11 against a fair value estimate of about US$139.65, the most followed narrative suggests some remaining upside, anchored in long term cash flow potential and margin recovery rather than short term share moves.

The analysts have a consensus price target of $139.647 for Sun Communities based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $155.0, and the most bearish reporting a price target of just $126.0.

Curious what has to happen for a loss making REIT to reach those earnings and margins? The narrative leans heavily on a sharp profitability shift, richer future multiples and a specific discount rate to justify that fair value.

Result: Fair Value of $139.65 (UNDERVALUED)

However, there are still pressure points, such as halted new developments and ongoing weakness in the RV segment, that could quickly challenge this underpriced story.

Another View: What The P/S Tells You

Our SWS DCF model points to a fair value of about US$206.72 per share, which suggests Sun Communities at US$126.11 is trading at a large discount. That sits uneasily next to a P/S ratio of 4.8x, which is higher than its own fair ratio of 4.2x, even though it is below peers at 6.3x and the wider North American Residential REITs group at 5x. If cash flows say one thing and sales multiples hint at a tighter margin of safety, which signal would you put more weight on?

Build Your Own Sun Communities Narrative

If you see the numbers differently or would rather test your own assumptions, it is quick to build a custom view and Do it your way.

A great starting point for your Sun Communities research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Ready for more investment ideas?

If Sun Communities has sharpened your focus, do not stop here, use the Simply Wall St Screener to uncover other opportunities that could fit your style and goals.

- Target reliable income by scanning for these 12 dividend stocks with yields > 3% that might suit a portfolio built around regular cash returns.

- Chase growth themes by reviewing these 28 AI penny stocks that are tied to long term trends in automation and data driven business models.

- Hunt for pricing gaps by assessing these 882 undervalued stocks based on cash flows that could be trading below their estimated cash flow value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.