A Look At Tractor Supply (TSCO) Valuation After Truist Downgrade And Softer Demand Signals

Tractor Supply Company TSCO | 43.82 | -1.59% |

Why a downgrade is in focus even as Tractor Supply keeps expanding

Tractor Supply (TSCO) is in the spotlight after Truist Securities cut its rating from Buy to Hold, citing proprietary card data that points to broadly weaker sales and softer demand trends.

This comes just as the company continues to add new locations, including its 2,400th store in Aiken, South Carolina, which is part of a plan to open 100 new stores by the end of 2026.

At a share price of US$51.01, Tractor Supply has had a softer run recently, with a 30 day share price return of a 4.64% decline and a 1 year total shareholder return of a 3.34% decline, hinting that the recent analyst downgrade and questions around demand have cooled momentum despite ongoing store openings and expansion efforts.

If Tractor Supply’s recent moves have you thinking about what else is out there, it could be a good moment to check out auto manufacturers as another way to scan the market.

With the shares under pressure, analysts turning cautious and the stock trading below the latest Truist price target, the key question is whether Tractor Supply is mispriced value or if the market already reflects its future growth.

Most Popular Narrative: 19.2% Undervalued

Compared with Tractor Supply’s last close of US$51.01, the most followed narrative points to a higher fair value, built on detailed revenue and earnings assumptions.

The analysts have a consensus price target of $62.593 for Tractor Supply based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $70.0, and the most bearish reporting a price target of just $47.0.

Want to see what kind of revenue path and margin profile are used to support that higher value, and which future P/E multiple ties it all together? The full narrative sets out a detailed earnings roadmap, share count changes and a specific discount rate that could change how you look at today’s price.

Result: Fair Value of $63.15 (UNDERVALUED)

However, that upside view could be tested if softness in comparable store sales and pressure on big ticket categories persist longer than analysts currently bake into their models.

Another View: Multiples Point to a Richer Price

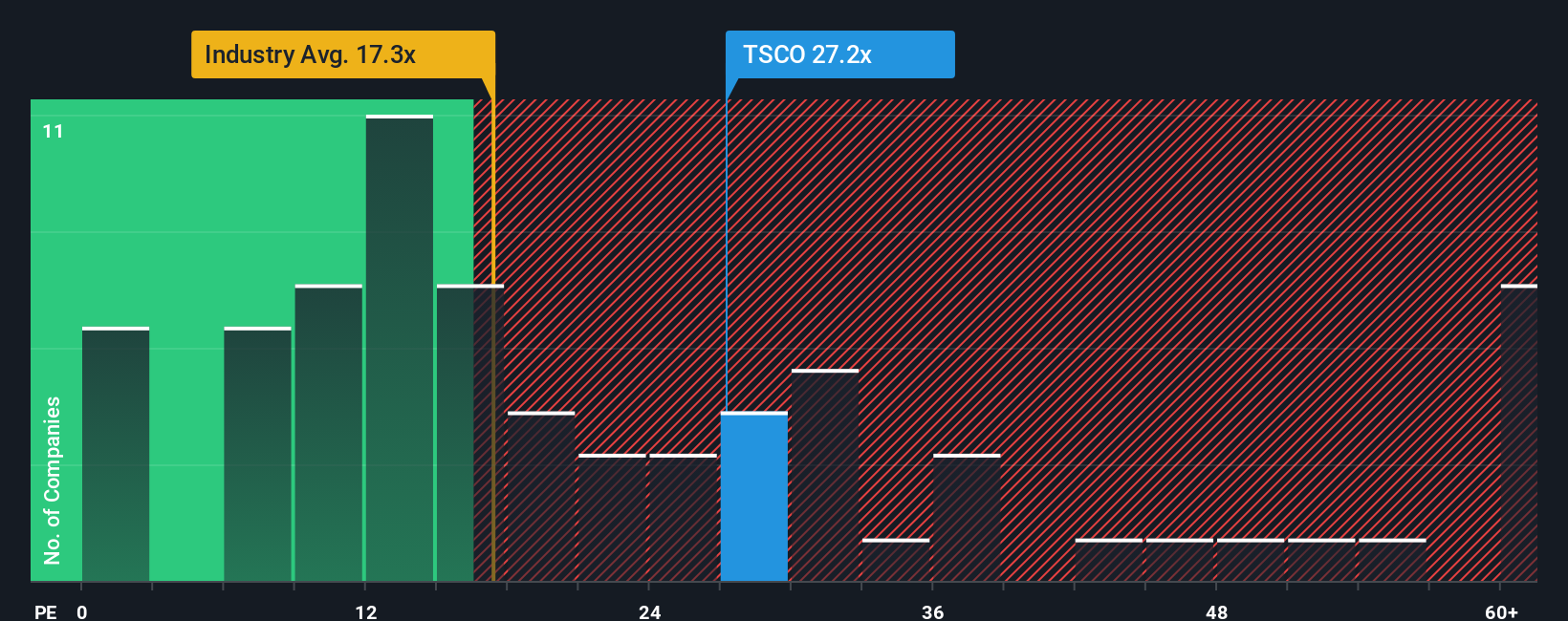

While the narrative-based fair value of US$63.15 suggests upside, the current P/E of 24.4x tells a different story. It sits above both the US Specialty Retail industry at 21x and the fair ratio of 18x. This implies there is less room for error if growth or margins fall short.

Build Your Own Tractor Supply Narrative

If you are not on board with these views or simply prefer to run the numbers yourself, you can build a fresh thesis in minutes with Do it your way.

A great starting point for your Tractor Supply research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Tractor Supply is on your radar but you are keen to broaden your watchlist, now is the time to scan other angles before the next move passes you by.

- Zero in on value by checking these 863 undervalued stocks based on cash flows that line up quality fundamentals with prices that may not fully reflect them yet.

- Ride the AI trend by reviewing these 24 AI penny stocks that are using artificial intelligence across everything from software tools to automation.

- Tap into income potential through these 12 dividend stocks with yields > 3% that offer yields above 3% and may suit a cash flow focused portfolio.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.