A Look At Tri Pointe Homes (TPH) Valuation After Weaker 2025 Results And New Community Launches

Tri Pointe Homes, Inc. TPH | 46.75 | +0.43% |

Tri Pointe Homes (TPH) is back in focus after reporting fourth quarter and full year 2025 results that showed lower revenue and net income year over year, along with new community launches in Utah.

Despite softer 2025 earnings, Tri Pointe Homes’ 30 day share price return of 30.85% and 90 day share price return of 37.73% suggest recent momentum, while the 5 year total shareholder return of 132.7% reflects a strong longer term outcome.

If this homebuilder’s move has caught your attention, it could be a good moment to broaden your search with our screener of 20 top founder-led companies to see what else stands out.

With earnings and revenue lower year over year, but the share price up sharply and trading only slightly below the analyst price target, the key question is whether Tri Pointe Homes is still mispriced or if the market is already assuming brighter days ahead.

Most Popular Narrative: 1.3% Undervalued

With Tri Pointe Homes last closing at $46.40 against a narrative fair value of $47.00, the current pricing sits almost on top of that projected level while still implying a small discount.

Fair Value: Updated to $47.00 from $38.20 to align the model with the announced $47 per share cash offer.

Discount Rate: Reduced slightly from 9.57% to 9.28%, reflecting a modest shift in the risk assumptions used in the valuation work.

Curious what justifies that higher fair value right as earnings and revenue are expected to soften? The narrative leans on adjusted revenue decline, firmer margins, and a richer future earnings multiple. Want to see how those ingredients are combined into that $47 figure and what that implies beyond the current deal price?

Result: Fair Value of $47 (UNDERVALUED)

However, this hinges on Tri Pointe avoiding deeper order softness and further margin pressure in key Western markets, where affordability issues and impairments have already been flagged.

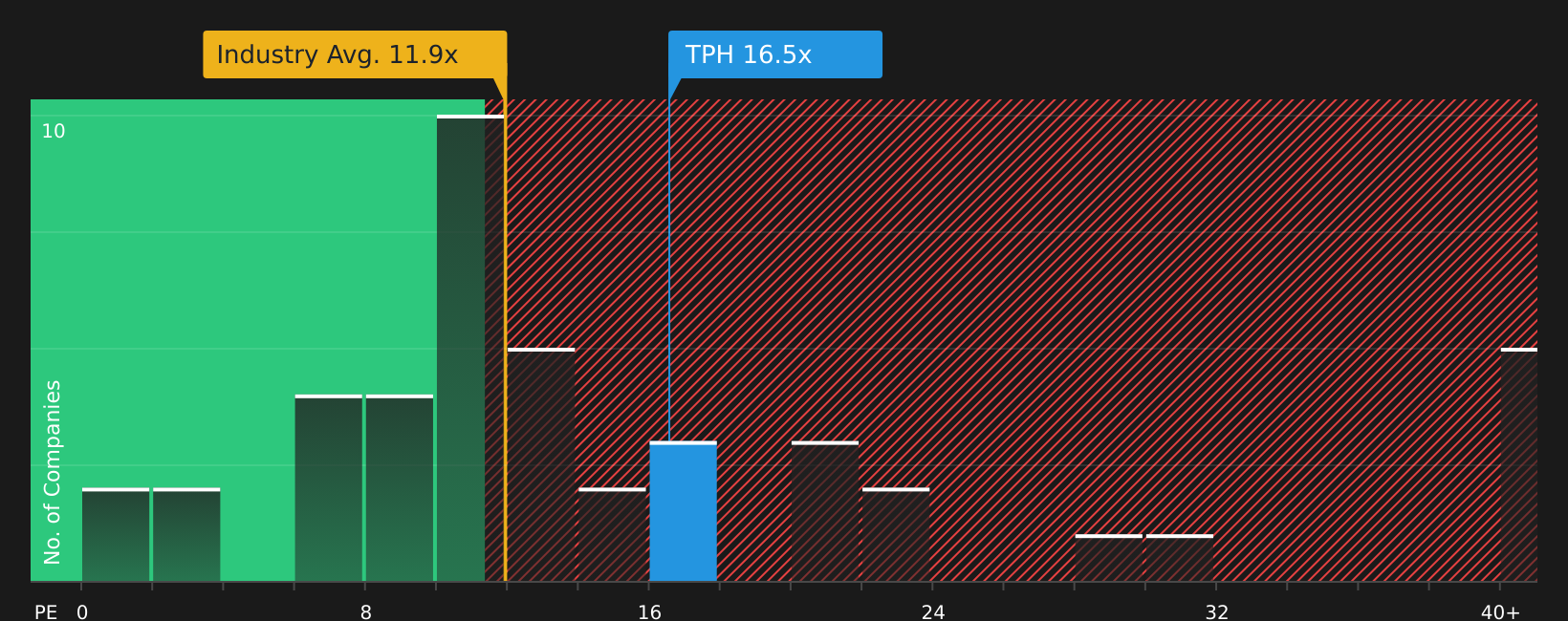

Another View: Multiples Point To A Richer Price

While the narrative fair value sits close to the $47 cash offer, the current P/E of 16.4x stands well above the US Consumer Durables industry at 11.8x, the peer average at 12.2x, and even the fair ratio of 11.2x. That gap suggests less cushion if sentiment cools. Is the premium worth paying for you?

Next Steps

If this mix of positives and concerns feels finely balanced, it makes sense to look at the data yourself and move promptly while views are still forming. You can start with our breakdown of 1 key reward and 3 important warning signs.

Looking for more investment ideas?

If you are serious about sharpening your portfolio beyond a single stock story, now is the time to put the Simply Wall St screener to work before other investors do.

- Target potential value opportunities by checking companies that appear attractively priced with the help of our 48 high quality undervalued stocks based on fundamentals.

- Prioritise resilience by scanning companies with stronger balance sheets and cleaner financial profiles using our solid balance sheet and fundamentals stocks screener (41 results).

- Hunt for underfollowed names that may not be on every watchlist yet by reviewing our screener containing 23 high quality undiscovered gems backed by data driven filters.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.