A Look At Vishay Intertechnology (VSH) Valuation After New Power Electronics Module Launch

Vishay Intertechnology, Inc. VSH | 18.58 | +0.92% |

Vishay Intertechnology (VSH) has just rolled out four new 100 V Gen 2 Trench MOS Barrier Schottky rectifier modules, a product launch that puts fresh attention on its role in industrial and automotive power electronics.

The new rectifier launch lands after a strong 30-day share price return of 22.92% and a 20.67% year to date share price gain, even though the 3 year total shareholder return is negative at 12.94%. This suggests recent momentum has picked up compared with longer term results.

If this kind of product driven move interests you, it could be a good moment to see what else is setting up for growth across high growth tech and AI stocks.

The stock is now trading at $18.45, above the US$15 analyst price target and with a weak value score of 3. The key question is whether this recent momentum leaves any mispricing or if the market is already accounting for potential future growth.

Most Popular Narrative: 23% Overvalued

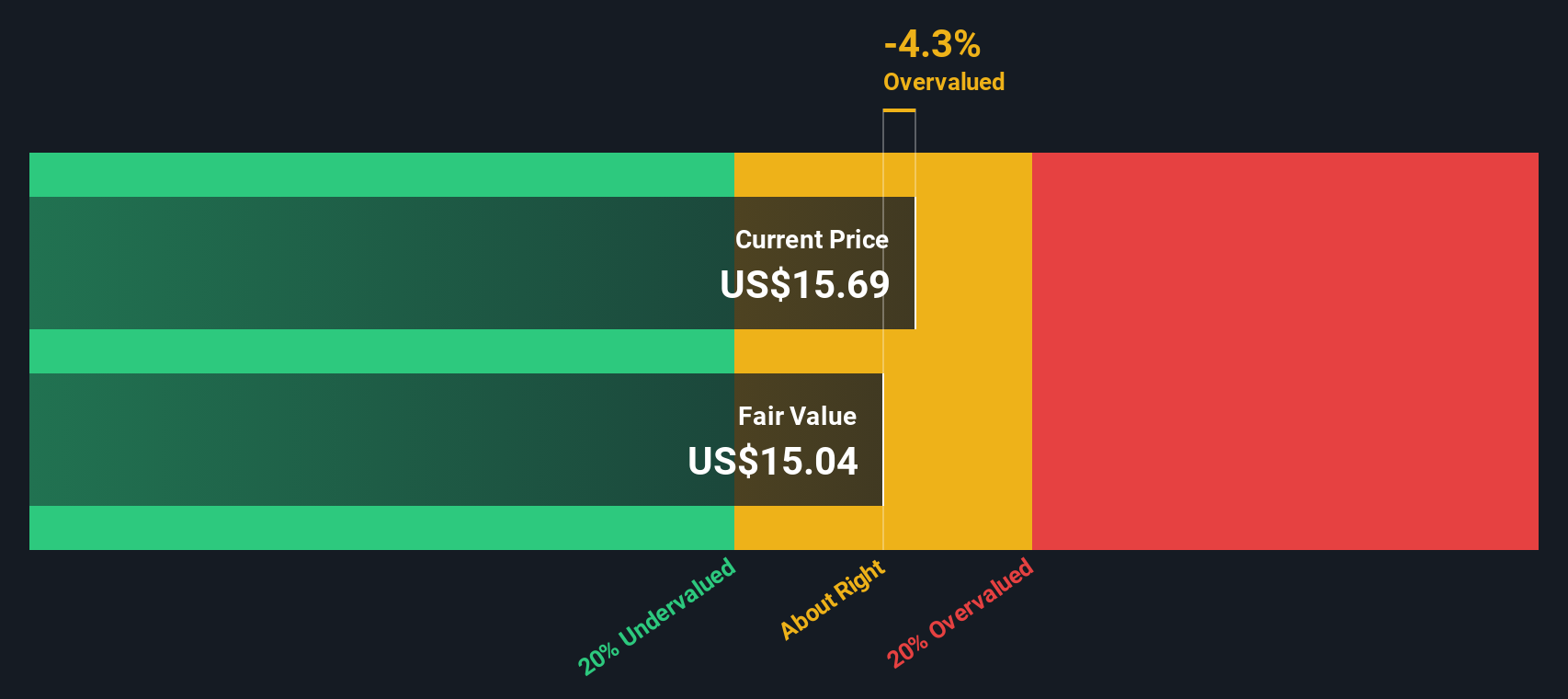

With Vishay Intertechnology last closing at $18.45 against a narrative fair value of $15.00, the most followed storyline sees the shares ahead of that fair value, built on detailed assumptions about future earnings and margins.

Ongoing innovation and commercialization in advanced technologies (e.g., silicon carbide MOSFETs and diodes) and deeper cross-selling initiatives are leading to an expanding bill-of-materials footprint with key customers in automotive, industrial, and AI, likely boosting average selling prices, product mix, and ultimately net margins.

Curious what kind of revenue path and margin reset would need to support that $15 fair value while the stock trades above it today? The core narrative leans on a sizeable earnings swing, richer profitability, and a lower future P/E than many sector names. Want to see exactly how those moving parts are stitched together and how a single discount rate ties it all back to today’s price?

Result: Fair Value of $15 (OVERVALUED)

However, heavy capacity spending with negative free cash flow, together with persistently low operating margins, could quickly challenge those rich earnings and P/E assumptions if demand disappoints.

Another angle on value

Our SWS DCF model presents a far tougher picture for Vishay Intertechnology, with an estimated future cash flow value of $6.88 per share compared with the current $18.45 price, which screens as overvalued. When one model indicates $15 and another suggests closer to $7, which set of assumptions do you find more appropriate?

Build Your Own Vishay Intertechnology Narrative

If you see the inputs differently or prefer to work from your own assumptions, you can rebuild the entire analysis in a few minutes, starting with Do it your way.

A great starting point for your Vishay Intertechnology research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Ready for more investment ideas?

If Vishay has caught your attention, do not stop here. Broaden your watchlist with a few focused stock groups that line up with your own priorities and risk comfort.

- Target income first and scan these 14 dividend stocks with yields > 3% that may suit investors who want cash returns to play a bigger role in their portfolio.

- Ride long term technology themes by checking out these 23 AI penny stocks that are tied to the growth of artificial intelligence and related infrastructure.

- Get ahead of niche trends by reviewing these 23 quantum computing stocks that could benefit if quantum computing applications keep moving closer to real world use.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.