A Look At Varonis Systems (VRNS) Valuation After Recent Share Price Momentum

Varonis Systems VRNS | 0.00 |

Recent performance context for Varonis Systems (VRNS)

Varonis Systems (VRNS) has attracted renewed attention after a mixed stretch for shareholders, with a month gain of 18.1% set against a past 3 months return of 26.8% and a 1 year decline of 40.7%.

At a share price of US$25.05, Varonis Systems has recently seen short term momentum pick up, with a 1 month share price return of 18.1%, while the 1 year total shareholder return remains a 40.7% loss. This suggests sentiment is improving after a tough stretch.

If you are comparing Varonis Systems with other potential opportunities in technology, it could be a good moment to broaden your search and check out 71 profitable AI stocks that aren't just burning cash

With Varonis posting revenue of US$623.5m, a net loss of US$129.3m and trading at US$25.05 at a discount to some intrinsic and analyst estimates, is this a potential entry point, or is the market already pricing in future growth?

Most Popular Narrative: 25.1% Undervalued

Varonis Systems’ most followed narrative pegs fair value at about $33.43, compared with the last close of $25.05. This frames the stock as materially undervalued based on long term assumptions.

Investments in R&D and expansion of platform capabilities (for example, next generation database security, MDDR, AI driven integrations with Microsoft Copilot and OpenAI, cross platform coverage for AWS, Azure, Snowflake, Databricks, and others) are increasing customer wallet share and accelerating new logo acquisition, strongly supporting consistent top line and free cash flow growth.

Read the complete narrative. Read the complete narrative.

The narrative explores what could potentially turn today’s loss making profile into that higher fair value. It leans on compounded revenue expansion, margin shift, and a rich future earnings multiple tied to data security demand.

Analysts behind this narrative are effectively pricing in faster revenue growth than the broader US market, a move toward healthier profit margins, and a premium P/E level if and when earnings turn positive. Those elements are all incorporated into a discounted cash flow style framework that uses an 8.97% discount rate to bring projected cash flows back to today’s dollars and arrive at the $33.43 figure.

Result: Fair Value of $33.43 (UNDERVALUED)

However, the SaaS transition pressure on margins and the risk of ongoing share dilution could still derail those upbeat assumptions if execution or demand disappoints.

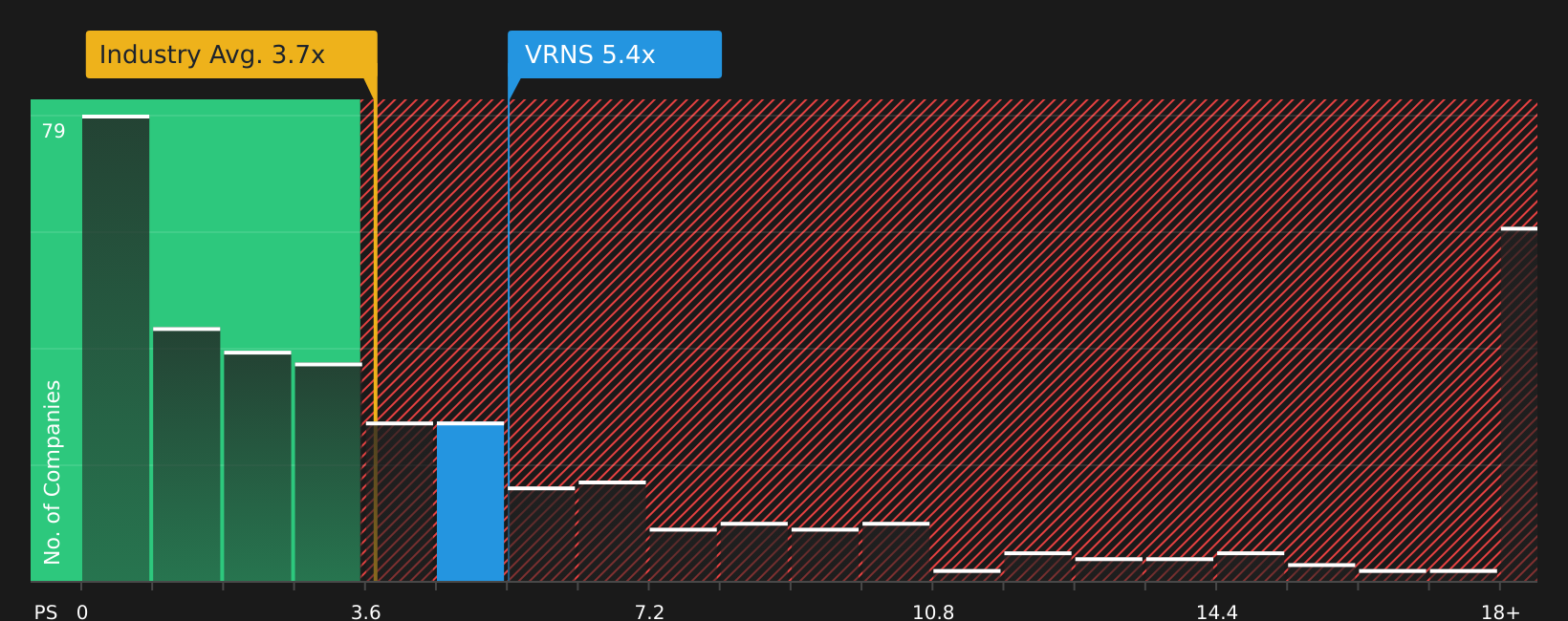

Another View: What Do Market Ratios Say?

Analysts and the SWS model see upside to fair value, yet the market is assigning Varonis a P/S ratio of 4.6x. This is higher than the US Software industry at 3.7x and peers at 2.9x. That gap suggests investors are already paying up, so the question is how much safety margin is really here?

Next Steps

Given the mix of optimism and caution in this article, it makes sense to move quickly, review the numbers yourself, and weigh both sides using the 2 key rewards and 1 important warning sign.

Looking for more investment ideas?

If VRNS is on your radar, do not stop here. The same toolkit can quickly surface other stocks that fit your style before opportunities move on.

- Target dependable income by scanning companies that appear built around resilient cash payouts using the 13 dividend fortresses.

- Spot potential upside by hunting for companies that combine quality fundamentals with prices that look appealing through the 53 high quality undervalued stocks.

- Prioritize resilience by focusing on businesses that pair solid finances with muted risk profiles via the 73 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.