A Look At W. R. Berkley (WRB) Valuation As Shares Show Recent Weakness

W. R. Berkley Corporation WRB | 0.00 |

Stock performance and recent context

W. R. Berkley (WRB) has seen mixed share performance recently, with the stock near US$66 and returns showing modest movement over the past week and month, but a more pronounced decline over the past 3 months and year.

Recent trading has been soft, with a 90 day share price return of about a 7% decline and a 1 year total shareholder return of about a 7% decline, even though the 3 and 5 year total shareholder returns remain strongly positive.

If you are comparing W. R. Berkley with other opportunities in financials and beyond, it can help to widen the lens and review 19 top founder-led companies

With WRB trading close to analyst targets and sitting on a sizeable modelled intrinsic discount, recent share weakness raises a core question for you: is this an undervalued insurer, or is the market already pricing in future growth?Most Popular Narrative: 3.2% Undervalued

With W. R. Berkley last closing at $66.12 against a narrative fair value of $68.33, the current setup hinges on how resilient earnings and margins can be in a softer pricing backdrop.

The expanding complexity of global business and assets is driving strong demand for specialty insurance solutions, with record net written premiums and broad-based growth across all lines positioning W. R. Berkley to continue increasing revenue.

Corporations' heightened focus on risk management, due to rising threats from climate change, supply chain disruptions, and cyber risks, is supporting disciplined underwriting and pricing power, evident in healthy combined ratios and a robust rate environment that should support further net margin expansion.

The fair value story rests on a precise mix of steady revenue assumptions, firmer profit margins, and an earnings multiple that edges above the wider insurance pack. Want to see exactly how those moving parts come together and which inputs carry the most weight in that $68.33 figure? The full narrative lays out the playbook in detail.

Result: Fair Value of $68.33 (UNDERVALUED)

However, there is still real risk that softer commercial and reinsurance pricing, together with rising loss costs, could squeeze margins and challenge today’s earnings assumptions.

Another Angle on Valuation

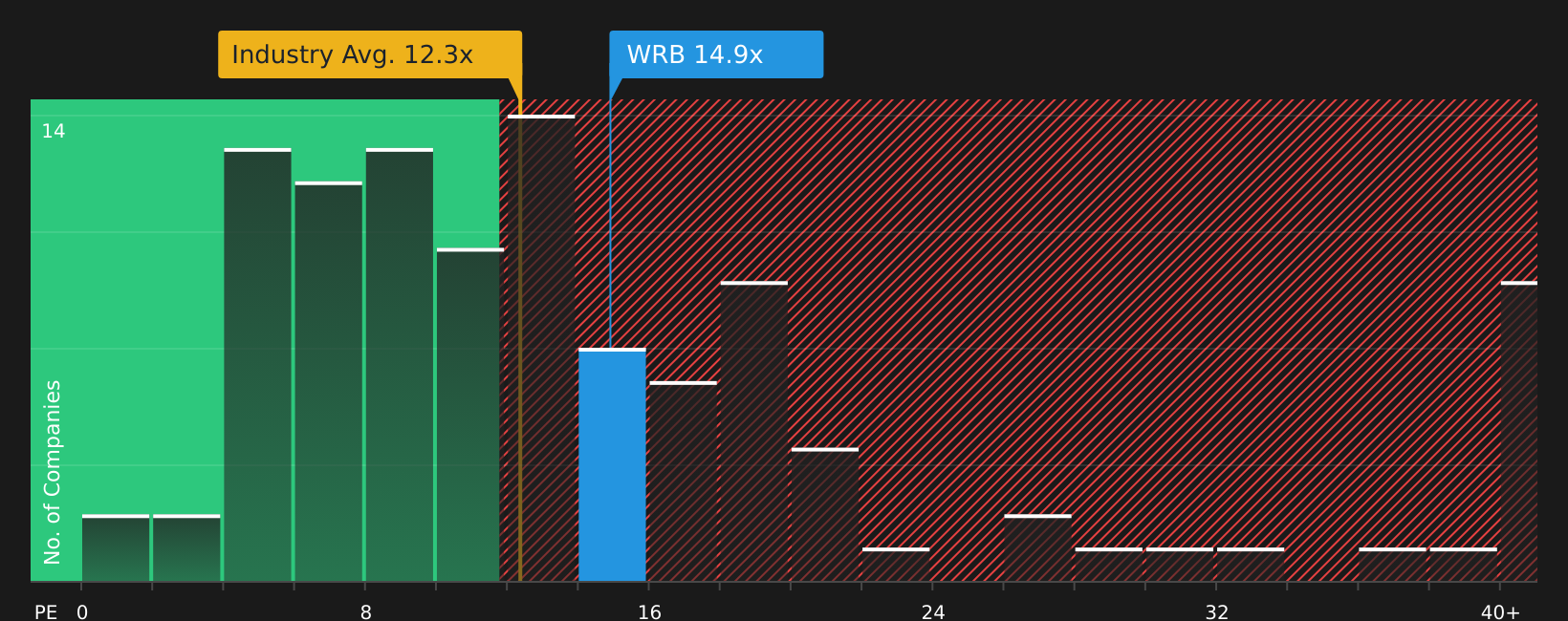

There is a twist when you look at W. R. Berkley through its current P/E. The stock trades at 13.1x earnings, which is higher than the 11.5x US Insurance average, the 11x peer average, and the 11.3x fair ratio that the market could move towards. That gap hints at valuation risk if sentiment cools, so the question is whether the earnings profile is strong enough for you to stay comfortable paying a premium.

Next Steps

Balanced story or mixed signals? With both risks and rewards on the table, now is a good time to review the data and decide where you stand.

Looking for more investment ideas?

Once you have a view on W. R. Berkley, do not stop there. Casting a wider net can surface stocks that better match your goals and risk comfort.

- Target potential mispricing by scanning 44 high quality undervalued stocks that pair solid fundamentals with room for the market to reassess their price tags.

- Lock in income ideas by reviewing 12 dividend fortresses that combine higher yields with a focus on durability.

- Prioritise resilience by checking 74 resilient stocks with low risk scores designed to highlight companies with more defensive profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.