A Look At Varonis Systems (VRNS) Valuation As Profitability And Efficiency Concerns Pressure Sentiment

Varonis Systems, Inc. VRNS | 0.00 |

Conference spotlight and investor concerns

Varonis Systems (VRNS) heads into its May 19 appearance at the J.P. Morgan Global Technology, Media and Communications Conference with investor sentiment already under pressure from efficiency and profitability concerns.

Recent commentary has focused on Varonis’s slower long term revenue growth compared with software peers, a customer acquisition cost payback period that appears unfavorable, and a GAAP operating margin that has been moving lower. Together, these factors weigh on confidence.

Varonis’s share price has climbed 12.64% over the past week and 24.68% over the past month, but the 1 year total shareholder return is down 34.43%. This highlights fading longer term momentum despite the upcoming conference catalyst.

If this kind of mixed performance has you reassessing your tech exposure, it could be worth scanning for other AI focused software opportunities using our curated list of 62 profitable AI stocks that aren't just burning cash

With the stock down 34.43% over the past year, but trading about 18% below the average analyst price target and roughly 25% below one intrinsic value estimate, it raises a key question for you: is this weakness a buying opportunity, or is the market already pricing in whatever growth comes next?

Most Popular Narrative: 8.3% Undervalued

With Varonis Systems last closing at $30.66 versus a narrative fair value of $33.43, the most followed storyline leans toward modest undervaluation and leans heavily on the SaaS and AI security opportunity.

Rapid proliferation of enterprise data and increased AI adoption are materially boosting demand for automated, comprehensive data protection, positioning Varonis to capture higher revenue growth and expand its total addressable market as organizations prioritize data security for both compliance and risk mitigation.

Varonis Systems Future Earnings and Revenue Growth Read the complete narrative.

Curious what sits behind that fair value gap? The narrative leans on brisk top line expansion, a step change in margins and a rich future earnings multiple. The exact mix of growth, profitability and discount rate assumptions might surprise you.

Result: Fair Value of $33.43 (UNDERVALUED)

However, you also need to weigh risks such as ongoing GAAP losses of US$130.4 million and potential pressure from larger platform competitors in data security.

Another View: Multiples Paint a Tougher Picture

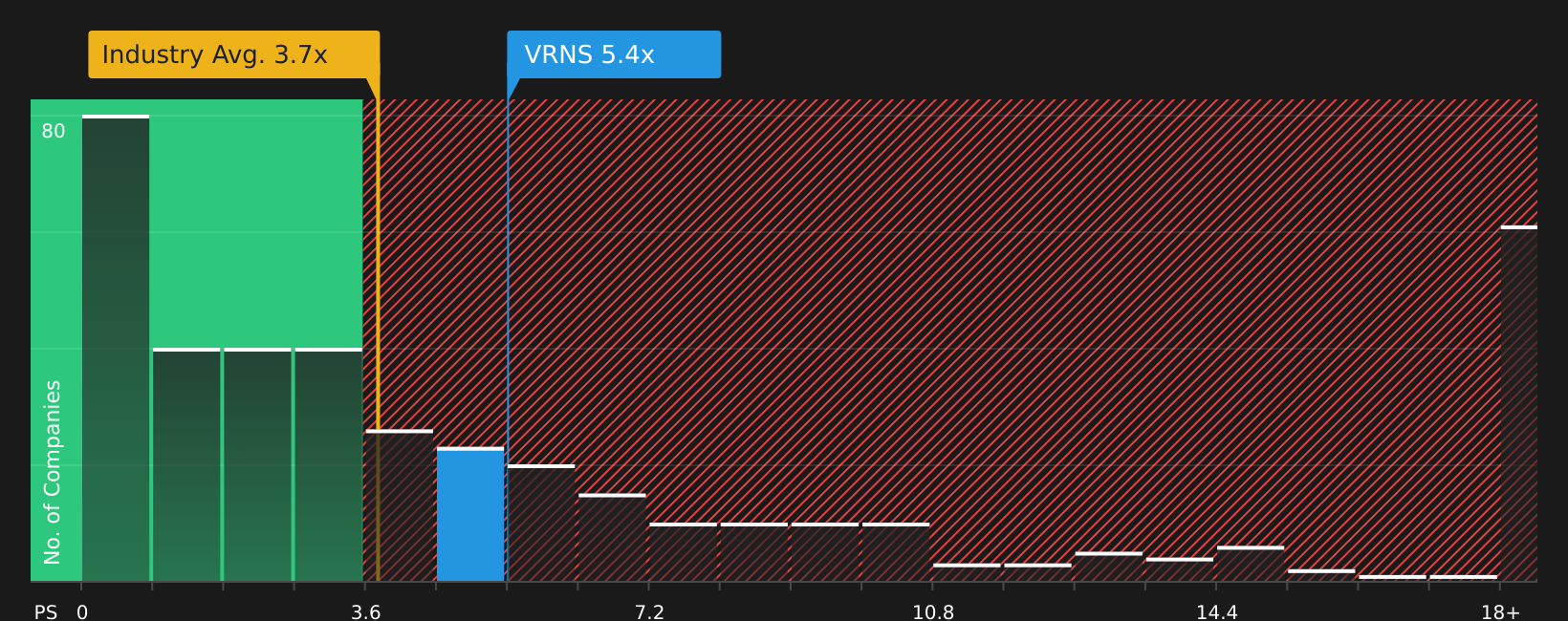

While the most popular fair value narrative points to modest undervaluation, the simple revenue multiple tells a tougher story. Varonis trades on a P/S of 5.3x, compared with 3.5x for the broader US software group, 4x for peers, and a fair ratio of 5x that the market could gravitate toward. That premium narrows the margin of safety, so how much confidence do you really have in the growth and margin assumptions baked into the higher tag?

Next Steps

Sitting on the fence after all of this? Move quickly to review the same numbers, cross check the trade offs, and weigh the 2 key rewards and 1 important warning sign.

Looking for more investment ideas?

If Varonis has sharpened your focus, do not stop here. Broaden your watchlist now so you are not playing catch up when the next opportunity surfaces.

- Target income first and scan for companies offering resilient cash returns with our hand picked set of 10 dividend fortresses.

- Hunt for quality at a lower price by reviewing our curated group of 53 high quality undervalued stocks.

- Protect your downside by concentrating on financially sound companies highlighted in the solid balance sheet and fundamentals stocks screener (46 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.