A Look At Tronox Holdings (TROX) Valuation After Truist Downgrade And Earnings Concerns

Tronox Holdings Plc TROX | 0.00 |

Tronox Holdings (TROX) is back in focus after Truist cut its rating to Sell, citing the risk of softer fiscal Q2 guidance, cost pressures, and an unfavorable geographic mix that may weigh on near term earnings.

Despite the downgrade, Tronox’s share price has been strong, with a 10.13% 1 month share price return and a 70.46% 3 month share price return. However, the 5 year total shareholder return of a 46.69% loss shows the longer term recovery journey is still incomplete.

If this kind of rebound has your attention, it could be a good moment to broaden your search with our screener covering 8 top copper producer stocks

With Tronox posting a very large year to date return but still carrying a 5 year total shareholder return loss, the key question now is whether the current share price reflects a bargain or whether the market is already pricing in future growth.

Most Popular Narrative: 69.1% Overvalued

The most followed valuation narrative puts Tronox’s fair value at $6.11, well below the last close at $10.33, which creates a wide gap for investors to assess.

Industry supply/demand dynamics are improving due to significant capacity reductions (over 700,000 tons) since 2023 and continuing rationalization, setting the stage for less price volatility and a margin recovery as end-market demand stabilizes or improves, with Tronox well positioned to capture increased earnings from a tighter supply landscape.

Curious what earnings power and margin profile are built into that fair value gap? The narrative leans heavily on measured growth assumptions and a re rated profit multiple. The key question is how those ingredients combine over time to bridge today’s price and that model.

Result: Fair Value of $6.11 (OVERVALUED)

However, there is still the risk that high net leverage of about $2.9b, along with exposure to regulatory and environmental costs, could pressure margins and cash flow.

Another Way to Look at Value

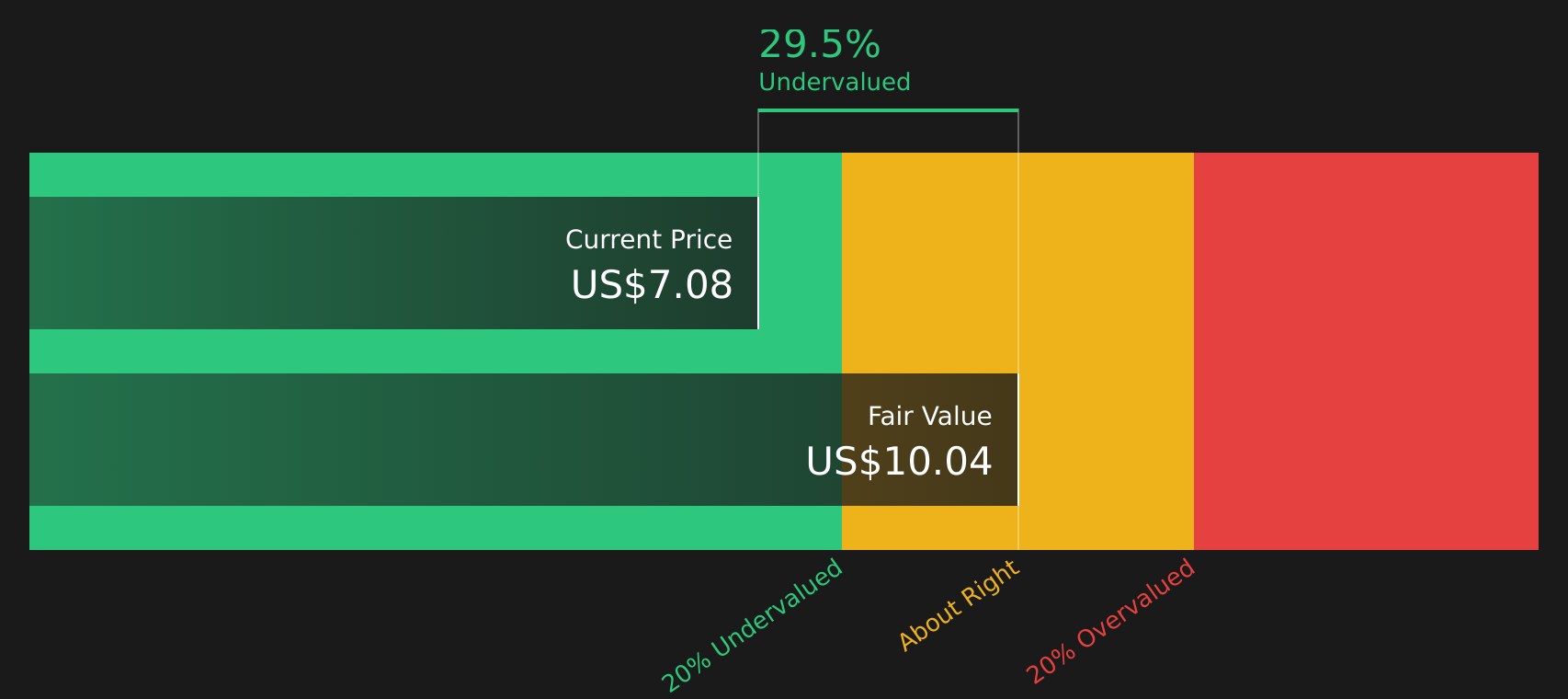

The popular narrative pegs fair value at $6.11 and calls Tronox overvalued, but the Simply Wall St DCF model points the other way, with an estimate of $13.01. That is a wide gap, which raises the question of which set of assumptions you are more comfortable with.

To see how that DCF result is built up, and what has the biggest impact if it changes, take a closer look at the model output here: Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Tronox Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 51 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals on value and sentiment, this is a good time to look through the details yourself and move quickly to shape your own stance using the 1 key reward and 4 important warning signs.

Looking for more investment ideas?

If Tronox has you thinking about what else might be worth your attention, now is the time to scan a wider field of opportunities and stay ahead.

- Focus on value potential by checking companies that combine quality fundamentals with attractive pricing through the 51 high quality undervalued stocks.

- Strengthen your income focus and assess businesses offering higher yields and resilient payouts using the 13 dividend fortresses.

- Prioritize resilience and capital preservation by reviewing companies screened for lower risk profiles via the 67 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.