A Look At Warner Music Group (WMG) Valuation After Hannah Karp Joins As Communications Chief

Warner Music Group WMG | 26.11 | +1.36% |

Why Hannah Karp’s Appointment Matters for Warner Music Group Stock

Warner Music Group (WMG) has put investor attention on its leadership bench by appointing longtime Billboard editor in chief Hannah Karp as executive vice president and chief communications officer.

Karp will lead global communications and brand marketing across Warner Music Group’s recorded music and publishing businesses, while also overseeing internal messaging, philanthropic initiatives, and special events that shape how the company presents itself to artists, partners, and investors.

At a share price of US$30.32, Warner Music Group has seen a 1 day share price return of 1.57%, while its 90 day share price return of a 6.19% decline contrasts with a 1 year total shareholder return of 4.24%. This suggests modest long term gains despite recent weaker momentum.

If Hannah Karp’s move has you thinking more broadly about where capital is heading in media and entertainment, it may be worth scanning fast growing stocks with high insider ownership as a way to spot other stories taking shape in the market.

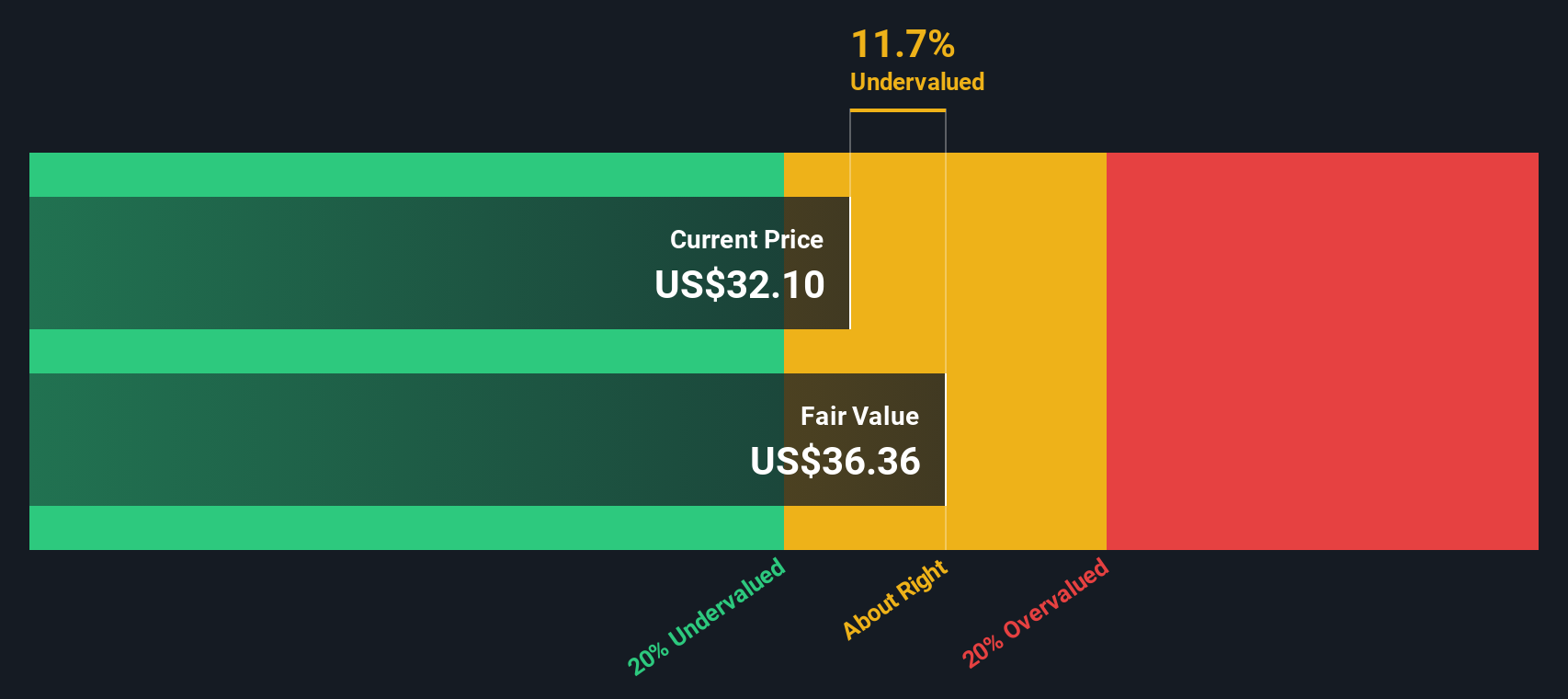

With Warner Music Group shares roughly flat over the past year but trading below some analyst price targets and an indicated intrinsic value, the key question is whether this represents a potential opportunity or whether the market already reflects future growth.

Most Popular Narrative: 19.7% Undervalued

At $30.32, the most followed narrative on Warner Music Group pegs fair value close to $37.78, which puts that story meaningfully ahead of the current price.

Early adoption of AI driven analytics and digital marketing tools (e.g., WMG Pulse), combined with an always on approach to both new releases and catalog marketing, allows Warner to optimize audience targeting and catalog performance, which is expected to drive both scalable revenue growth and operating leverage.

Curious what kind of revenue mix and margin shift sits behind that fair value, and how much earnings power this narrative is baking in? The answers are all in the full set of assumptions that link streaming growth, catalog deals and future profit multiples into one price target.

Result: Fair Value of $37.78 (UNDERVALUED)

However, this story can unravel quickly if heavy A&R spending continues to limit free cash flow or if revenue remains concentrated in a small pool of superstar artists.

Another Angle on Valuation

Our DCF model suggests Warner Music Group is trading at about an 18.9% discount to an estimated fair value of roughly $37.38, which also points to undervaluation. When both a narrative based model and a cash flow model lean the same way, do you treat that as conviction or crowding?

Build Your Own Warner Music Group Narrative

If you look at the numbers and reach a different conclusion, or just prefer your own work, you can build a custom thesis in minutes: Do it your way.

A great starting point for your Warner Music Group research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Warner Music Group is on your radar, do not stop there. The next smart move is to widen your net and see what the screener turns up.

- Spot income ideas with potential staying power by scanning these 13 dividend stocks with yields > 3% that may suit a portfolio focused on regular payouts.

- Zero in on future facing themes by checking out these 23 AI penny stocks that tie real businesses to the growth of artificial intelligence.

- Stay open to mispriced opportunities by reviewing these 872 undervalued stocks based on cash flows that could line up with your risk tolerance and time horizon.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.