A Look At Verizon (VZ) Valuation After Subscriber Surge Buyback And Frontier Acquisition

Verizon Communications Inc. VZ | 49.40 | +0.02% |

Verizon Communications (VZ) is back in focus after reporting its strongest subscriber gains since 2019, outlining ambitious 2026 postpaid targets, closing the Frontier acquisition, and launching a US$25b buyback alongside its ongoing dividend commitment.

The stronger fourth quarter, Frontier deal, dividend update and US$25b buyback have quickly fed into the share price, with a 7 day share price return of 17.62% and year to date share price return of 14.14%. At a US$46.25 share price, that short term momentum sits on top of a 1 year total shareholder return of 24.13% and 3 year total shareholder return of 39.80%, suggesting sentiment has been improving over both recent months and the longer term.

If Verizon’s move has caught your eye, this can be a good moment to see what else is gaining attention in communications and connectivity. This includes fast growing stocks with high insider ownership.

With Verizon trading at US$46.25, a modest discount to the average analyst price target and a large gap to one intrinsic value estimate, the real question is whether this surge leaves upside on the table or whether markets are already pricing in future growth.

Most Popular Narrative: 1.8% Undervalued

Compared with Verizon Communications' last close of $46.25, the most followed narrative pegs fair value at about $47.11, leaving a small valuation gap to unpack.

Ongoing cost optimization driven by successful voluntary separation programs, copper network decommissioning, AI powered process efficiencies, and operational streamlining continues to improve operating leverage and expand EBITDA and free cash flow, underpinning sustainable future earnings growth.

Want to see what sits behind that fair value call? Revenue, earnings, and margins are all wired into one tight cash flow story. The key is how long those assumptions hold and what future profit multiple the narrative leans on. Curious which levers matter most in that model and how sensitive the outcome is to each one?

Result: Fair Value of $47.11 (UNDERVALUED)

However, that story can fray if heavy 5G and fiber investment fails to pay off, or if competition and high debt costs start to squeeze margins and cash generation.

Another Take: Multiples Point To A Richer Price

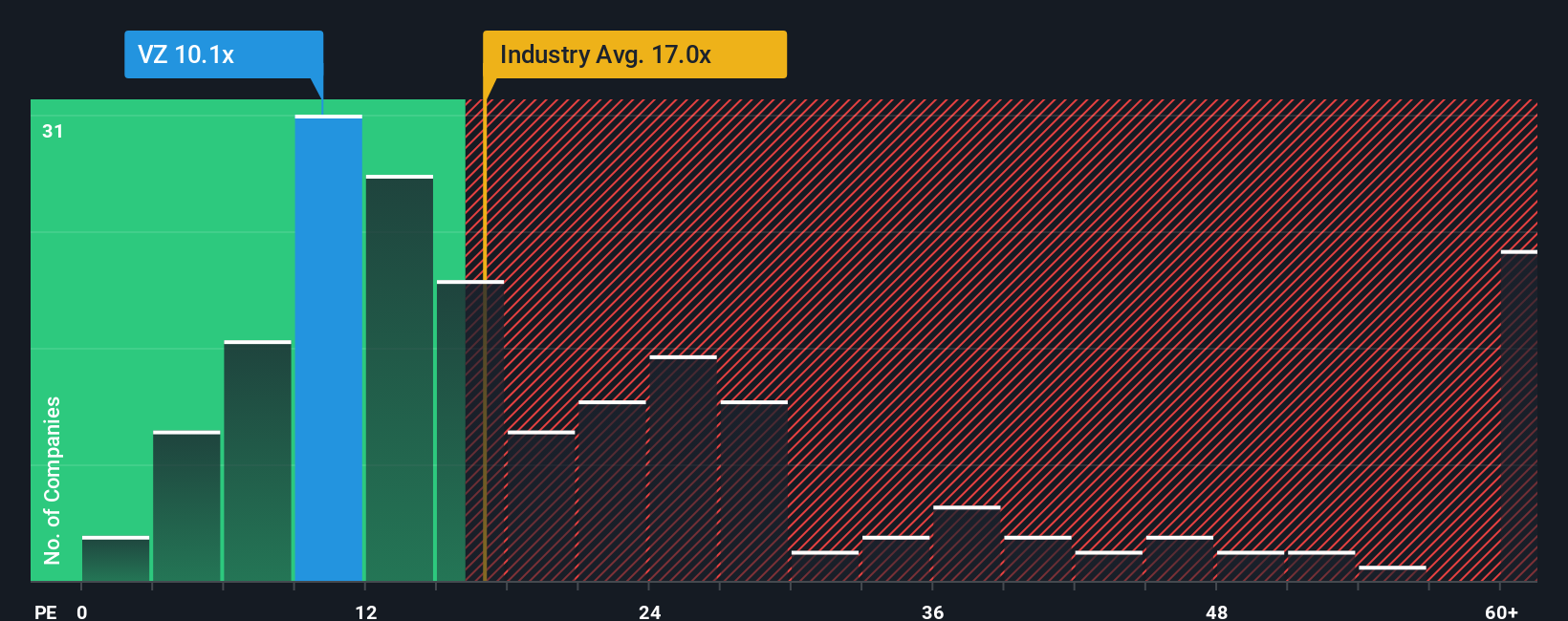

That 1.8% undervaluation call sits next to a very different signal. On earnings, Verizon trades at a P/E of 11.4x, which is more than double its direct peer average of 5.4x and below its fair ratio of 14.3x, as well as the 16.4x Global Telecom average.

In plain terms, the market already prices Verizon well above close peers, yet still below where the fair ratio suggests the P/E could drift over time. This raises a question: is that a cushion for further upside, or a sign that expectations could be tight if growth or margins disappoint?

Build Your Own Verizon Communications Narrative

If you see the data differently or prefer to test your own assumptions, you can build a custom Verizon view in just a few minutes with Do it your way.

A great starting point for your Verizon Communications research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Ready for more investment ideas?

If Verizon is on your radar, do not stop there. Use the Simply Wall Street Screener to quickly uncover other opportunities that might fit your style and goals.

- Target reliable cash flows by checking out these 13 dividend stocks with yields > 3% that can add income potential to a long term portfolio.

- Spot growth themes early by scanning these 26 AI penny stocks that are tied to advances in artificial intelligence and data driven business models.

- Hunt for value by reviewing these 871 undervalued stocks based on cash flows where current prices sit below our cash flow based assessments.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.