A Look At Ultra Clean Holdings (UCTT) Valuation As Analyst Optimism And Zacks Rank #1 Fuel Interest

Ultra Clean Holdings, Inc. UCTT | 0.00 |

Ultra Clean Holdings (UCTT) is back on investor radars after a surge in analyst optimism, with Wall Street raising earnings per share estimates and awarding the stock a top Zacks Rank #1 rating.

The stock’s share price return has been strong over longer periods, with a 90 day share price return of 36.8% and a year to date share price return of 207.5%. The 1 year total shareholder return sits at 321.53%, suggesting momentum that aligns with the recent shift in analyst sentiment.

If the recent move in semiconductor equipment stocks has caught your attention, it may be a good moment to scan the wider opportunity set through our 46 AI infrastructure stocks

With Ultra Clean trading at US$84.01 against an analyst price target of US$104.40 and a value score of 4, should you view this as an underappreciated semiconductor supplier, or has the market already priced in future growth?

Most Popular Narrative: 3% Overvalued

Ultra Clean’s most followed narrative pegs fair value at $81.25, slightly below the last close at $84.01. This sets up a tight valuation debate.

Ongoing organizational flattening, cost reduction initiatives, and factory/site consolidation are producing tangible decreases in OpEx, with further improvements expected by Q4, providing sustainable margin enhancement as industry volumes recover. Progress in vertical integration, particularly the Fluid Solutions business unit, along with deployment of company-wide SAP systems, is set to improve operational efficiency and streamline customer engagement, driving higher margin mix and improved earnings beginning in early 2026.

Want to see what sits behind this tight fair value band? The projections blend revenue growth, slimmer costs and a higher future earnings multiple. Curious which levers matter most.

Result: Fair Value of $81.25 (OVERVALUED)

However, there are still two clear swing factors: prolonged industry demand weakness that keeps revenue below prior capacity expectations, and high reliance on a few large customers.

Another View on Value

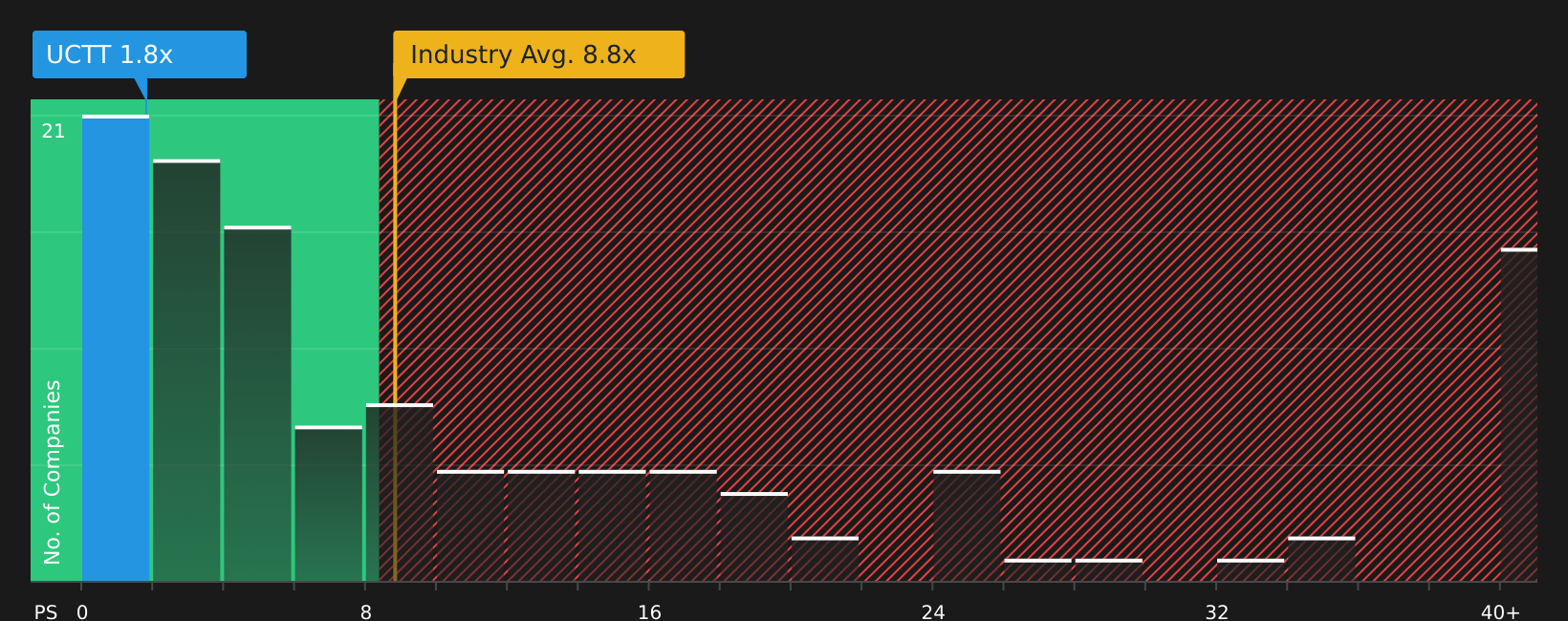

While the narrative model points to fair value around $81.25 and labels Ultra Clean as slightly overvalued at $84.01, the current P/S of 1.8x sits well below the US Semiconductor industry at 8.8x and a fair ratio estimate of 2.8x. This raises the question of whether sentiment or fundamentals catch up first.

For a closer look at what the numbers imply if the market moves toward that fair ratio, tap into the See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With sentiment clearly split between risks and rewards, now is the time to look through the full picture yourself and decide where you stand. To balance both sides before making your next move, take a closer look at the 3 key rewards and 2 important warning signs

Looking for more investment ideas?

If you stop here, you might miss stocks that better match your goals, so take a few minutes to scan other opportunities that fit your style.

- Target quality at a discount by reviewing our list of 49 high quality undervalued stocks that combine fundamentals with pricing that some investors may find attractive.

- Prioritize resilience by checking out 67 resilient stocks with low risk scores, focused on companies with lower risk scores that may suit more cautious portfolios.

- Spot potential early standouts through the screener containing 21 high quality undiscovered gems, highlighting lesser known stocks with strong underlying metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.