A Look At Transocean (RIG) Valuation After New Brazil And Norway Rig Contracts

Transocean Ltd. RIG | 6.59 | +1.38% |

Transocean (RIG) shares are in focus after the company disclosed new work for two offshore rigs, with contracts in Brazil and Norway adding approximately $168 million of firm backlog and extending visibility on future drilling activity.

The new rig awards arrive after a strong run in the share price. Transocean’s 90 day share price return of 36.86% contrasts with a more modest 0.71% year to date gain, while the 1 year total shareholder return of 4.40% sits against a 3 year total shareholder loss of 24.56% and a 5 year total shareholder return of 30.18%. This suggests that recent momentum has picked up from a mixed longer term record.

If this kind of contract news has caught your eye, it could be a good moment to see what else is moving among aerospace and defense stocks as another way to find opportunity.

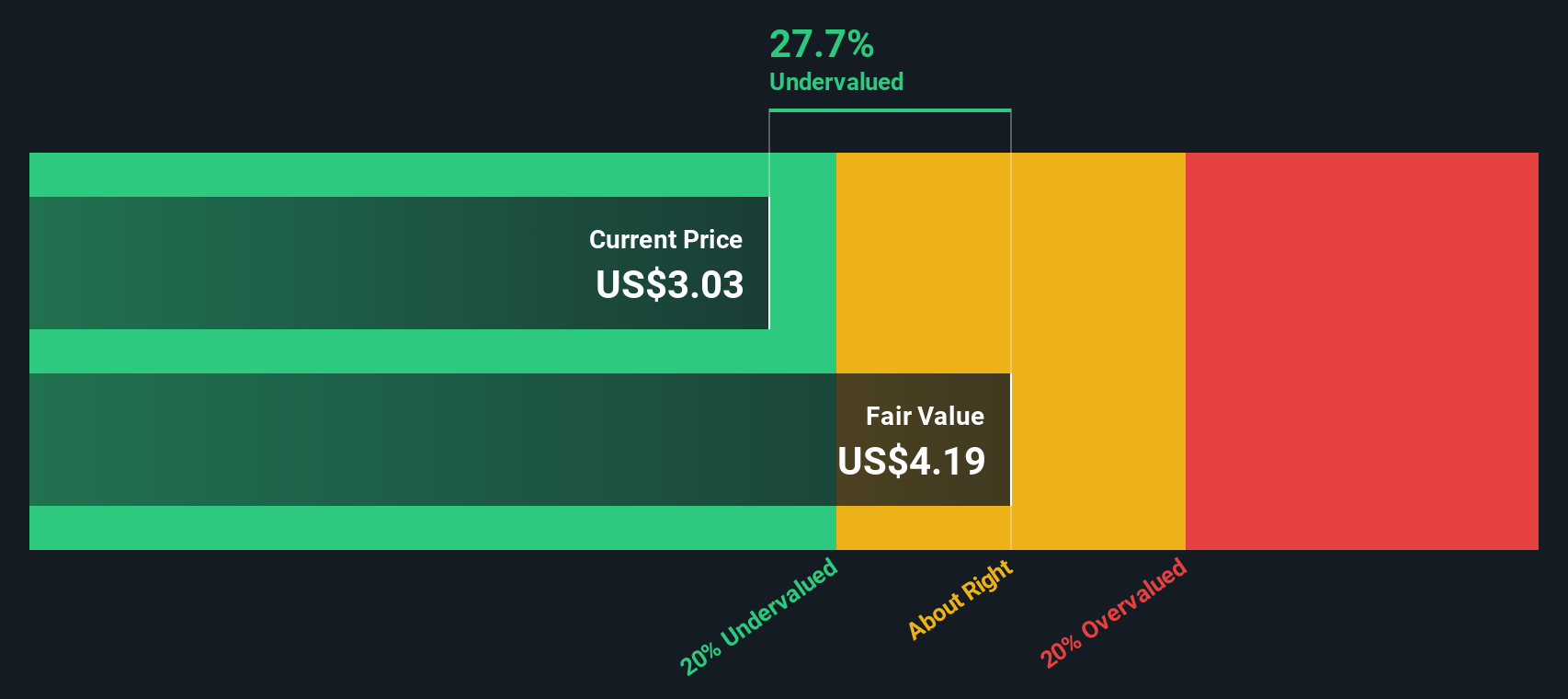

With shares up 36.86% over 90 days, but trading near analysts’ price target and at an estimated 32.32% intrinsic discount, is Transocean still underappreciated, or is the market already pricing in future growth?

Most Popular Narrative: 2.5% Overvalued

With Transocean last closing at US$4.27 against a narrative fair value of about US$4.17, the valuation gap is narrow and hinges on some specific performance assumptions.

Transocean's industry leading backlog (~US$7 billion) with major E&P clients provides strong revenue visibility and cash flow stability, enabling efficient conversion of backlog into revenue and supporting rapid deleveraging, which will positively impact net debt levels and interest expense.

Curious how a company with recent losses ends up with a premium earnings multiple in this narrative? The story leans heavily on a margin reset, a sharp swing in profitability and a future valuation framework more commonly associated with faster growing sectors.

Result: Fair Value of US$4.17 (OVERVALUED)

However, there are still clear pressure points, including Transocean’s heavy debt load and interest costs, as well as the risk that softer dayrates or utilization could weaken backlog conversion.

Another View: DCF Points the Other Way

Here is where things get interesting. While the narrative fair value of about US$4.17 suggests Transocean looks slightly overvalued at US$4.27, our DCF model puts fair value much higher at US$6.31, implying the shares trade at a 32.3% discount. Which signal do you trust more: the story or the cash flow math?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Transocean for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 879 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Transocean Narrative

If you see the numbers differently, or prefer to test your own assumptions, you can build a customised view in a few minutes here: Do it your way.

A great starting point for your Transocean research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Transocean has sharpened your interest, do not stop here. Widen your search and give yourself more options before your next portfolio move.

- Spot potential high risk high reward opportunities early by scanning these 3530 penny stocks with strong financials that already show stronger financial underpinnings than many expect from this corner of the market.

- Ride the momentum of breakthrough technology by zeroing in on these 26 AI penny stocks that tie artificial intelligence to real business models, not just headlines.

- Focus on value first by filtering for these 879 undervalued stocks based on cash flows that current prices suggest may offer more cash flow for every dollar you put to work.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.