A Look At Ventas (VTR) Valuation As Shares Show Mixed Recent Performance

Ventas, Inc. VTR | 0.00 |

Ventas stock performance snapshot

Ventas (VTR) has drawn investor attention after a mixed recent performance, with the stock up 3.7% in the past day but down over the past week, month and past 3 months.

Over the past year, Ventas has delivered a 32.4% total return and is up 6.1% year to date. This gives investors a reference point against its longer term 3 year and 5 year total returns.

The recent 1 day share price return of 3.7% to US$82.02 comes after weaker 7 day, 30 day and 90 day share price returns, while the 1 year, 3 year and 5 year total shareholder returns indicate stronger momentum over longer horizons.

If this kind of move in healthcare real estate has your attention, it could be a good moment to see what else is setting up in the sector and scan 39 healthcare AI stocks

With Ventas trading at US$82.02 and referenced intrinsic and analyst estimates implying potential upside, the key question is whether the current price still reflects a discount or if the market is already pricing in future growth.

Most Popular Narrative: 15.1% Undervalued

With Ventas last closing at $82.02 against a narrative fair value of $96.65, the current setup reflects a valuation gap that analysts have tried to explain using detailed growth and profitability assumptions tied to healthcare real estate demand.

Ventas is positioned to benefit from a rapidly growing aging population driving sustained demand for senior housing and healthcare facilities, combined with historically low new construction, supporting multi-year occupancy gains and net operating income (NOI) growth as occupancy rates rise from the low 80% toward the 90%+ level. This is likely to drive substantial operating leverage and margin expansion.

Want to see what kind of revenue ramp and margin profile has to line up for that valuation gap to make sense? The narrative leans on earnings compounding, higher profitability and a premium future earnings multiple that sits above the sector. It focuses on how those moving parts connect and what would need to occur each year to reach that fair value.

Result: Fair Value of $96.65 (UNDERVALUED)

However, this optimistic setup can quickly be challenged if senior housing operators underperform, or if higher interest costs squeeze returns from Ventas’ planned acquisition pipeline.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Another angle on valuation

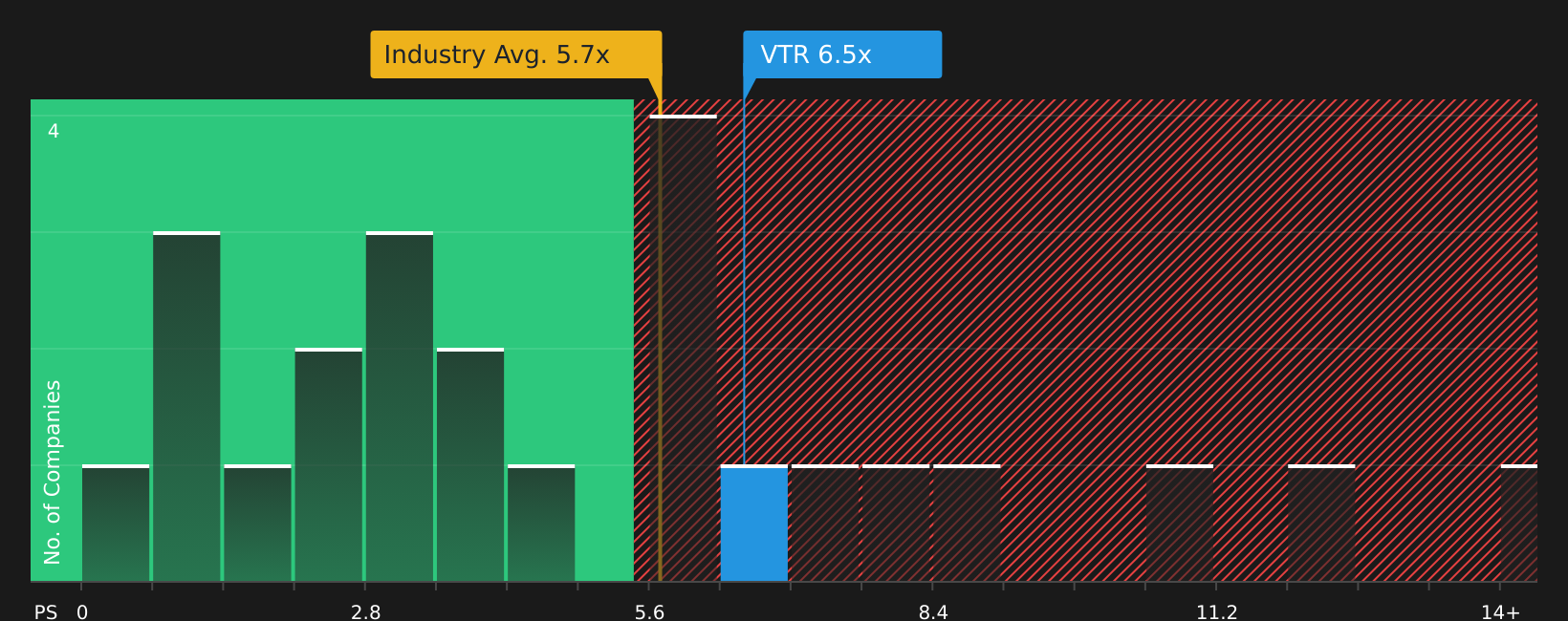

Those cash flow based narratives paint Ventas as 15.1% undervalued, yet its current P/S of 6.5x is higher than both the North American Health Care REITs industry at 5.7x and a fair ratio of 5.5x. That premium suggests less margin for error, so which signal do you put more weight on?

Next Steps

Mixed signals on value and sentiment so far? Take a closer look at the numbers, weigh both the concerns and potential upside, and review the 3 key rewards and 3 important warning signs.

Looking for more investment ideas?

If Ventas has sharpened your focus, do not stop here. Use these curated stock ideas to broaden your watchlist and avoid missing opportunities building beneath the surface.

- Target resilient cash generators by scanning 49 high quality undervalued stocks, which combine quality fundamentals with prices that sit below their estimated worth.

- Strengthen your income stream by reviewing 9 dividend fortresses, featuring higher yielding companies with a focus on consistency.

- Prioritize stability and downside protection by filtering for 61 resilient stocks with low risk scores, aiming to keep volatility in check while still offering growth potential.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.