A Look At T-Mobile US (TMUS) Valuation As Verizon News Refocuses Attention On Growth Prospects

T-Mobile US, Inc. TMUS | 201.40 | -1.40% |

T-Mobile US (TMUS) is back in focus after a 4.2% share move that followed Verizon’s new buyback announcement, recent competition commentary, and growing attention on T-Mobile’s upcoming earnings and capital markets day.

At a share price of US$194.99, T-Mobile US has seen mixed momentum, with a 7 day share price return of 3.74% sitting against a 30 day return of 2.30% and a 1 year total shareholder return of 16.83% loss. This suggests recent interest has picked up while longer term gains have leveled off.

If Verizon’s buyback and competition comments have you thinking about where capital might move next in telecom and adjacent tech, it could be a useful moment to scan high growth tech and AI stocks for other potential ideas riding similar themes.

With T-Mobile posting annual revenue of US$85.8b and net income of US$11.9b, along with a recent 16.83% one-year total return loss, the key question is whether current pricing is conservative or already reflecting future growth potential.

Most Popular Narrative: 26.9% Undervalued

Compared with the narrative fair value of $266.82, T-Mobile US at $194.99 sits at a sizable discount, and the story behind that gap centers on how future growth, margins and cash returns could develop.

The launch and expansion of T-Fiber following the acquisition of Lumos, along with further expansion plans via Metronet, could lead to incremental service revenue growth and enhance long-term profitability.

The company's strategic investments and partnerships in fiber markets, designed to leverage T-Mobile's customer base and network capabilities, are likely to provide improved EBITDA growth and value-accretive returns from increased broadband penetration.

Curious what earnings profile and margin structure need to sit behind that fair value estimate? The narrative leans on specific growth, profitability and cash return assumptions that go well beyond headline 5G momentum.

Result: Fair Value of $266.82 (UNDERVALUED)

However, higher handset tariffs or more aggressive competitor promotions could weigh on margins and customer growth, challenging the earnings path implied in the current narrative.

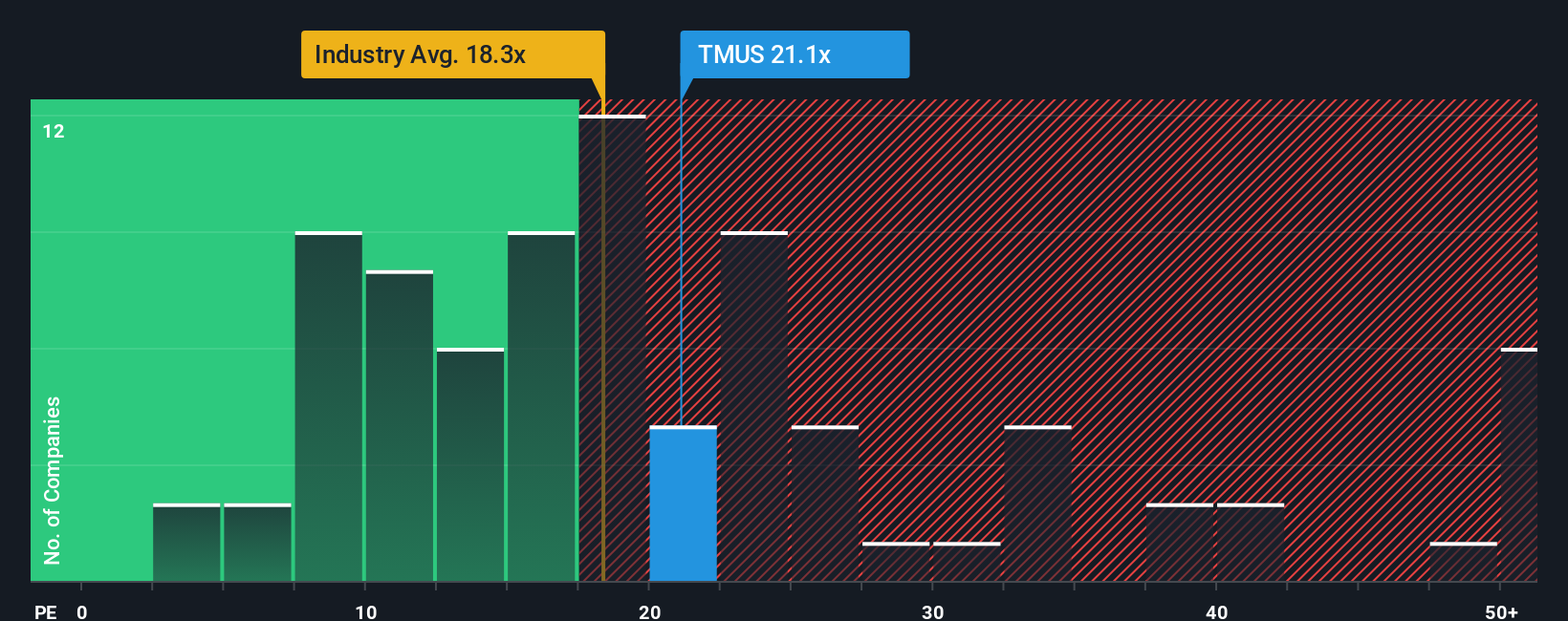

Another View: What The P/E Signals

Our first take leans on a narrative fair value of $266.82, which points to T-Mobile US looking undervalued at $194.99. Yet its current P/E of 18.4x sits above a fair ratio of 16.3x, even though it is roughly in line with the global wireless telecom average of 18.5x and well below peer averages of 32.6x. That mix of discount and premium leaves a simple question for you: is the market underpricing future cash flows or already paying up for them through earnings?

Build Your Own T-Mobile US Narrative

If you see the data a little differently, or prefer to test your own assumptions, you can build a custom T-Mobile US story in just a few minutes, starting with Do it your way.

A great starting point for your T-Mobile US research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If you stop at just one company, you risk missing other opportunities that fit your style, so put the Simply Wall St Screener to work for you.

- Spot potential high-upside opportunities early by checking out these 3542 penny stocks with strong financials that already show stronger financial foundations.

- Ride the long-term shift toward automation and data by scanning these 24 AI penny stocks that are directly plugged into artificial intelligence trends.

- Focus on price versus cash flow and let these 876 undervalued stocks based on cash flows surface companies that screen cheap on fundamentals, not just headlines.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.