A Look At Warrior Met Coal (HCC) Valuation As Blue Creek Mine Completion Expands Capacity

Warrior Met Coal, Inc. HCC | 94.89 | +3.25% |

Warrior Met Coal (HCC) just marked a major milestone by celebrating completion of its Blue Creek Mine after a roughly US$1b investment that materially expands metallurgical coal capacity and supporting logistics infrastructure in Alabama.

The Blue Creek Mine milestone comes after a strong run in Warrior Met Coal’s shares, with a 90 day share price return of 49.06% and a 1 year total shareholder return of 87.35%, suggesting momentum has been building recently rather than fading.

If this kind of project backed growth story has your attention, it could be a good moment to widen your watchlist. You may wish to consider aerospace and defense stocks as another pocket of the market to investigate.

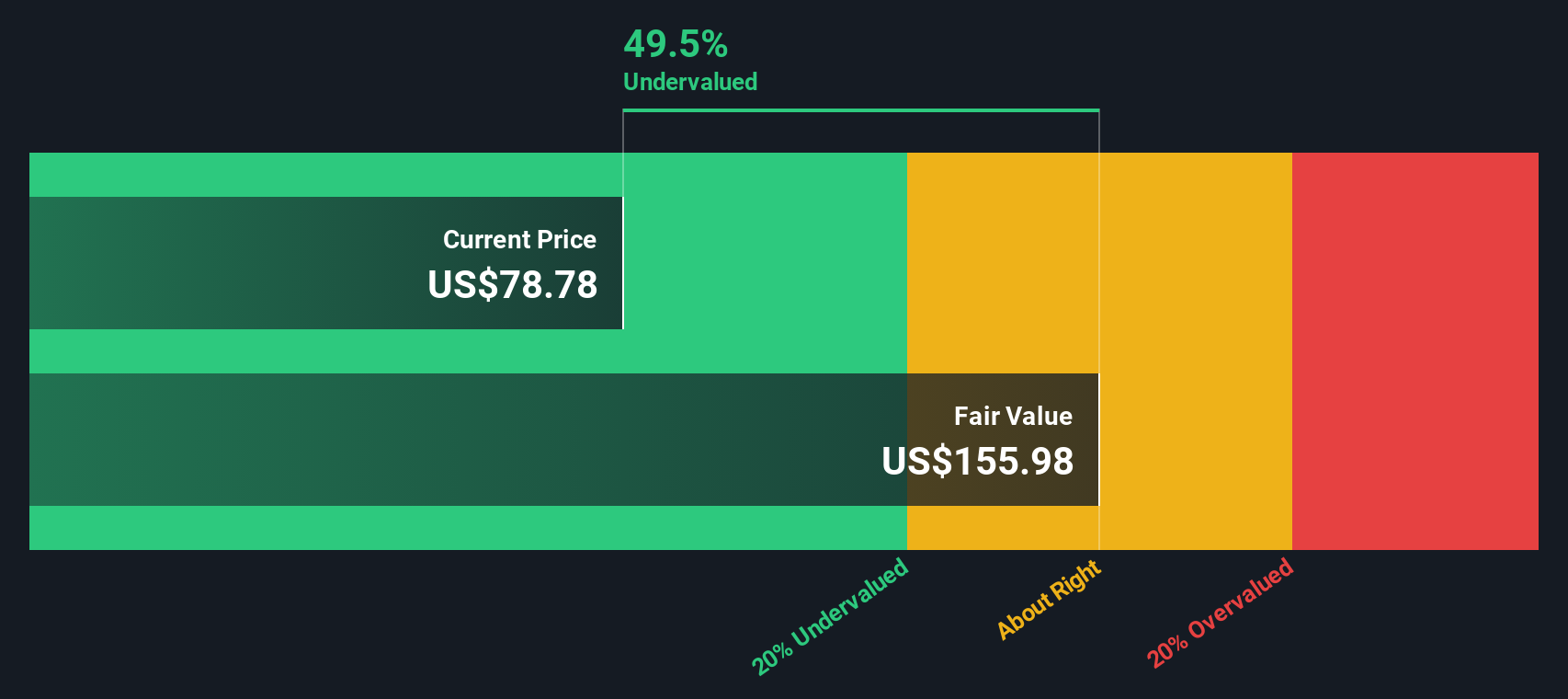

With Warrior Met Coal trading at US$100.20 against an average analyst price target of US$89.17, yet showing an estimated 41% intrinsic value gap, investors face a key question: is there still an opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 24% Overvalued

Compared with the last close of US$100.20, the most followed narrative pegs Warrior Met Coal’s fair value closer to US$80.83, creating a valuation tension investors will want to understand.

The analysts have a consensus price target of $65.667 for Warrior Met Coal based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $75.0, and the most bearish reporting a price target of just $55.0.

Curious what kind of revenue ramp, margin rebuild, and low single digit P/E multiple need to line up to support that valuation gap? The full narrative spells it out.

Result: Fair Value of $80.83 (OVERVALUED)

However, this depends on global steel demand and coal pricing not weakening further, and on Blue Creek scaling up without cost overruns or difficulty placing additional volume.

Another View: Big Discount On Our Numbers

Analysts looking at recent earnings and margins see Warrior Met Coal as about 24% overvalued around US$100.20, with fair value closer to US$80.83. Our DCF model lands in a very different place, with shares trading roughly 40.7% below an estimated fair value of US$169.05.

This kind of gap raises a practical question for you as an investor: which set of assumptions do you trust more, the near term analyst view or the longer term cash flow story?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Warrior Met Coal for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 878 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Warrior Met Coal Narrative

If you are not fully on board with these numbers or prefer to stress test the assumptions yourself, you can build a custom view in minutes with Do it your way.

A great starting point for your Warrior Met Coal research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Warrior Met Coal is already on your radar, do not stop there. Use the Simply Wall St Screener to uncover more focused ideas built around numbers, not hype.

- Target potential names with higher return profiles by scanning these 3535 penny stocks with strong financials that already show stronger balance sheets and quality metrics than many expect from this corner of the market.

- Explore the momentum in automation and data by checking these 26 AI penny stocks that are aligned with revenue opportunities in artificial intelligence, not just buzzwords.

- Look for potentially mispriced opportunities through these 878 undervalued stocks based on cash flows that highlight gaps between market prices and cash flow based assessments across a wide range of sectors.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.