A Look At TD SYNNEX (SNX) Valuation After The New Ramp Partnership Announcement

TD SYNNEX Corporation SNX | 0.00 |

TD SYNNEX (SNX) has drawn fresh investor attention after agreeing to distribute Ramp’s all-in-one spend management platform across its extensive U.S. reseller network, giving partners access to integrated cards, expenses, bill payments, procurement, and accounting tools.

Those distribution wins have landed during a strong run for the stock, with the share price at US$246.76 and recent momentum reflected in a 9.32% 1 month share price return and a 102.70% 1 year total shareholder return, signaling building optimism.

If partnerships like Ramp’s spend management platform have your attention, it could be a good moment to broaden your search and check out 47 AI infrastructure stocks

With TD SYNNEX trading around US$246.76 after strong recent returns, the key question is whether the current price already reflects its growth prospects, or whether there is still a potential opportunity that markets have not fully priced in.

Most Popular Narrative: 8.3% Overvalued

The most followed narrative puts TD SYNNEX's fair value at $227.82, slightly below the last close at $246.76, and anchors that view in specific growth and margin assumptions.

The analysts have a consensus price target of $227.82 for TD SYNNEX based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $271.0, and the most bearish reporting a price target of just $166.0.

Curious what justifies that fair value being below today’s price? The narrative leans on measured revenue growth, steady margins and a future earnings multiple that diverges from the wider sector. The key is how those moving parts are wired together over the next few years.

Result: Fair Value of $227.82 (OVERVALUED)

However, there are a few pressure points that could challenge this story, including customer concentration around Hyve and ongoing margin pressures from foreign exchange and project mix.

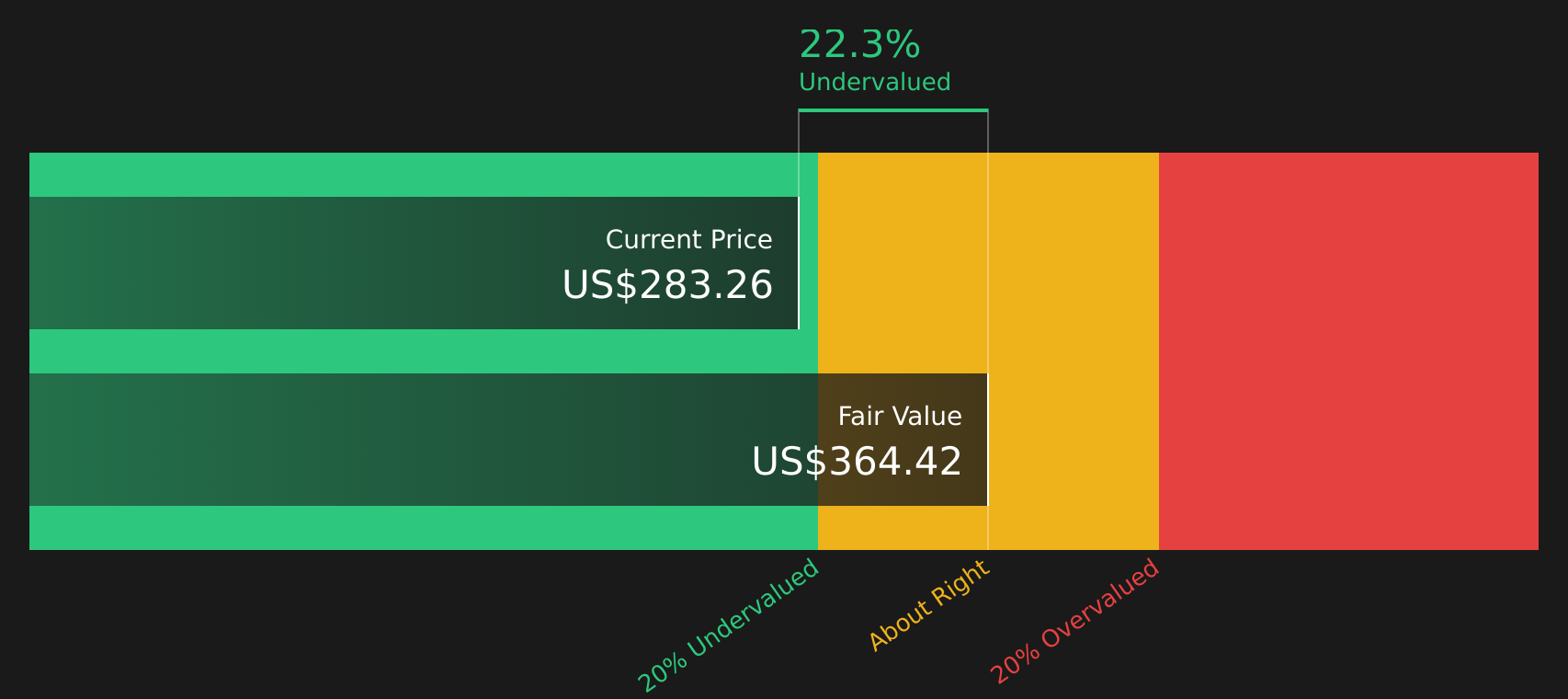

Another View: Cash Flows Point To Underpricing

Analysts see TD SYNNEX as about 8.3% overvalued on a US$227.82 fair value, but the SWS DCF model points the other way, with a fair value of US$286.27 and the stock trading 13.8% below that level. Which set of assumptions do you find more convincing?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out TD SYNNEX for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 47 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment clearly split between opportunity and caution, this is a moment to look at the data yourself, move quickly, and weigh both sides through the lens of 3 key rewards and 1 important warning sign

Looking for more investment ideas?

If TD SYNNEX has sharpened your focus, do not stop here. Broaden your watchlist now or you may miss companies that better match your style.

- Target value first and see which companies line up with your checklist by scanning 47 high quality undervalued stocks.

- Prioritise resilience and sift through stocks with balance sheets that look sturdier using the solid balance sheet and fundamentals stocks screener (45 results).

- Hunt for lesser known opportunities before they are crowded trades by checking the screener containing 22 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.