A Look At UGI (UGI) Valuation As It Reshapes Business And Exits Its Electric Division

UGI Corporation UGI | 0.00 |

UGI (UGI) is in the middle of a broad reshaping of its business, from selling its electric division and building out natural gas infrastructure to expanding online propane sales and delivering on early ESG commitments.

Recent moves like the electric division sale, new gas infrastructure projects in Pennsylvania and online AmeriGas propane sales have come alongside a 1 month share price return of about 7%, while the year to date share price is still down around 8%. The 3 year total shareholder return of roughly 41% points to stronger gains over a longer horizon.

If UGI’s reshaping has you thinking about where the next opportunity might come from in energy infrastructure, it could be a good time to scan 34 power grid technology and infrastructure stocks

With UGI’s shares up about 7% over the past month but still down around 8% year to date, the key question is whether the recent restructuring is already reflected in the price or if the market is underestimating the company’s potential.

Most Popular Narrative: 20.2% Undervalued

At a last close of $34.57 versus a narrative fair value of $43.33, the current UGI price sits well below what the most widely followed view suggests is reasonable, which sets up a clear tension between market pricing and that narrative.

Strategic investments in renewable natural gas (RNG) projects, bonus depreciation potential, and stronger regulatory incentives through recent legislation (e.g., the One Big Beautiful Bill Act) are expected to drive long-term EBITDA growth and improve net margins.

The fair value estimate rests on a clear blueprint for steadier revenue growth, higher profitability and a future earnings multiple that remains below the sector benchmark. It raises questions about which assumptions carry the most weight in that calculation and how they connect back to Pennsylvania rate decisions and energy transition spending.

Result: Fair Value of $43.33 (UNDERVALUED)

However, there is still a real risk that weaker propane demand at AmeriGas or less favorable Pennsylvania rate outcomes could undercut the earnings path behind that fair value.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

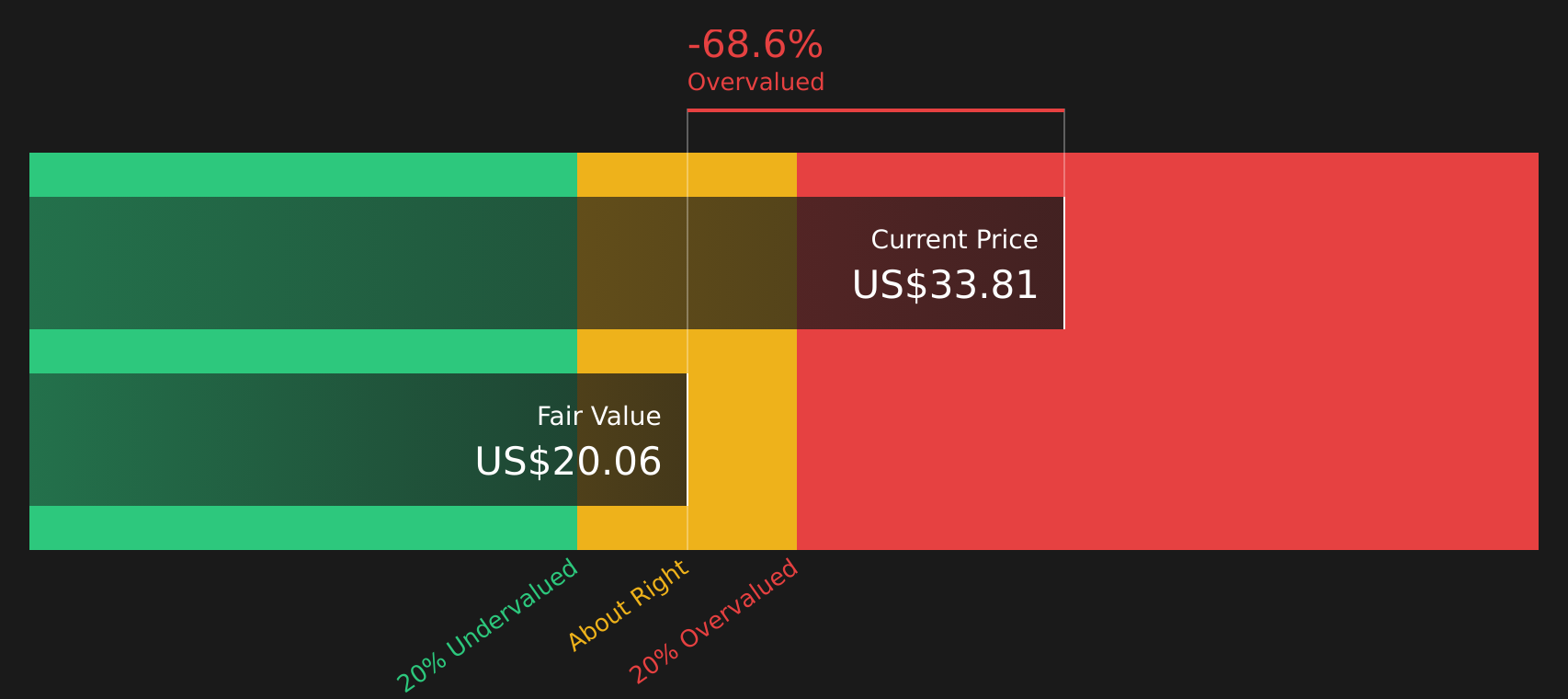

Another View: Cash Flows Paint a Different Picture

While the analyst narrative sees UGI trading about 20% below a fair value of $43.33 based on earnings and multiples, the Simply Wall St DCF model is more cautious, with an estimate of future cash flow value around $20.11 per share. On that basis, the stock appears expensive.

This gap between earnings-based upside and a DCF that points to overvaluation puts the focus on which assumptions investors rely on more: the cash generation path, or the earnings and multiple approach.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out UGI for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 47 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With such a mixed picture on value, sentiment can shift quickly. Spend some time with the full data and decide where you stand using the 5 key rewards and 2 important warning signs.

Looking for more investment ideas?

If UGI has sharpened your focus on value and resilience, do not stop here. Broaden your watchlist with a few targeted stock ideas using these screeners.

- Target potential mispricings by checking companies flagged as 47 high quality undervalued stocks where strong fundamentals and attractive pricing could line up.

- Strengthen your income stream by reviewing stocks highlighted as 10 dividend fortresses that offer higher yields with a focus on sustainability.

- Reduce portfolio stress by scanning for 63 resilient stocks with low risk scores that pair lower risk profiles with solid business characteristics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.