A Look At Uniti Group (UNIT) Valuation After Q1 2026 Fiber Growth And Broadband Expansion

Uniti Group Inc. UNIT | 0.00 |

Uniti Group (UNIT) is back in focus after reporting first quarter 2026 results that paired significant fiber revenue growth with fresh broadband expansions across Georgia, Texas, Kentucky, North Carolina, Florida and Oklahoma.

Those broadband and wholesale fiber updates have arrived alongside strong share price momentum, with the stock posting a 34.6% 3 month share price return and a 113.5% 3 year total shareholder return, even though the 5 year total shareholder return is still down 14.1%.

If Uniti’s fiber build and AI driven demand have your attention, it could be a good moment to see what else is moving in related infrastructure, starting with 39 AI infrastructure stocks

After a sharp run in the share price alongside rapid fiber expansion and growing AI related demand, the key question is whether Uniti is still trading below its fundamentals or if the market is already pricing in future growth.

Most Popular Narrative: 32.4% Overvalued

With Uniti Group last closing at $11.25 against a most followed fair value estimate of $8.50, the current price sits well above that narrative line in the sand and puts the focus on what assumptions are doing the heavy lifting.

Declining legacy/TDM revenues are being offset by strong growth in fiber infrastructure (7% YoY) and consumer fiber ARPU (+11% YoY) and penetration (+120 bps YoY). This indicates that the mix shift to fiber will drive future consolidated revenue and net margin expansion as higher-value offerings comprise a growing share of total business.

Want to see what sits behind that fiber mix shift story? The most followed narrative leans on revenue compounding, margin reset and a future earnings multiple that is very different to where Uniti trades today. The full set of assumptions joins those pieces together into one valuation path.

Result: Fair Value of $8.50 (OVERVALUED)

However, there is still meaningful execution risk, with high leverage and rising fiber build costs that could pressure margins and challenge the narrative that the stock is currently overvalued.

Another Way To Look At Value

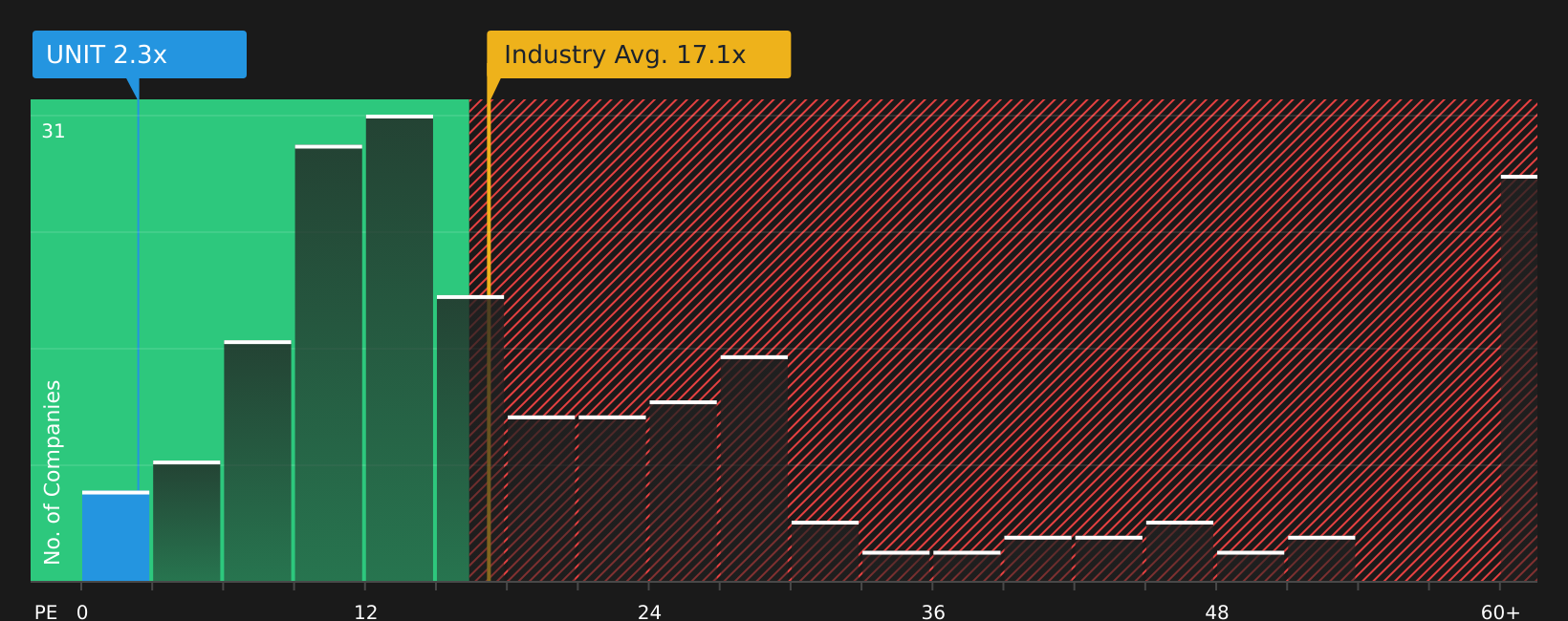

The analyst narrative leans on future earnings and P/E assumptions, but Uniti’s current P/E of 2.4x tells a different story when compared with the peer average of 8.7x, the global Telecom average of 17.1x, and a fair ratio of 7.5x that the market could move toward.

If the share price ever tracked closer to those higher P/E levels, the gap between today’s multiple and both peers and the fair ratio would represent either a cushion or a risk, depending on how the story around earnings quality and leverage evolves. Which side of that tradeoff do you think matters most right now?

Next Steps

With mixed sentiment running through this story, it makes sense to review the same numbers yourself and decide quickly where you stand, starting with 3 key rewards and 4 important warning signs.

Looking for more investment ideas?

If you stop here, you could miss stocks that better match your goals, so keep turning over stones with a broader set of ideas from the Simply Wall Street Screener.

- Target potential value opportunities by reviewing companies that pass the 47 high quality undervalued stocks that filters for quality and pricing support.

- Prioritise resilience by scanning the 67 resilient stocks with low risk scores to see which stocks score well on lower risk profiles.

- Hunt for under the radar potential using the screener containing 22 high quality undiscovered gems that highlights companies with strong fundamentals that may not be widely followed yet.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.