A Look At Uniti Group (UNIT) Valuation After Major Fiber Contract Win And Brian Higgins Endorsement

Uniti Group Inc. UNIT | 0.00 |

Uniti Group (UNIT) has returned to focus after securing its largest long haul fiber contract with a major hyperscaler and drawing fresh attention from billionaire investor Brian Higgins as a top pick.

These headlines arrive after a sharp move in the stock, with a 30 day share price return of 13.94% and a 90 day share price return of 45.31%. The 3 year total shareholder return of 118.65% suggests longer term holders have already experienced strong compounding, and shorter term momentum has recently picked up.

If Uniti’s recent fiber wins have your attention, it can be useful to see what else is moving in related infrastructure and connectivity. Take a look at 35 power grid technology and infrastructure stocks

With UNIT now at US$11.77, a 3 year total return above 100%, and revenue growth paired with weaker net income growth, it is fair to ask: is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 38.5% Overvalued

Analysts following Uniti Group see fair value at $8.50 per share, which sits well below the recent $11.77 close and frames a cautious valuation story built on detailed growth and margin assumptions.

Analysts are assuming Uniti Group's revenue will grow by 19.1% annually over the next 3 years.

Analysts are not forecasting that Uniti Group will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Uniti Group's profit margin will increase from 55.9% to the average US Telecom industry of 12.9% in 3 years.

Want to see what sits behind that gap between today’s price and the $8.50 fair value? The narrative leans on ambitious revenue compounding, a reset of margins, and a future earnings multiple that has to line up with those moving pieces. Curious which specific growth, profitability, and discount rate assumptions have to hold together for this story to work long term?

Result: Fair Value of $8.50 (OVERVALUED)

However, those cautious fair value models could unravel if high leverage and refinancing risk bite harder than expected, or if key hyperscaler and Windstream related revenues disappoint.

Another Way To Look At Value

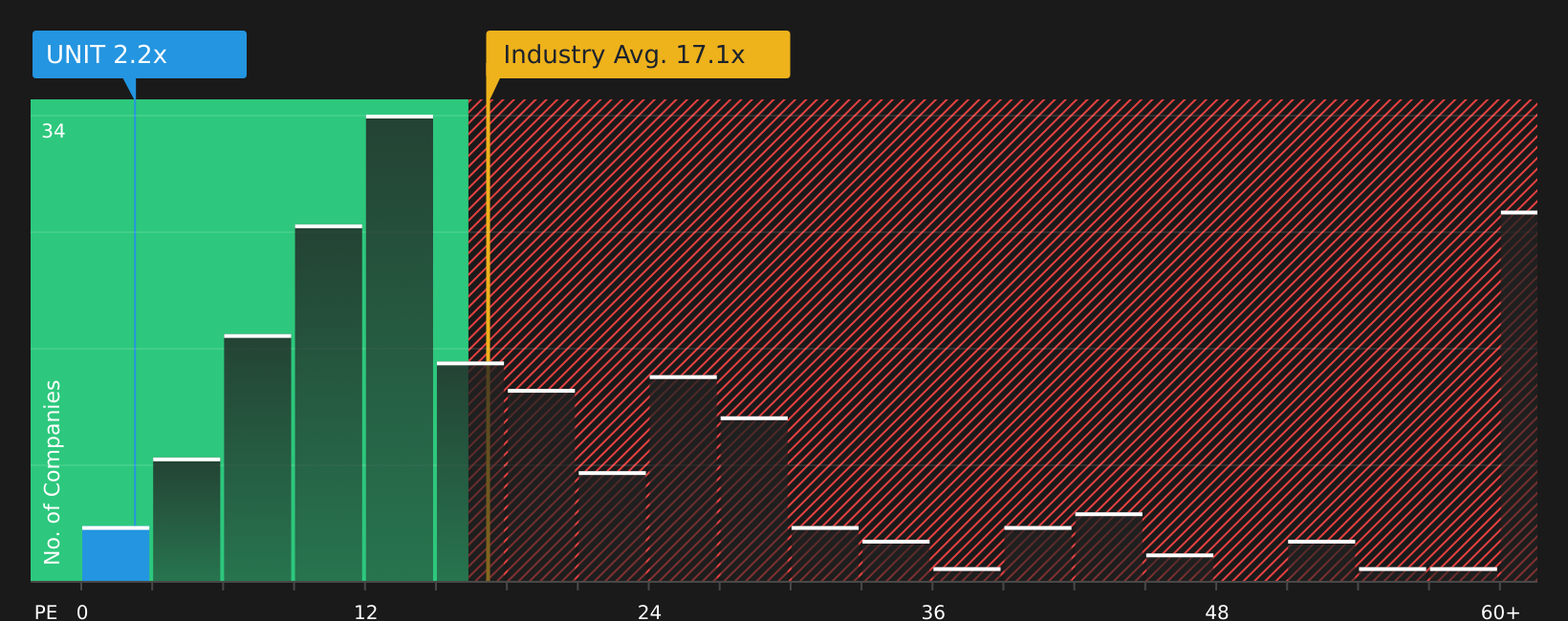

The analyst fair value of $8.50 points to Uniti as 38.5% overvalued. However, the current P/E of 2.3x tells a very different story when set against the US market at 19.4x, the global telecom group at 17.6x, a peer average of 8.7x, and a fair ratio of 7.3x. That sort of gap often reflects either real risk or a mispriced opportunity, so which side do you think this sits on?

Next Steps

The mixed signals on value, growth, and leverage make this a story that rewards your own digging rather than quick headlines. Take a moment to weigh the upside and downside for yourself with 3 key rewards and 4 important warning signs

Looking for more investment ideas?

If Uniti has you thinking about what else might fit your watchlist, do not stop here. Broaden your view with a few focused stock ideas.

- Target potential value opportunities by scanning for companies with quality fundamentals that the market may be overlooking using the 50 high quality undervalued stocks

- Strengthen the defensive side of your portfolio by reviewing companies screened for resilient financial profiles through the 69 resilient stocks with low risk scores

- Hunt for under followed names with solid business traits by checking the screener containing 25 high quality undiscovered gems

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.