A Look At Truist Financial’s Valuation As Q4 Results And New AI Platform Signal Steady Progress

TRUIST FINANCIAL CORPORATION TFC | 49.43 | -0.32% |

Truist Financial (TFC) is back in focus after Q4 results that broadly aligned with analyst expectations and the launch of a new AI driven integrated receivables platform aimed at tightening operations for commercial and corporate clients.

The recent Q4 update and AI receivables launch come on the back of firm momentum, with a 24.74% 3 month share price return and a 22.84% 1 year total shareholder return from a latest share price of US$55.81.

If Truist’s use of AI has caught your attention, it could be a good moment to look beyond the big banks and check out 56 profitable AI stocks that aren't just burning cash as a starting list of ideas.

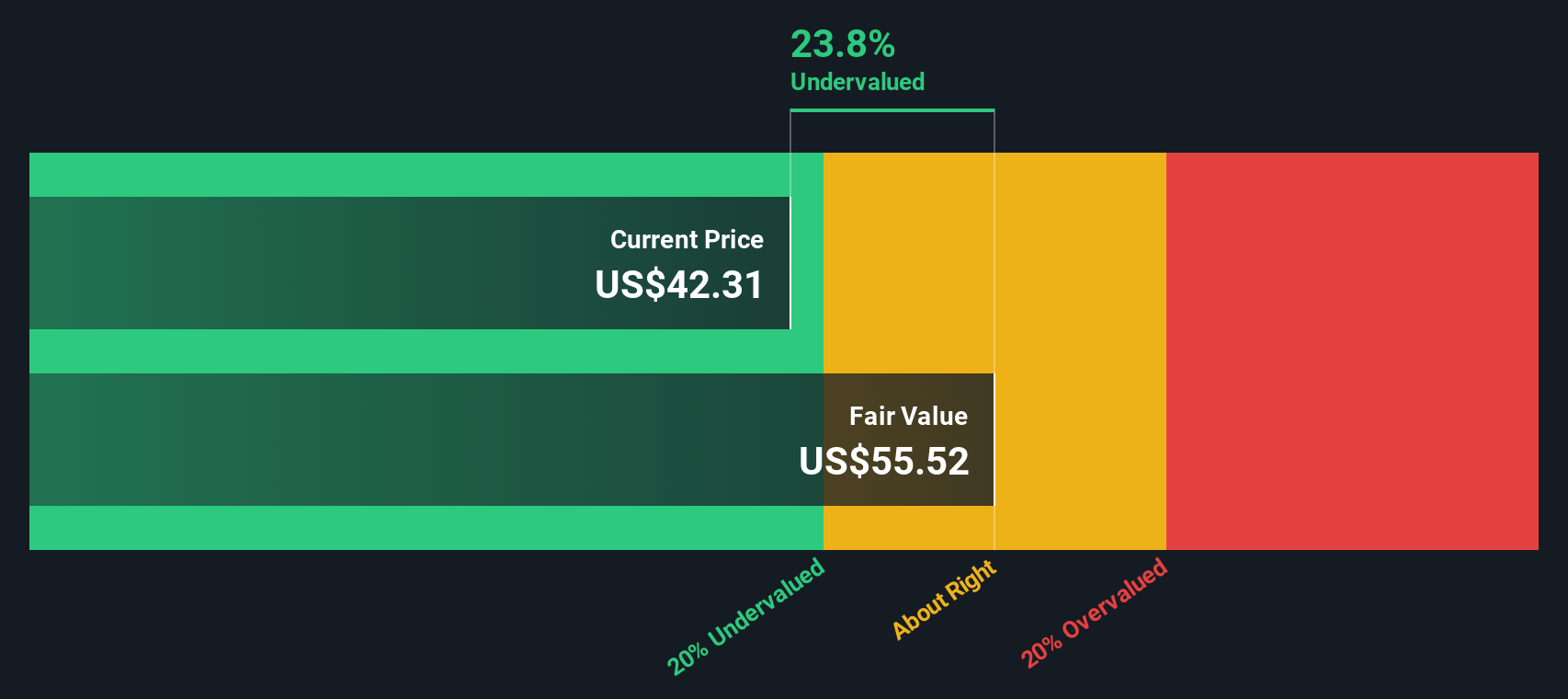

With Truist trading near its US$56 analyst price target but showing a 19.58% intrinsic discount, the key question is whether recent gains leave more room to run or if the market is already pricing in future growth.

Most Popular Narrative: 0.9% Overvalued

Truist’s recent close of $55.81 sits slightly above the most followed fair value estimate of about $55.31, which is built on detailed revenue, margin and return assumptions.

Recent research points to a generally constructive tone on Truist Financial, with several bullish analysts raising price targets and upgrading ratings, while a smaller group strikes a more cautious note around guidance and execution risk.

Curious what kind of revenue path, profit margins and future earnings multiple support that almost one to one match with today’s price? The narrative leans on specific growth rates, a tighter cost base and capital return plans. It also builds in a future valuation multiple that differs from what many investors might expect for a large regional bank. Want to see exactly which assumptions hold this fair value together and how sensitive they are to small changes?

Result: Fair Value of $55.31 (OVERVALUED)

However, heavy spending on branches and Truist’s commercial real estate exposure could pressure margins and asset quality if conditions turn against those parts of the business.

Another Angle On Value

The narrative model pegs Truist’s fair value at about $55.31 and labels the current $55.81 price as slightly overvalued. Our DCF model, however, points to future cash flows worth about $69.40 per share, or roughly a 19.6% gap. Which view do you think tells the more useful story?

Build Your Own Truist Financial Narrative

If some of these assumptions do not sit right with you, or you prefer to lean on your own research, you can spin up a personalised Truist view in just a couple of minutes: Do it your way.

A great starting point for your Truist Financial research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Ready To Hunt For More Investment Ideas?

If Truist has sharpened your thinking, do not stop here. Use the Simply Wall St screener to uncover other ideas that fit your style.

- Target value first by scanning a curated set of 53 high quality undervalued stocks that pair quality fundamentals with prices that may not fully reflect them.

- Prioritise resilience by zeroing in on 86 resilient stocks with low risk scores that score well on our risk framework and may suit a more cautious approach.

- Get ahead of the crowd by reviewing a screener containing 24 high quality undiscovered gems that most investors are not paying attention to yet.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.