A Look At Veris Residential (VRE) Valuation After Erez Calls For Review To Unlock Net Asset Value

Veris Residential, Inc. VRE | 18.95 | +0.26% |

Erez Asset Management’s letter urging Veris Residential (VRE) to launch a formal review of alternatives has pushed the REIT into focus, with the shareholder citing a sizeable gap to stated net asset value.

The shareholder letter has arrived at a time when momentum in Veris Residential’s share price has been firming. The 7 day share price return stands at 9.55%, the 30 day share price return at 10.79% and the year to date share price return at 12.13%. The 5 year total shareholder return of 24.68% points to a more measured longer term outcome as investors weigh the REIT’s discount to stated net asset value against ongoing governance and capital allocation questions.

If this type of catalyst driven move has your attention, it could be a good moment to broaden your search and look through 22 top founder-led companies as potential next ideas.

With Veris Residential trading at a discount to both its stated net asset value and analyst price target, yet already showing solid recent returns, investors may need to consider whether there is still a buying opportunity or if the market is already pricing in future growth.

Most Popular Narrative: 10.9% Overvalued

The most followed narrative puts Veris Residential’s fair value at $15, below the last close of $16.64, setting up a clear valuation gap for investors to weigh.

While Veris benefits from institutional investor demand and a renewed focus on sustainability, the persistent affordability crisis and political momentum for tenant protections or rent controls in urban markets may constrain Veris's ability to raise rents in line with recent history, directly limiting rental revenue growth and margin expansion.

If you want to see what is built into that $15 fair value, the key is how future revenue, margins and earnings power are modeled against those constraints.

Result: Fair Value of $15 (OVERVALUED)

However, concentrated exposure to Jersey City and higher leverage could quickly challenge this bearish view if local conditions or financing terms shift more sharply than expected.

Another View: Cash Flows Point To A Different Story

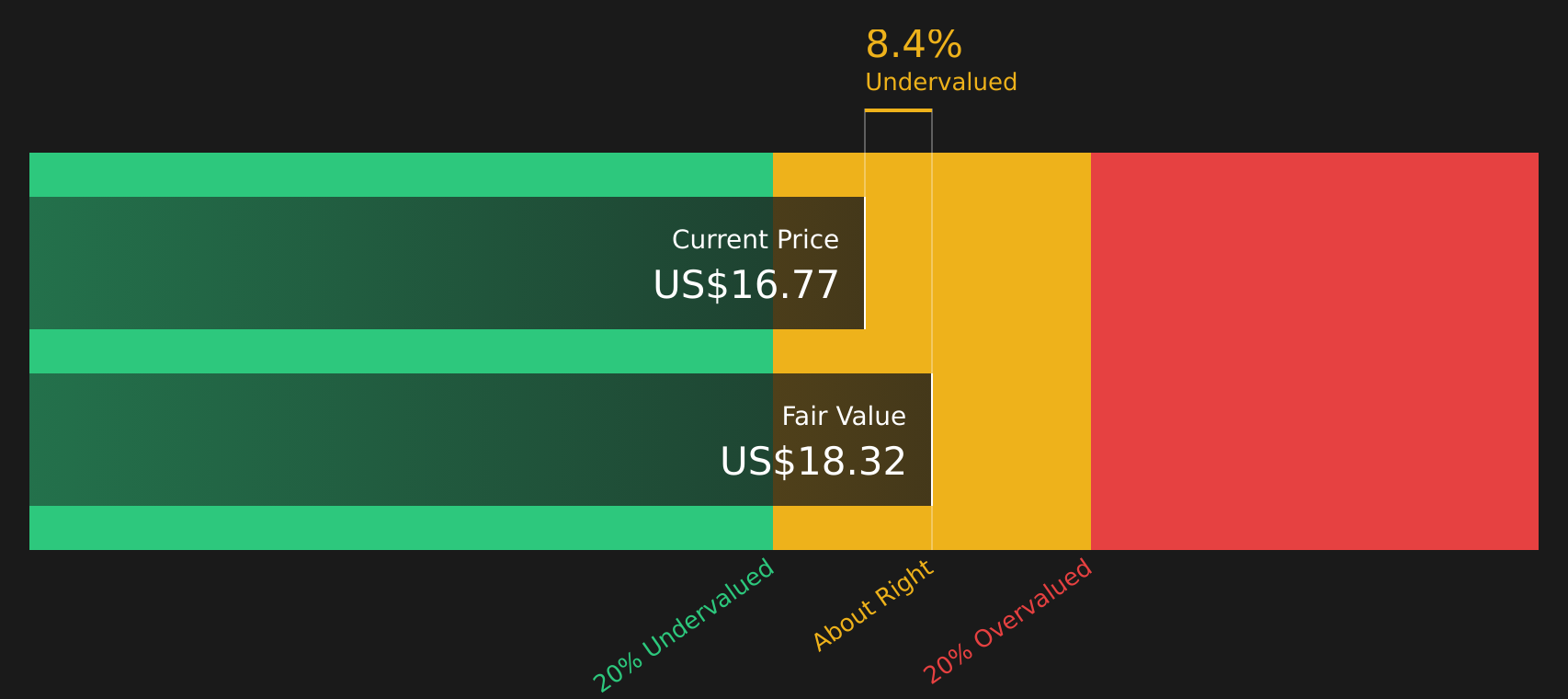

The bearish narrative leans heavily on earnings and P/E, but our DCF model focuses on future cash flows instead and comes out more optimistic. On that basis, Veris Residential at $16.64 sits about 7.1% below an estimated fair value of $17.92, which frames today’s price as a potential discount rather than a premium. Which version of “fair” do you trust more: earnings multiples or cash flow math?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Veris Residential for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 53 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Veris Residential Narrative

If this view does not quite fit how you see Veris Residential, or you prefer to dig into the numbers yourself, you can build your own narrative in just a few minutes with Do it your way

A great starting point for your Veris Residential research is our analysis highlighting 2 key rewards and 4 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Veris Residential has sparked your interest, do not stop here. Broaden your watchlist with focused ideas built from real data and clear filters.

- Target stability and potential value with 86 resilient stocks with low risk scores, which keep overall risk scores in check while still offering room for returns.

- Hunt for quality at a reasonable price by checking out 53 high quality undervalued stocks, which combine solid fundamentals with pricing that may appeal to value focused investors.

- Build a watchlist of dependable income ideas by scanning 14 dividend fortresses, where yields of 5%+ are paired with a focus on resilience.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.