A Look At Victoria's Secret (VSXY) Valuation After Earnings Beat And Upgraded Outlook

Victoria's Secret & Company VSXY | 0.00 |

Victoria's Secret (VSXY) is back in focus after first quarter results beat sales and earnings expectations, lifted by broad-based growth, strong customer acquisition, and a higher full-year outlook that helped reset investor sentiment.

At a share price of $78.96, Victoria's Secret has seen strong momentum, with a 57.04% 30 day share price return and a very large 1 year total shareholder return that reflects how rapidly sentiment has shifted after the earnings beat, guidance lift, buyback activity, and proxy fight headlines.

If the turnaround story has you rethinking where growth could come from next, it can be useful to scan beyond retail and look at companies building future infrastructure, including 33 power grid technology and infrastructure stocks

After a 47% one-day surge, a 57.04% 30-day jump, a very large 1-year total return, and the stock now trading only about 4% below the average analyst target, is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 20.4% Overvalued

Analysts in the most followed narrative see fair value for Victoria's Secret at $65.56, which sits below the latest close of $78.96 and frames the current rally against a richer valuation backdrop.

The ongoing transformation of Victoria's Secret toward inclusivity, body positivity, and enhanced storytelling continues to resonate with younger customers and drive new customer acquisition, especially among the 18-44 demographic, supporting sustained revenue and market share growth.

Momentum in omnichannel growth, including robust international expansion and digital channel strength, positions the brand to benefit from rising global middle-class demand, leading to higher topline revenue and improved operating leverage.

Want to see what kind of revenue path, margin reset, and future earnings multiple have to line up for that $65.56 fair value to work? The most followed narrative leans on stronger profitability and a lower future P/E all at once, and the exact mix of those ingredients may surprise you.

Result: Fair Value of $65.56 (OVERVALUED)

However, if tariffs bite harder than modeled or mall traffic weakens further, margin pressure and slower sales could easily challenge the current fair value narrative.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Another Lens On Value

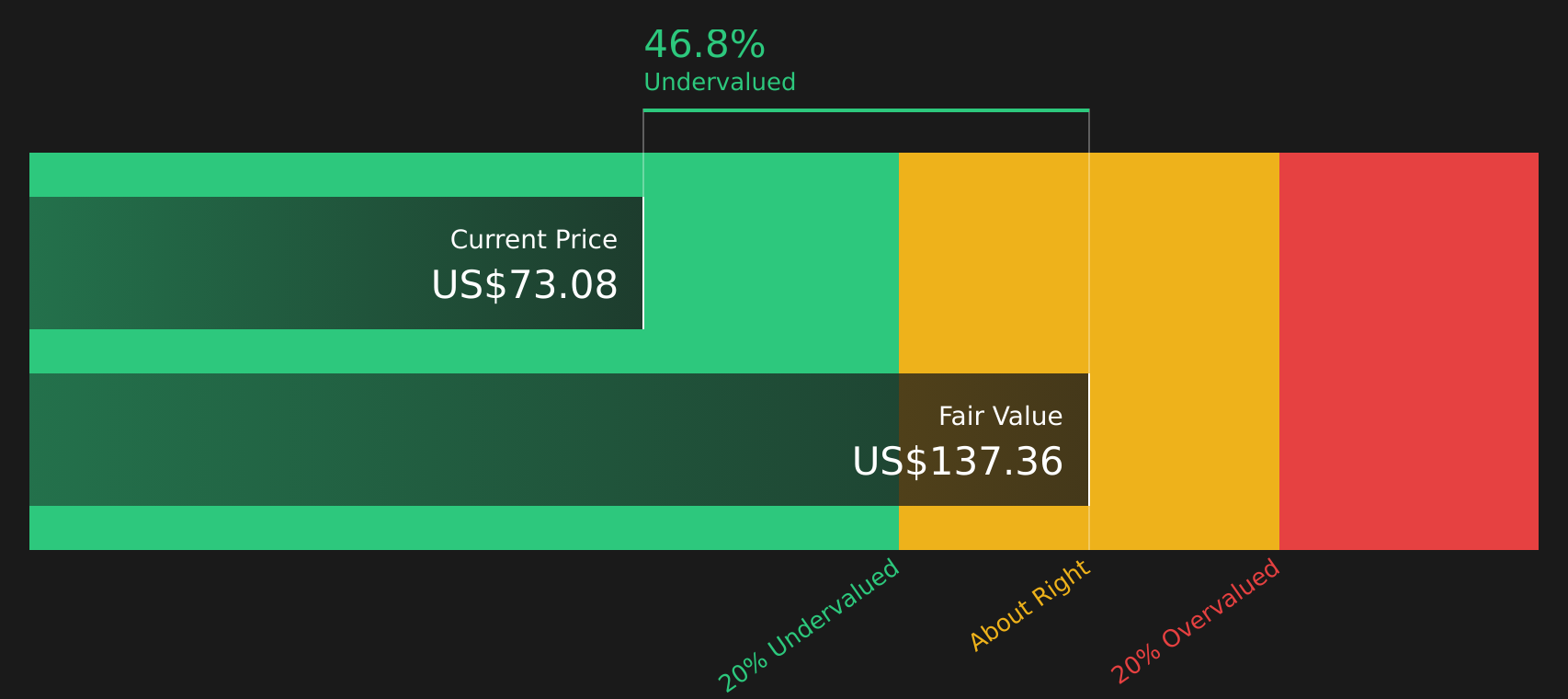

While one widely followed view suggests Victoria's Secret is 20.4% overvalued at $78.96 based on analyst targets, Simply Wall St's DCF model suggests the opposite. The model estimates a future cash flow value of $134.45, which would imply the stock trades at a sizeable discount. Which perspective do you think better reflects how cash flows might develop?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Victoria's Secret for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 47 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Mixed signals on value can be useful, especially when momentum and narratives are moving fast, so checking the underlying data now helps you build your own stance using the 3 key rewards and 3 important warning signs.

Looking for more investment ideas?

If you stop with just one stock, you could miss other opportunities that better fit your goals. Widen your search and pressure test your next move using targeted screeners.

- Spot potential mispricings by scanning 47 high quality undervalued stocks that combine quality fundamentals with more modest expectations.

- Lock in potential income streams by reviewing 10 dividend fortresses that focus on higher yields with staying power.

- Sleep a little easier by checking 63 resilient stocks with low risk scores built around companies with more resilient risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.