A Look At Sysco (SYY) Valuation After Earnings Beat And Strong January Outlook

Sysco Corporation SYY | 71.16 | -0.66% |

Sysco (SYY) shares recently moved higher after the company reported quarterly results that aligned with revenue expectations and delivered slightly better adjusted earnings, supported by improving case volumes and disciplined expense control.

The recent earnings beat and upbeat commentary on January trading have been reflected in Sysco’s 30-day share price return of 15.89% and year to date share price return of 16.52%, while the 1-year total shareholder return of 22.07% points to improving momentum rather than a sudden spike.

If Sysco’s move has you thinking about where else capital could work hard, it may be worth scanning our list of 22 top founder-led companies as a next research stop.

With Sysco now trading near US$85 after a strong run, its implied intrinsic discount of about 37% and modest gap to the average analyst target raise the key question: is there still mispricing here or has the market already baked in the next leg of growth?

Most Popular Narrative: 2.5% Undervalued

Sysco’s most followed narrative pegs fair value around $86.75, only a touch above the recent $84.62 close. This sets up a nuanced valuation story rather than a clear bargain.

Strategic cost management and self funded initiatives targeting $100 million in profit improvement, alongside disciplined capital allocation for shareholder returns, are expected to support future cash flow and earnings growth even amidst macroeconomic uncertainties.

Curious how that projected profit uplift, modest revenue build and a tighter margin profile add up to this fair value gap and future earnings multiple story? The full narrative lays out the cash flow path, the earnings step up and the pricing of those profits in a way a quick headline simply cannot capture.

Result: Fair Value of $86.75 (UNDERVALUED)

However, the story could look different if weak restaurant traffic persists or if higher labor and tariff related costs squeeze margins more than analysts currently assume.

Another Angle On Valuation

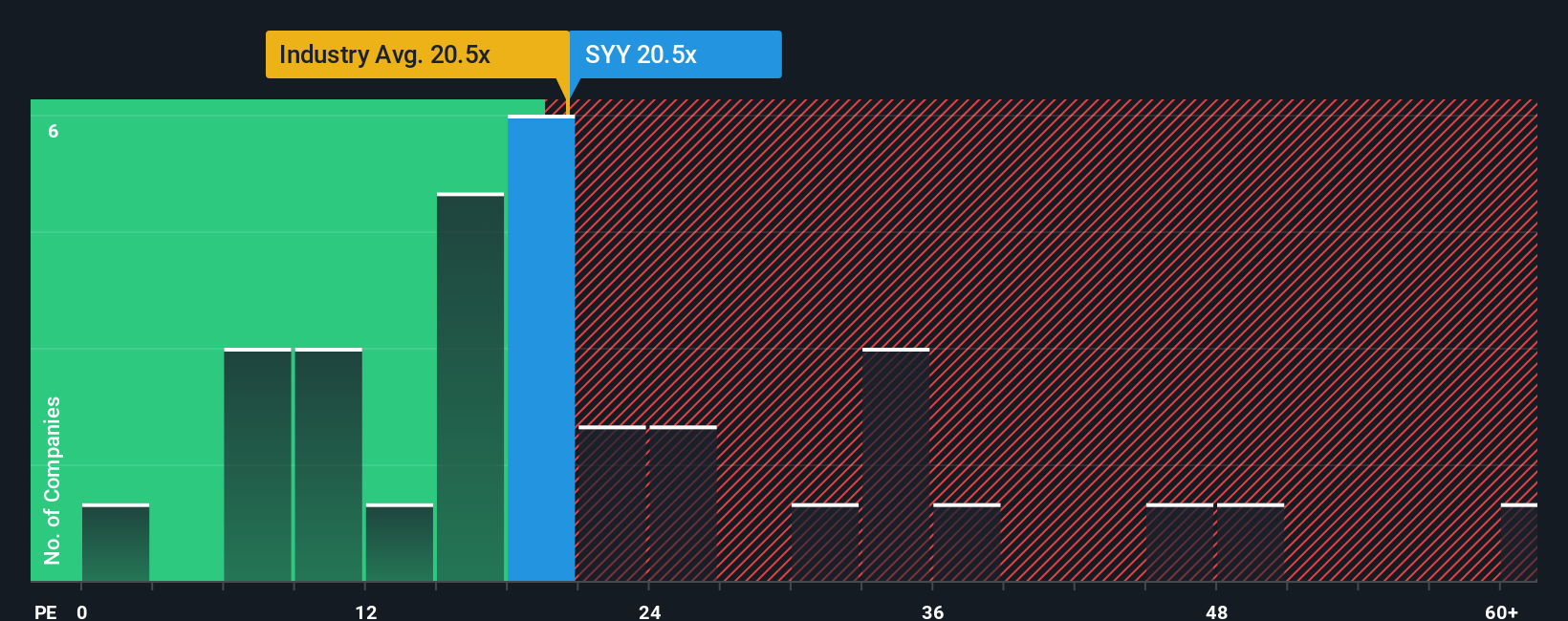

On earnings multiples, Sysco looks fairly tightly priced. The stock trades on a P/E of 22.5x, very close to the US Consumer Retailing average of 22.4x, yet below both its peer average of 35.3x and a fair ratio estimate of 26.1x. This points to a valuation gap some investors may see as cushion rather than upside. The question is whether that gap reflects untapped potential or simply higher risk around execution and debt funding.

Build Your Own Sysco Narrative

If this view does not quite match your own instincts, or you would rather test the assumptions yourself with the latest data, you can build a custom Sysco thesis in just a few minutes, starting with Do it your way.

A great starting point for your Sysco research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Ready to hunt for your next idea?

If Sysco is already on your watchlist, do not stop there. Cast the net wider and let fresh data driven ideas challenge and sharpen your portfolio thinking.

- Target resilient income by checking companies in our 15 dividend fortresses that offer higher yields with a focus on stability.

- Spot potential mispricing by scanning the 55 high quality undervalued stocks that pair quality fundamentals with discounted market prices.

- Get ahead of the crowd by reviewing our screener containing 25 high quality undiscovered gems before they land on everyone else’s radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.