A Look At Vistance Networks (VISN) Valuation After RUCKUS Pro AV Launch And New Partnerships

Gyroscope Therapeutics Holdings plc VISN | 18.73 | +2.07% |

RUCKUS Networks’ new Pro AV focused ICX switch lineup and updated management platforms, plus fresh ties with Crestron and the SDVoE Alliance, put Vistance Networks (VISN) firmly in the Ethernet based professional AV spotlight.

VISN’s latest product and partnership news comes on the back of a 14.4% 90 day share price return and a very large 1 year total shareholder return, suggesting momentum has been strong rather than fading recently.

If this Pro AV news has you looking across the wider networking and infrastructure space, you might also want to scan our screener of 34 AI infrastructure stocks as another source of ideas.

With VISN up 14.4% over 90 days and delivering a very large 1 year total return, yet still trading at a 26% discount to the US$24.25 analyst target, are you seeing a genuine opening here, or is the market already pricing in future growth?

Most Popular Narrative: 20.8% Undervalued

With Vistance Networks closing at $19.20 against a narrative fair value of $24.25, the gap between market pricing and that story driven estimate is hard to ignore.

The completed sale of the CCS business is set to eliminate company debt and preferred equity, reduce interest expense, and free up significant excess cash for shareholder returns, directly improving net earnings and the company's capital structure resilience.

Read the complete narrative. Read the complete narrative.

Want to see what sits behind that higher fair value? The narrative focuses on projected revenue expansion, firmer margins, and a rich future earnings multiple. Curious which assumptions really move the model?

Result: Fair Value of $24.25 (UNDERVALUED)

However, you still need to weigh up that VISN’s remaining ANS and RUCKUS operations are more cyclical, with customer concentration and tougher competition potentially putting pressure on revenue and margins.

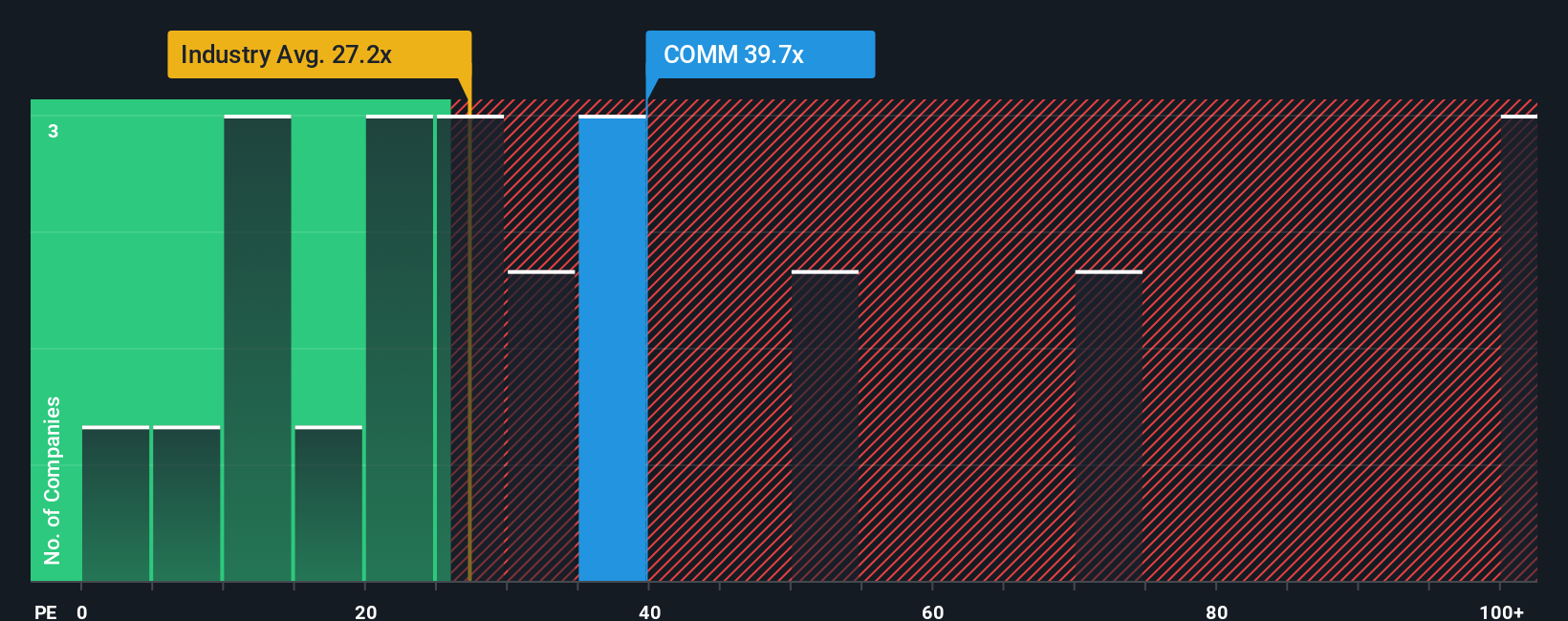

Another Angle, Market Ratio Says Overvalued

That 20.8% “undervalued” narrative sits awkwardly next to how VISN trades on earnings today. The current P/E is 14.5x versus a fair ratio of 3.6x, and well below peers at 71.7x and the wider US Communications group at 30.9x. Is this a sensible discount, or a warning that the story is running ahead of the numbers?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Vistance Networks for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 55 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Vistance Networks Narrative

If you are not fully on board with this take, or prefer to lean on your own research and data, you can build a custom view in just a few minutes, Do it your way.

A great starting point for your Vistance Networks research is our analysis highlighting 3 key rewards and 4 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If VISN has sharpened your focus, do not stop here. Put the same energy into finding other opportunities that fit your own risk, income, and return goals.

- Spot potential bargains early by scanning our list of screener containing 23 high quality undiscovered gems that combine solid fundamentals with low market attention.

- Target resilient balance sheets by filtering for companies in the solid balance sheet and fundamentals stocks screener (44 results) that can better handle tougher conditions.

- Prioritise stability by reviewing 86 resilient stocks with low risk scores that score well on financial strength and risk metrics before the crowd catches on.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.