A Look At Talen Energy (TLN) Valuation After Long Term AWS Deal And Reaffirmed 2026 Targets

Talen Energy Corp TLN | 327.58 | -0.15% |

Talen Energy (TLN) is back in focus after its long term deal to supply carbon free nuclear power to Amazon Web Services data centers, along with reaffirmed 2026 guidance and an ongoing share repurchase program.

The long term AWS contract, reaffirmed 2026 guidance and upcoming earnings update have arrived alongside a 1 month share price return of 11.71% and a 1 year total shareholder return of 79.79%. Together, these factors suggest momentum has recently picked up after softer year to date share price performance.

If this kind of nuclear power story has your attention, it could be worth scanning our 84 nuclear energy infrastructure stocks to look for other potential beneficiaries of rising demand for low carbon baseload energy.

With the stock up 79.79% over the past year, a long term AWS deal in hand and management reaffirming 2026 targets, the real question now is whether Talen is still mispriced or if the market already sees the future growth story.

Most Popular Narrative: 32.5% Overvalued

At a last close of $391.43 versus a narrative fair value of $295.50, the current price sits well above the level this valuation model points to. This sets up a clear tension between market enthusiasm and the story behind that number.

"Talen Energy (TLN) is at the epicenter of the 2026 energy rotation, with shares trading around $382 as investors scramble for reliable, "always-on" carbon-free power. The company's crown jewel, the Susquehanna nuclear plant, has become one of the most valuable assets in the PJM Interconnection grid. Following a landmark 1.9 GW power purchase agreement with Amazon Web Services (AWS), Talen has transitioned from a merchant power producer to a specialized infrastructure provider for the cloud. This 17-year contract is expected to generate approximately $18 billion in revenue, providing a level of cash flow visibility rarely seen in the independent power producer (IPP) sector."

Curious how a long dated AWS contract, projected cash flows and margin assumptions all feed into that $295.50 figure, rather than something closer to today’s price? The narrative leans heavily on detailed cash flow forecasts, nuclear asset uptime and future earnings power to anchor its view. If you want to see which specific growth and profitability assumptions justify calling Talen 32.5% overvalued, the full valuation story lays it all out.

Result: Fair Value of $295.50 (OVERVALUED)

However, the story could shift quickly if regulators tighten data center power rules or if high capital spending for nuclear and gas assets reduces expected cash flow.

Another View: DCF Paints a Very Different Picture

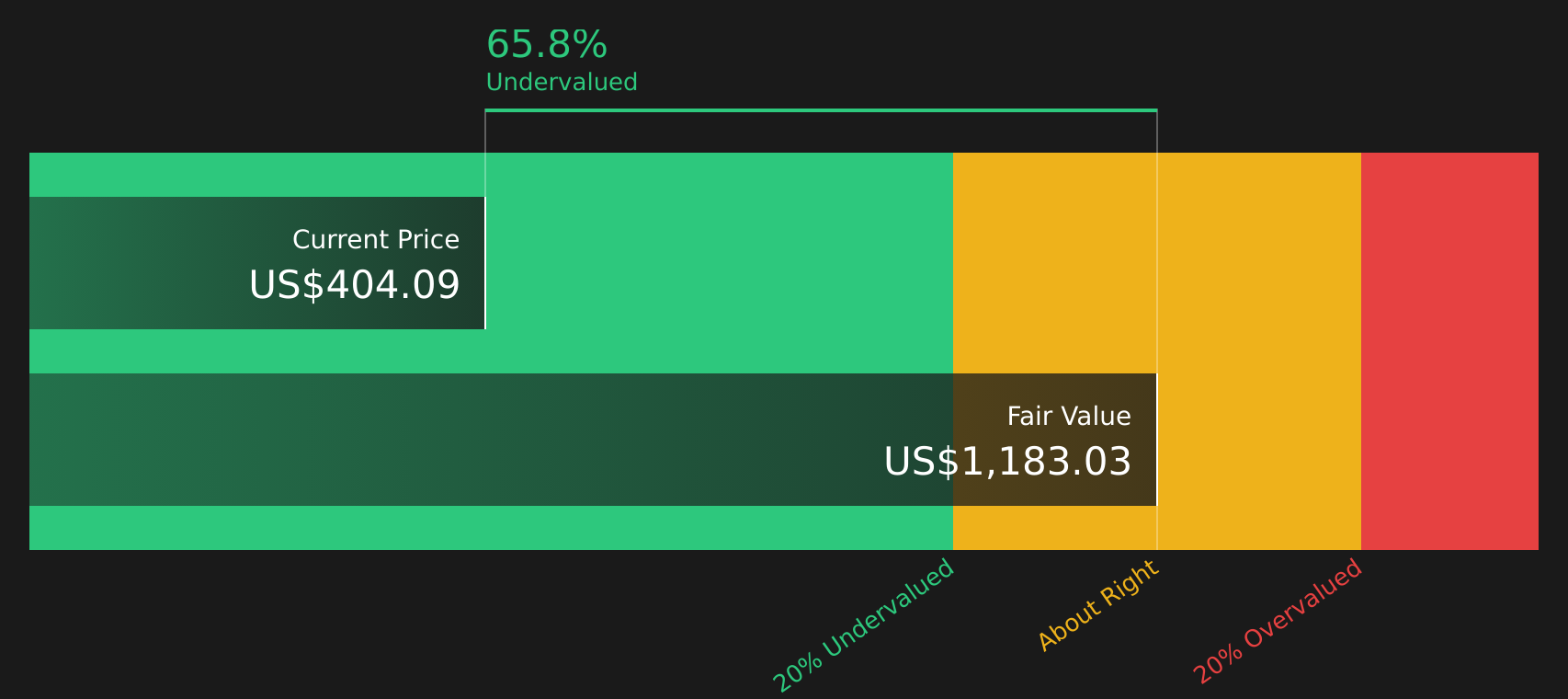

The user narrative pegs fair value at $295.50 and calls Talen about 32.5% overvalued, but our DCF model comes back with a future cash flow value of $1,037.55 per share, which is far above the current $391.43 price. That gap raises a simple question: which story do you think is closer to reality?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Talen Energy for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 53 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this mix of bullish and cautious signals has you thinking hard about what comes next, now is a good time to dig into the details and form your own view. You can start with 2 key rewards and 3 important warning signs.

Looking for more investment ideas?

If Talen has sharpened your interest, do not stop here, use the Simply Wall St Screener to quickly surface other stocks that might fit your approach.

- Target quality at a discount by scanning our 53 high quality undervalued stocks to see which companies currently line up with attractive fundamentals and pricing.

- Prioritise resilience by checking the 80 resilient stocks with low risk scores to focus on businesses that score well on stability and risk factors.

- Hunt for potential standouts by reviewing the screener containing 23 high quality undiscovered gems that are flying under the radar but already show solid underlying numbers.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.