A Look At Telephone And Data Systems (TDS) Valuation After US$1b Spectrum Sale And Special Dividend

Telephone and Data Systems, Inc. TDS | 44.89 | +1.70% |

Event overview and why it matters

Telephone and Data Systems (TDS) is in focus after subsidiary Array Digital Infrastructure completed a sale of certain spectrum assets to New Cingular Wireless PCS for over US$1b in cash, accompanied by a special cash dividend.

The spectrum sale and special dividend arrive during a strong run in Telephone and Data Systems shares, with a 17.39% 1 month share price return and a 28.05% 1 year total shareholder return. The very large 3 year total shareholder return above 7x suggests momentum has been building rather than fading.

If this kind of telecom rerating has your attention, it could be a good time to scan other healthcare stocks for contrasting defensiveness and income characteristics.

With TDS shares up strongly over 1 month, 1 year and even 3 years, and the spectrum sale bringing in over US$1b in cash plus a special dividend, is there genuine value left here or is the market already pricing in future growth?

Most Popular Narrative: 8.9% Undervalued

With Telephone and Data Systems closing at US$44.34 against a narrative fair value of about US$48.67, the story focuses on how far its transformation can go.

The divestiture of UScellular and major spectrum assets has substantially deleveraged TDS's balance sheet, freeing up capital for aggressive expansion in fiber infrastructure and providing flexibility for opportunistic M&A. Both of these factors are positioned to influence long-term revenue and earnings as broadband demand intensifies.

Curious what kind of revenue reset, margin shift, and future earnings base are reflected in that price target? The narrative leans on bold profitability assumptions and a valuation multiple that sits below current industry levels. Want to see how those moving parts add up to the fair value figure?

Result: Fair Value of $48.67 (UNDERVALUED)

However, the story can shift quickly if legacy copper and cable revenue pressure persists, or if heavy fiber capex strains cash flows and limits financial flexibility.

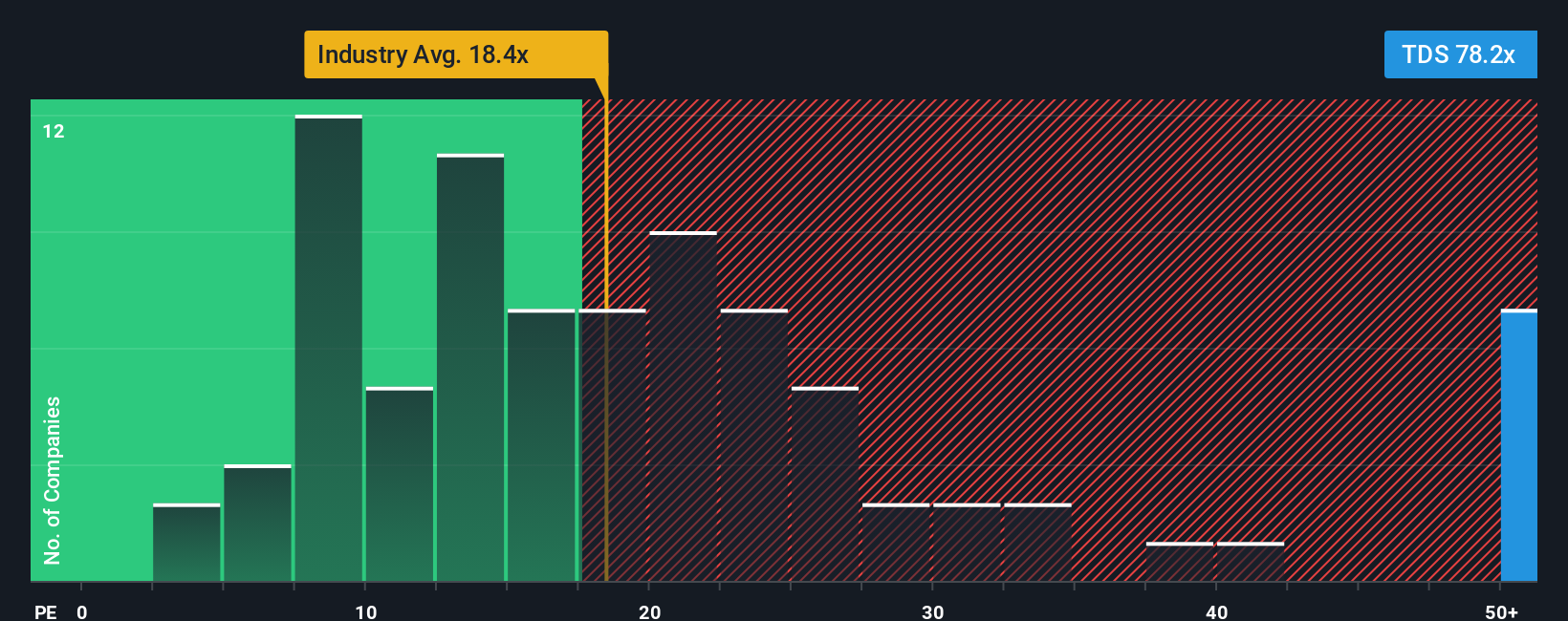

Another angle on valuation

The fair value story around US$48.67 suggests Telephone and Data Systems might still have some upside, but the earnings multiple sends a very different message. The current P/E of 90.9x compares with a fair ratio of 36.3x, the US peer average of 15.5x, and a global wireless average of 18.5x.

That gap implies the market is already paying a rich price for each dollar of earnings, which could limit room for disappointment. The question is whether you think TDS can grow into that premium, or whether this sets up more valuation risk than you are comfortable with.

Build Your Own Telephone and Data Systems Narrative

If you see the numbers differently or prefer to weigh the assumptions yourself, you can build a fresh TDS story in minutes with Do it your way.

A great starting point for your Telephone and Data Systems research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas beyond TDS?

If you are serious about sharpening your portfolio, do not stop at one stock. Use the Simply Wall St Screener to compare themes, risks, and potential rewards side by side.

- Target income potential with these 12 dividend stocks with yields > 3%, focusing on companies that already offer yields above 3% instead of waiting for returns that may or may not arrive.

- Capture growth themes early by scanning these 25 AI penny stocks, where businesses are using artificial intelligence to reshape how products are built, delivered, and monetised.

- Hunt for mispriced opportunities using these 886 undervalued stocks based on cash flows, so you can spot stocks where current prices differ from cash flow based assessments before they move back in line.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.