A Look At TransDigm Group’s Valuation As Raised 2026 Guidance Follows Solid First Quarter Results

TransDigm Group Incorporated TDG | 1167.00 | -0.53% |

TransDigm Group (TDG) has just raised its fiscal 2026 earnings guidance alongside reporting first quarter sales of US$2,285 million and net income of US$445 million, which is putting fresh attention on its core aerospace franchises.

Even with the raised fiscal 2026 guidance and ongoing acquisitions such as Jet Parts Engineering, Victor Sierra and Stellant Systems, TransDigm's recent share price performance has cooled. The 7 day share price return shows a 9.95% decline and the 30 day share price return shows a 7.65% decline, while the 1 year total shareholder return of 3.51% and very large 5 year total shareholder return of 168.30% show that longer term holders have still seen meaningful gains.

If this aerospace update has you thinking about where else capital could work hard, take a look at our screener of 22 top founder-led companies for fresh ideas beyond the usual names.

So with earnings guidance lifted, recent acquisitions bedding down and the share price sliding over the past month, is TransDigm quietly slipping into undervalued territory, or is the market already paying up for all that future growth?

Most Popular Narrative: 19% Undervalued

Compared to TransDigm Group's last close at $1,285.53, the most followed narrative assigns a fair value of about $1,586, which points to a meaningful valuation gap and puts the spotlight firmly on its cash generation story.

Ongoing industry trends toward outsourcing parts manufacturing by major OEMs are creating opportunities for specialized suppliers like TransDigm to capture additional content per aircraft, ultimately boosting long term revenue growth, EBITDA margins, and free cash flow generation.

Curious what kind of revenue trajectory, margin profile, and earnings multiple it takes to reach that fair value number, and how much optimism is baked in.

Result: Fair Value of $1,586 (UNDERVALUED)

However, there are still pressure points, including high leverage and reliance on legacy aftermarket platforms. These factors could challenge margins and make those cash flows less predictable.

Another View: P/E Ratios Send A Caution Flag

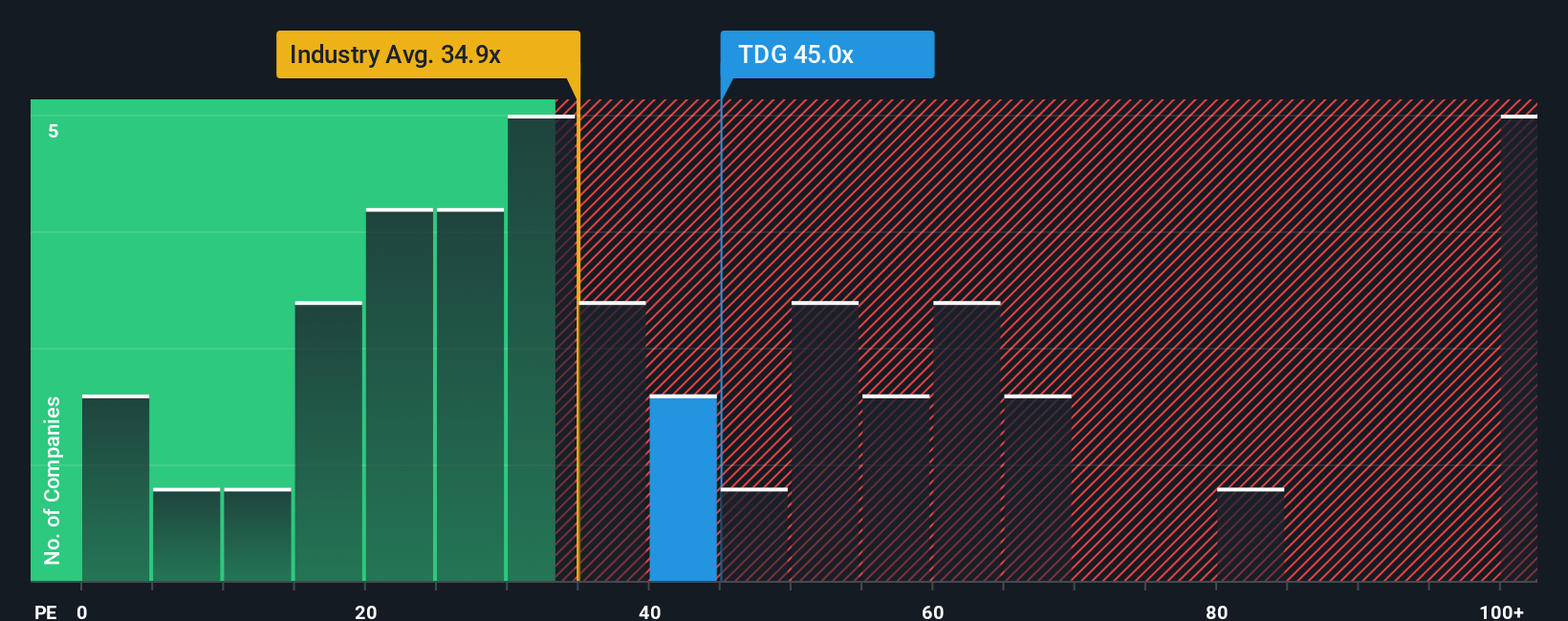

That 19% “undervalued” call rests on a cash flow narrative, but the P/E ratio paints a tighter picture. TransDigm trades on 40.2x earnings versus a fair ratio of 37.3x. It also sits above the peer average of 37.5x and roughly in line with the US Aerospace & Defense industry at 41.3x. This points to limited room for error if growth or margins come in softer than expected. So is this really a valuation gap, or simply a full price for a quality aerospace compounder?

Build Your Own TransDigm Group Narrative

If you are not fully aligned with these views, or simply prefer to test your own assumptions against the numbers, you can build a custom thesis in just a few minutes by starting with Do it your way.

A great starting point for your TransDigm Group research is our analysis highlighting 4 key rewards and 4 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If TransDigm has sharpened your thinking, do not stop here. Broadening your watchlist with high quality ideas can be just as valuable as a single stock pick.

- Target dependable compounding by scanning for quality companies trading below what our models suggest using the 52 high quality undervalued stocks that filters for strong fundamentals at appealing prices.

- Prioritise resilience by focusing on businesses with strong finances through the solid balance sheet and fundamentals stocks screener (45 results), designed to spotlight companies that keep debt and liquidity in check.

- Hunt for fresh opportunities before they go mainstream with our screener containing 24 high quality undiscovered gems, which surfaces under the radar names with robust financial profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.