A Look At Swarmer (SWMR) Valuation After Shelf Registration Sparks Fresh Market Attention

Swarmer SWMR | 0.00 |

Swarmer (SWMR) has filed a shelf registration to offer up to 3,000,000 shares of common stock, totaling about US$180.96 million. This move gives the company added capital-raising flexibility.

The shelf registration news has arrived at a time when Swarmer’s share price performance has been volatile. The 30 day share price return of 69.87% and the year to date share price return of 82.15% contrast with recent declines, suggesting momentum has cooled in the very near term.

If this kind of sharp move has your attention, it could be a good moment to see how other defense focused AI and autonomy players are trading by scanning 48 AI infrastructure stocks

With Swarmer’s shares up 82.15% year to date and trading only about 6% below the US$60 analyst target, the key question is whether recent growth justifies the current valuation or whether the market is already pricing in future gains.

Preferred Price-to-Book of 26.4x: Is it justified?

Swarmer’s stock currently screens as expensive on its preferred valuation yardstick, with a P/B of 26.4x compared with both sector and peer averages despite the recent pullback.

The P/B ratio compares the company’s market value to its book value, which is essentially net assets on the balance sheet. For an early stage defense focused AI software business with limited revenue and current losses, a high P/B often reflects that investors are paying up for potential future cash flows rather than current balance sheet strength.

In this case, the gap is wide. Swarmer’s 26.4x P/B stands against a 3.7x average for the US Aerospace & Defense industry and 3.6x for its immediate peer set, indicating that the stock trades at a substantial premium to both groups.

Result: Price-to-book of 26.4x (OVERVALUED)

However, the recent share price slide and ongoing net losses of about US$12.29 million highlight execution and funding risks that could quickly challenge this premium story.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

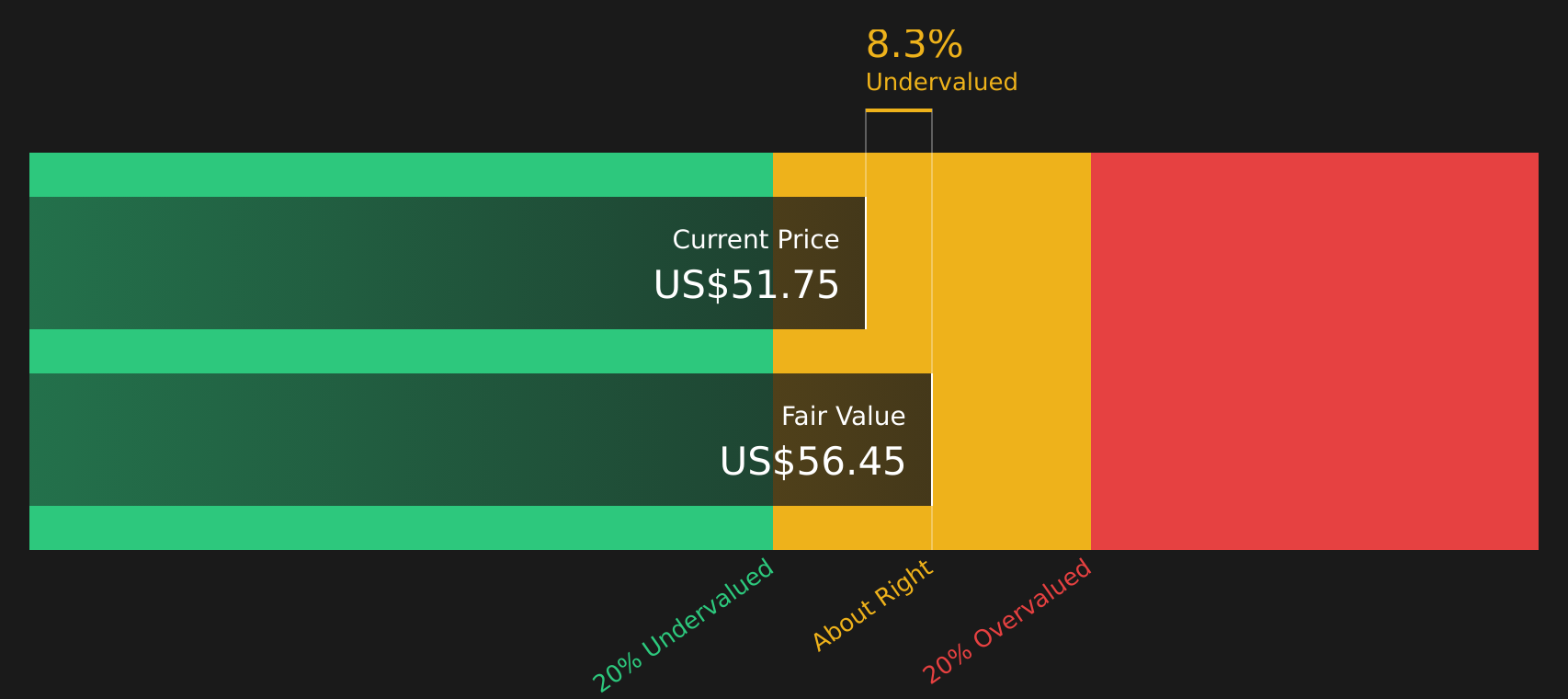

Another view from the SWS DCF model

While the 26.4x P/B suggests a rich price tag, the SWS DCF model comes out with a very similar result, with Swarmer trading at about $56.47 versus an estimated future cash flow value of about $56.26. If both stories line up this closely, where could fresh upside or downside come from next?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Swarmer for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 47 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment clearly mixed, this is a good moment to move fast, review the facts yourself, and weigh Swarmer’s upside against its risks by checking the 1 key reward and 3 important warning signs

Looking for more investment ideas?

If Swarmer’s story has you thinking bigger, do not stop here, use the Simply Wall St screener to spot other opportunities before they race ahead of you.

- Target potential bargains by scanning 47 high quality undervalued stocks that combine strong fundamentals with prices the market may be overlooking.

- Prioritise stability by reviewing 63 resilient stocks with low risk scores that score well on resilience, so sudden surprises are less likely to catch you off guard.

- Hunt for early standouts with the screener containing 20 high quality undiscovered gems that have solid numbers but still sit under most investors’ radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.