A Look At Tractor Supply (TSCO) Valuation After 2025 Results And 2026 Growth Guidance

Tractor Supply Company TSCO | 0.00 |

Tractor Supply (TSCO) is back in focus after reporting fourth quarter and full year 2025 results. The company showed higher sales alongside relatively steady net income, and paired those numbers with fresh 2026 guidance.

The earnings release, new 2026 guidance and ongoing share buybacks appear to have caught investors' attention, with a 1 day share price return of 3.39% and a 30 day share price return of 10.94% lifting year to date gains to 8.75%. The 5 year total shareholder return of 91.70% points to a stronger longer term record than the more modest 1 year total shareholder return of 4.85%, suggesting momentum has picked up recently compared with the past year.

If Tractor Supply’s update has you thinking about where else capital might work hard, this could be a good moment to look at fast growing stocks with high insider ownership as a fresh hunting ground.

With sales moving higher, net income holding relatively steady and the share price already up in recent weeks, the key question now is whether Tractor Supply still offers value or if the market is already pricing in future growth.

Most Popular Narrative: 4% Undervalued

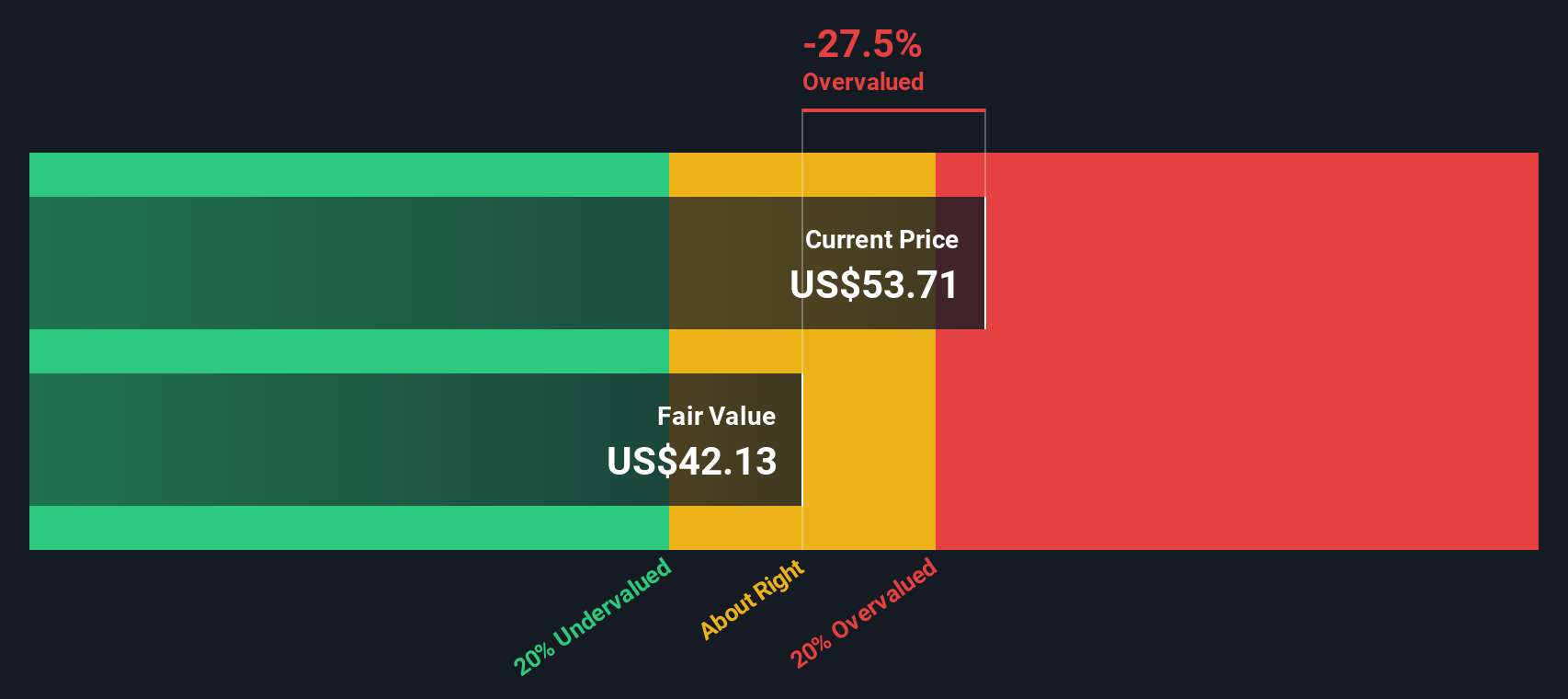

At a last close of $55.28 against a narrative fair value of $57.59, Tractor Supply’s story hinges on how future growth, margins and store expansion play out.

Strong transaction growth, unit growth in consumable, usable, and edible categories, and record customer retention indicate sustained demand, likely bolstering future revenue.

Tractor Supply's success with strategic initiatives like their Chick Days and direct sales efforts, including PetRx integration, may enhance customer engagement and drive revenue and margin improvements.

Curious what is baked into that fair value? Revenue stepping up, margins edging higher, and a richer earnings multiple all sit at the core of this narrative.

Result: Fair Value of $57.59 (UNDERVALUED)

However, there are still pressure points, with softer comparable store sales and big ticket weakness that could challenge the earnings and margin assumptions behind this view of the shares being 4% undervalued.

Another View: Cash Flows Point to a Richer Price

While the fair value narrative sits at $57.59 and frames Tractor Supply as 4% undervalued, our DCF model paints a different picture, with a future cash flow value of $34.08 per share. That gap suggests the market could be pricing the cash flows quite optimistically, so which story do you trust more?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Tractor Supply for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 868 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Tractor Supply Narrative

If you look at the numbers and come to a different conclusion, or prefer to test your own assumptions, you can build a full narrative yourself in just a few minutes with Do it your way.

A great starting point for your Tractor Supply research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Tractor Supply has sharpened your focus, do not stop here. Use the Simply Wall Street Screener to uncover more ideas that match how you like to invest.

- Hunt for potential mispricings with these 868 undervalued stocks based on cash flows that line up strong cash flow forecasts with current share prices.

- Ride the wave of artificial intelligence trends by checking out these 27 AI penny stocks shaping how data and automation show up in everyday businesses.

- Get ahead of the next payment and blockchain shifts with these 19 cryptocurrency and blockchain stocks that tie real companies to digital asset themes.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.