A Look At Vulcan Materials (VMC) Valuation As Infrastructure Optimism Supports Pricing Power And Demand

Vulcan Materials Company VMC | 279.88 | -0.09% |

Vulcan Materials (VMC) shares are reacting to renewed optimism around federal and state infrastructure spending, tight aggregate supply, and supportive analyst commentary that underscores the company’s pricing power and steady, contract backed demand.

That optimism has been reflected in a 4.5% 30 day share price return and a 13.7% 1 year total shareholder return, while the 3 year and 5 year total shareholder returns of 72.4% and 106.6% point to momentum that has built over time rather than appearing suddenly.

If infrastructure spending has your attention, it can be useful to see how other materials linked names have been trading, especially across aerospace and defense stocks as large capital projects often span multiple sectors.

So with Vulcan already up strongly over 1, 3 and 5 years and trading around $305.92 against an average analyst target near $327.65, is there still a reasonable entry point here, or is the market already pricing in future growth?

Most Popular Narrative: 4.8% Undervalued

With Vulcan Materials last closing at $305.92 against a most followed fair value estimate of $321.50, the current narrative leans slightly toward undervaluation and hangs on sustained infrastructure demand and margin strength.

Expanding infrastructure investment and a dominant presence in high-growth metros are associated with sustained revenue growth and strong pricing power for Vulcan Materials. Operational efficiencies, successful acquisitions, and rising demand from infrastructure and renewable projects are described as supporting margin expansion and long-term profitability.

Curious what sits behind that confidence in pricing and margins? The narrative focuses on steady revenue compounding, thicker profit margins, and a future earnings multiple that is expected to require meaningful execution. The full write up outlines how those elements connect to that fair value estimate.

Result: Fair Value of $321.50 (UNDERVALUED)

However, you still need to factor in risks around public funding dependence and weather-exposed Southeast markets, which could pressure volumes and margins if conditions turn.

Another Angle: Richer Multiples Temper The Undervaluation Story

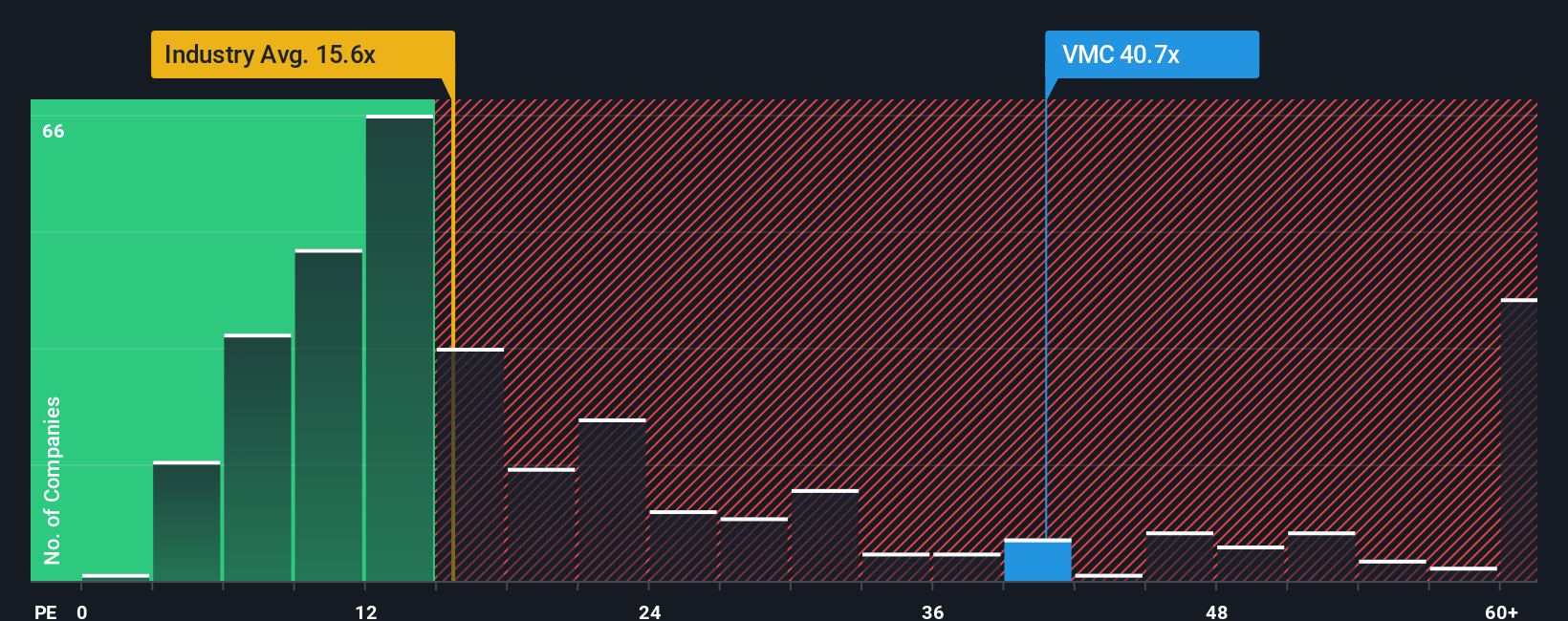

That 4.8% undervaluation signal sits awkwardly next to Vulcan Materials trading on a P/E of 35.9x, versus 24.9x for peers and a fair ratio of 24.5x. That gap points to meaningful valuation risk if sentiment cools, so how comfortable are you paying a premium for this earnings profile?

Build Your Own Vulcan Materials Narrative

If you are not fully on board with this view or prefer to rely on your own analysis, you can weigh the same data, develop your own perspective in a few minutes and Do it your way.

A great starting point for your Vulcan Materials research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Ready for more investment ideas?

If Vulcan has sharpened your focus on infrastructure and pricing power, do not stop there. Broaden your watchlist and pressure test your thinking across other corners of the market.

- Spot potential mispricings quickly by scanning these 876 undervalued stocks based on cash flows that line up with your return and risk expectations.

- Tap into the next wave of automation and productivity by reviewing these 24 AI penny stocks shaping the way software and hardware work together.

- Put income at the center of your plan with these 13 dividend stocks with yields > 3% that already offer yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.