A Look At Tripadvisor (TRIP) Valuation As AI Travel Answers Pressure Its Traffic And Business Model

TripAdvisor, Inc. TRIP | 0.00 |

Tripadvisor (TRIP) is under pressure after CEO Matt Goldberg warned that AI driven travel answers are cutting into the company’s visitor traffic, raising fresh questions about the resilience of its online travel model.

The stock has been under pressure for some time, with the share price falling 31.4% year to date and the 1 year total shareholder return down 29.9%. The recent 7 day share price rebound of 8% suggests short term bargain hunting rather than strong momentum.

If AI is changing how travelers research trips, it can help to widen your watchlist beyond a single online travel stock and scan other technology driven opportunities using the 34 AI small caps

With Tripadvisor shares down sharply over 1, 3 and 5 years, yet trading at a sizeable discount to some analyst targets and intrinsic estimates, is the stock now mispriced, or is the market already bracing for weaker future growth?

Most Popular Narrative: 30.2% Undervalued

The most widely followed valuation narrative puts Tripadvisor’s fair value at $14.38, well above the last close at $10.04. This raises clear questions about what assumptions sit behind that gap.

The analysts have a consensus price target of $18.162 for Tripadvisor based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $25.0, and the most bearish reporting a price target of just $13.5.

Want to see what is driving that valuation spread? The narrative leans heavily on compounding earnings, firmer margins and a richer future profit multiple. Curious which exact combinations of revenue growth, profitability and discount rate get you to that $14.38 figure and beyond? The full narrative lays out the playbook in detail.

Result: Fair Value of $14.38 (UNDERVALUED)

However, that upside story can unravel quickly if organic traffic keeps sliding or if competitors, including super apps and direct bookings, continue chipping away at Tripadvisor’s relevance.

Another View: Earnings Multiple Paints A Tougher Picture

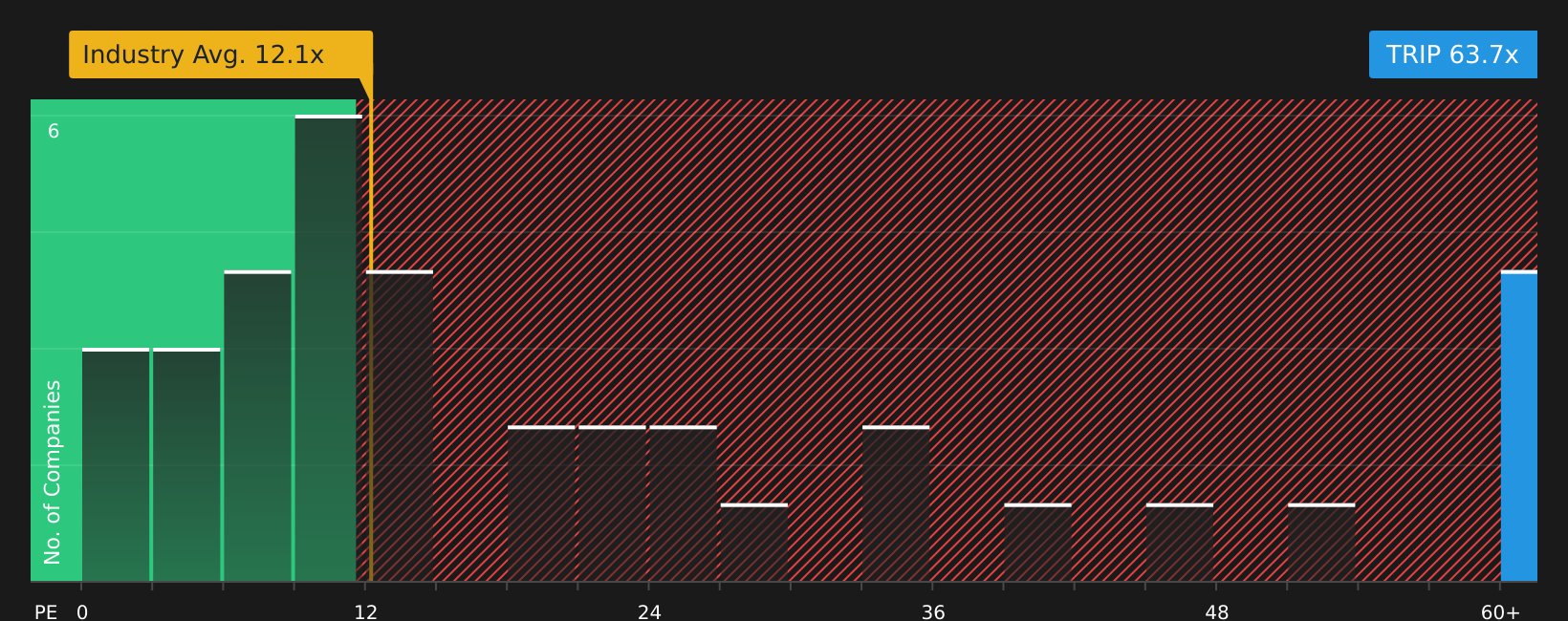

The earlier fair value of $14.38 suggests Tripadvisor looks 30.2% undervalued, but the earnings multiple tells a different story. At a P/E of 62.8x versus 12.3x for the US Interactive Media and Services industry and a 9x peer average, the stock is priced at a much richer level than many direct comparables.

Even against the Simply Wall St fair ratio of 26.9x, Tripadvisor’s current P/E is more than double, which points to meaningful valuation risk if earnings or sentiment disappoint. With such a wide gap between the narrative fair value and what the multiple implies, which signal do you trust more for your own process?

Next Steps

With sentiment clearly split between risk and potential upside, it makes sense to move fast, review the underlying data yourself, and weigh both sides. To see what stands out on each side of the ledger, take a closer look at the 2 key rewards and 2 important warning signs

Looking for more investment ideas?

If Tripadvisor is on your radar, do not stop there. Broadening your watchlist can surface opportunities you might regret missing later.

- Zero in on potential mispricings by scanning companies flagged as 46 high quality undervalued stocks.

- Strengthen your defensive side by reviewing the 65 resilient stocks with low risk scores that aim to limit downside when conditions get choppy.

- Spot future standouts early by checking the screener containing 22 high quality undiscovered gems before they attract wider attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.