A Look At Vulcan Materials (VMC) Valuation As Analyst Optimism Tops Insider Selling Concerns

Vulcan Materials Company VMC | 279.88 | -0.09% |

Vulcan Materials (VMC) has been drawing fresh attention as analysts highlight its role in US infrastructure and investors weigh this sentiment against recent insider selling, which includes share sales by the company’s president.

At a share price of $301.71, Vulcan Materials has had a relatively steady run, with a 30 day share price return of 3.32% and a 1 year total shareholder return of 12.92%. The 3 year total shareholder return of 74.76% points to stronger longer term momentum that investors are weighing against recent insider selling and mixed analyst commentary.

If you are assessing how infrastructure linked names fit into your portfolio, this can be a useful moment to broaden your search with fast growing stocks with high insider ownership.

With Vulcan Materials trading at $301.71 against an average analyst target of $324.59 and some insiders selling into strength, you have to ask: Is there still value on the table, or is future growth already priced in?

Most Popular Narrative: 6.2% Undervalued

The most followed narrative places Vulcan Materials' fair value at US$321.50, which sits modestly above the recent US$301.71 close and frames the stock as slightly discounted.

Accelerating infrastructure spending, driven by the ongoing rollout of IIJA funding, major state initiatives in core Southern and Sunbelt markets, and increasing local spending, is visibly expanding Vulcan's backlogs and contract awards; with over 60% of IIJA funds still to be spent and awards up over 20% in Vulcan-served regions, this points to multi-year growth in volumes and more predictable, compounding revenue.

Curious how projected revenue, margin lift and a premium future P/E are all stitched together to back that fair value? The full narrative walks through the earnings path, the assumed profitability shift and the valuation multiple that ties it all together.

Result: Fair Value of $321.50 (UNDERVALUED)

However, you still have to keep an eye on delays or deferrals in key construction projects, as well as any shift in government infrastructure funding that could stall those earnings assumptions.

Another View: Multiples Flag A Richer Price

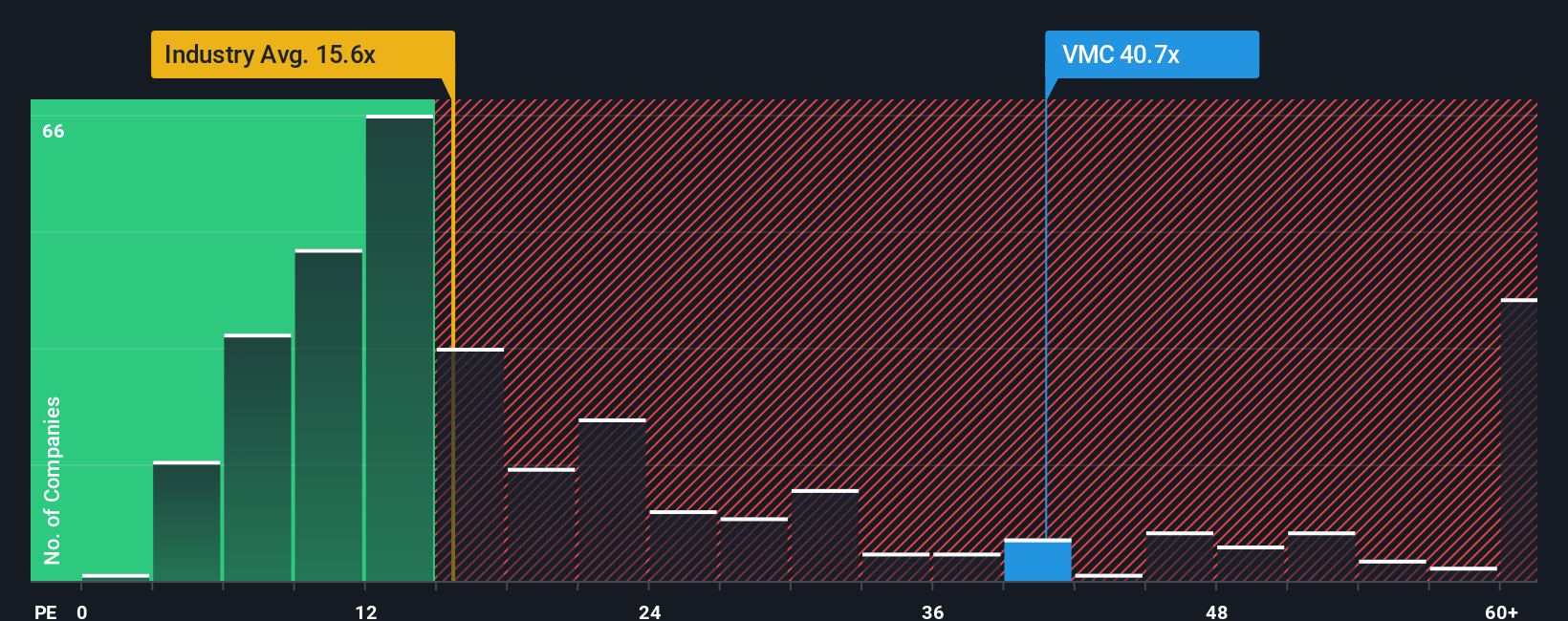

Those fair value narratives suggest upside, but the market is already paying a steep P/E of 35.4x for Vulcan Materials compared with a fair ratio of 23.5x, a peer average of 26x and a global Basic Materials average of 15.2x. That premium can signal conviction, or simply leave less margin for error if expectations cool.

Build Your Own Vulcan Materials Narrative

If you look at the numbers and come to a different conclusion, or simply prefer to test your own assumptions, you can build a custom Vulcan view in just a few minutes with Do it your way.

A great starting point for your Vulcan Materials research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Ready for more investment ideas?

If Vulcan Materials has sharpened your interest, do not stop here. Broaden your watchlist with fresh ideas sourced from focused screeners built to surface specific opportunities.

- Target potential value opportunities by checking stocks flagged as attractively priced on cash flows through these 869 undervalued stocks based on cash flows.

- Spot income ideas by reviewing companies with stronger yields using these 12 dividend stocks with yields > 3%.

- Explore long term technology themes by scanning for names linked to digital assets and blockchain via these 80 cryptocurrency and blockchain stocks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.