A Look At Sunoco (SUN) Valuation After 2026 EBITDA Guidance And Parkland Acquisition Synergy Outlook

Sunoco LP SUN | 64.74 | +1.06% |

Sunoco (SUN) has put fresh numbers on the table for 2026, issuing adjusted EBITDA guidance of $3.1b to $3.3b, built around Parkland acquisition synergies and an ongoing bolt-on acquisition program.

Sunoco’s adjusted EBITDA outlook and ongoing acquisitions are landing at a time when momentum in the units has been firm, with a 10.11% 30 day share price return and a 5 year total shareholder return of 168.34% suggesting long term holders have already seen substantial value. Recent gains also hint at investor interest picking up around the latest guidance and upcoming 2025 results.

If this kind of deal making has your attention, it could be worth broadening your watchlist with aerospace and defense stocks that are also reshaping their futures.

With Sunoco trading at $57.60 against an average analyst price target of $64.22 and flagged by some as a value name, the key question is whether there is still an opportunity for investors or if the market is already pricing in any potential future growth.

Most Popular Narrative: 11% Undervalued

Against Sunoco’s last close of $57.60, the most followed narrative points to a fair value of about $64.71, suggesting some upside still embedded in its long term forecasts.

The NuStar and upcoming Parkland and TanQuid acquisitions are expected to deliver substantial double-digit accretion and cost synergies, further increasing operating leverage and net margins while materially enhancing Sunoco's international and midstream asset footprint.

Curious how a fuel distributor ends up with this kind of valuation gap? The narrative leans heavily on faster growth, higher margins, and a very different future earnings multiple. Want to see which assumptions really do the heavy lifting here?

Result: Fair Value of $64.71 (UNDERVALUED)

However, this hinges on fuel demand holding up and recent acquisitions delivering as planned, with any demand drop or integration misstep quickly challenging that upside story.

Another View: Richer Multiples, Different Message

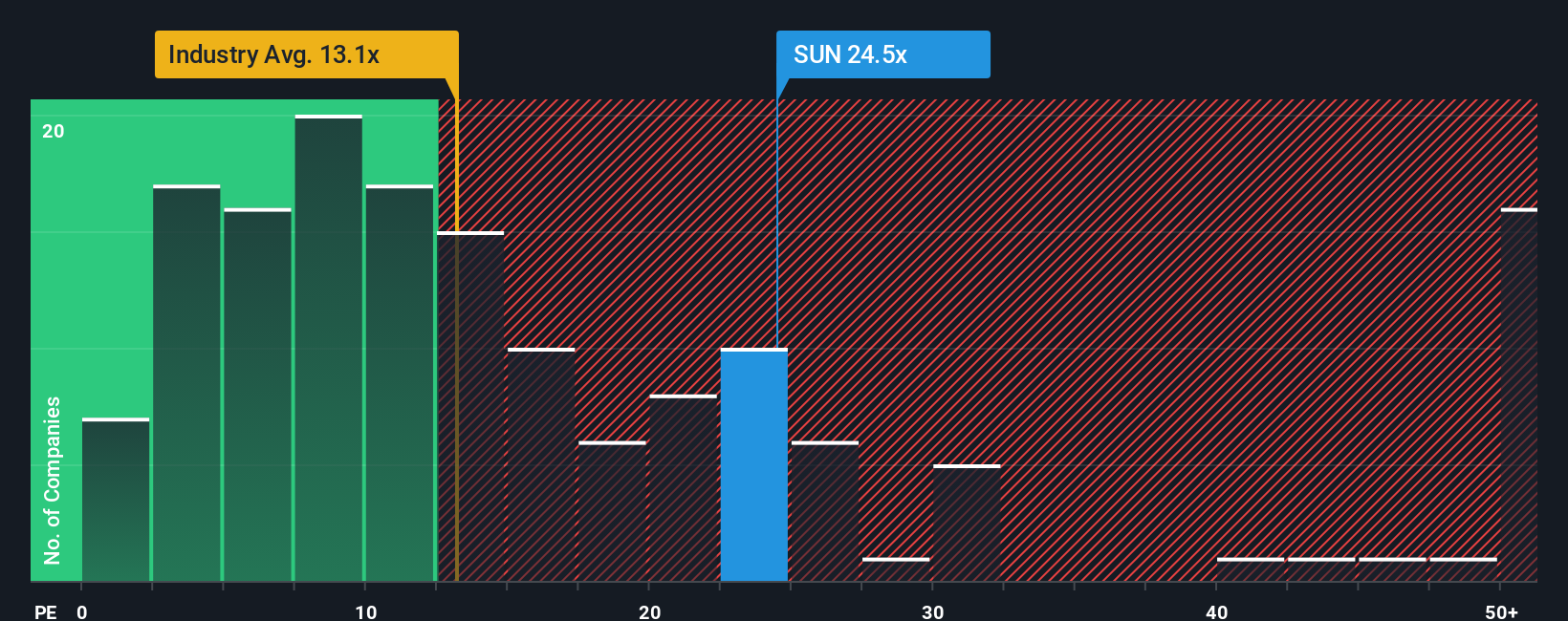

That 11% upside story sits alongside a different message from plain P/E math. Sunoco trades on about 27x earnings, above peers at 23.6x and well ahead of the wider US Oil and Gas industry at 13.7x, yet below its own fair ratio estimate of 30.2x.

In practice, that mix points to a unit price that already reflects plenty of optimism, while still leaving a small cushion if the market ever shifts closer to the fair ratio. The tension for you is clear: is this a premium you are comfortable paying for the current growth narrative, or a valuation risk you would rather avoid?

Build Your Own Sunoco Narrative

If you look at the numbers and reach a different conclusion, or simply prefer your own homework, you can build a custom narrative in minutes, starting with Do it your way.

A great starting point for your Sunoco research is our analysis highlighting 2 key rewards and 4 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Sunoco has sharpened your thinking, do not stop here. Widen your opportunity set now so you are not relying on a single story or sector.

- Target higher income by reviewing these 12 dividend stocks with yields > 3% that may offer stronger yields than keeping cash on the sidelines.

- Chase potential growth by scanning these 24 AI penny stocks positioned around artificial intelligence, data infrastructure, and software adoption.

- Hunt for price gaps by checking these 868 undervalued stocks based on cash flows that appear mispriced when you line up cash flows against current market expectations.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.