A Look At Webull (BULL) Valuation As Shares Trade Well Below Narrative Fair Value

Bull Run Corp BULL | 0.00 |

Webull (BULL) has caught investor attention after recent trading, with the stock closing at US$6.33 and showing mixed performance across different periods, including a decline over the past month and a gain over the past 3 months.

Looking beyond the latest move to US$6.33, Webull’s share price return is down 22.71% year to date and the 1 year total shareholder return is down 49.12%, indicating momentum has been weak despite an 8.95% 3 month share price gain.

If you are comparing Webull with other opportunities in fast growing finance and trading platforms, it can help to widen the lens and review 21 top founder-led companies

With the stock trading at US$6.33 against a US$12.00 analyst target and an indicated intrinsic discount of 76.50%, investors now face a key question: is Webull undervalued, or is the market already pricing in future growth?

Most Popular Narrative: 47.2% Undervalued

At a last close of $6.33 versus a narrative fair value of $12.00, Webull is framed as materially undervalued, with that gap resting on aggressive growth and margin assumptions.

The successful launch and acceleration of subscription-based offerings such as Webull Premium and paid analytics products are already exceeding targets, combining higher daily trading activity and increased average revenue per user (ARPU) to boost net margins and recurring revenue stability.

Want to see what kind of revenue ramp, margin shift, and future earnings multiple support that $12.00 fair value? The narrative spells out a bold growth path, built on faster top line expansion, a swing into profitability, and a premium valuation multiple that assumes Webull can earn a place alongside higher growth capital markets platforms.

Result: Fair Value of $12.00 (UNDERVALUED)

However, that upbeat story can still be knocked off course if retail trading activity cools, or if tighter global rules slow Webull’s crypto and international expansion.

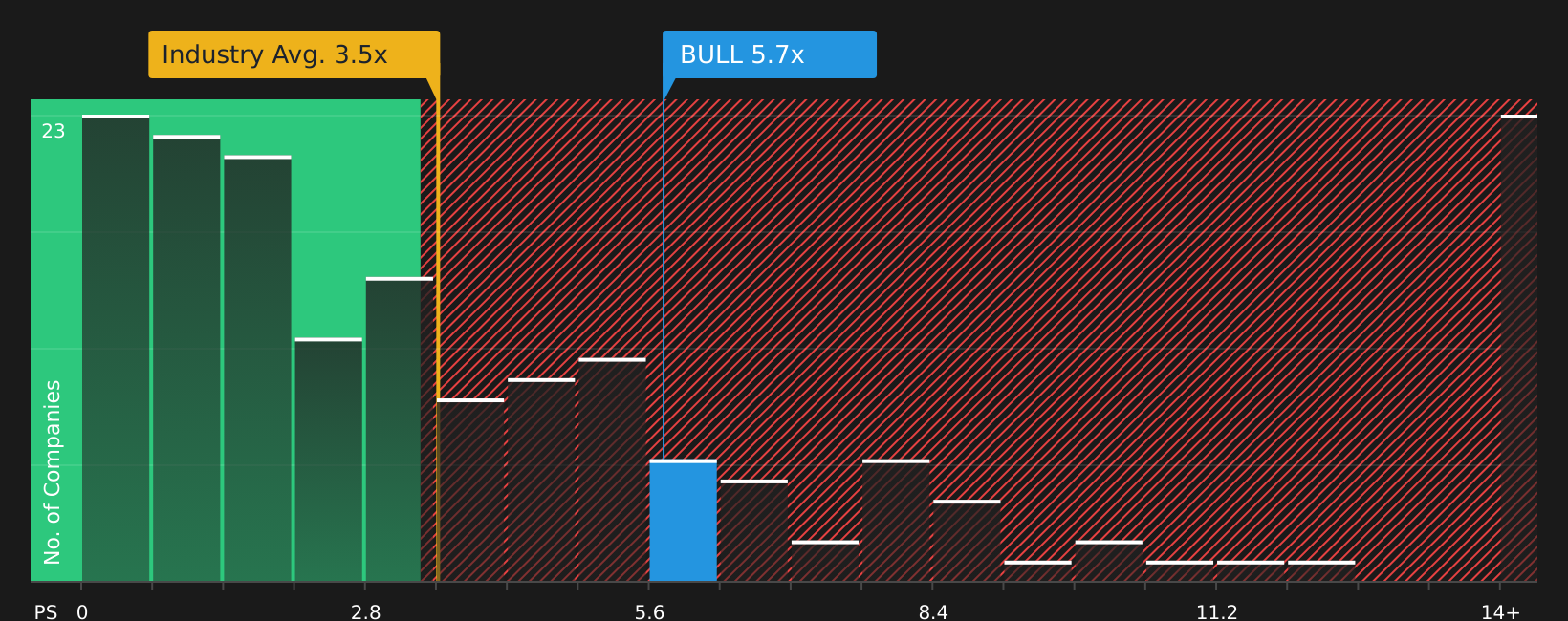

Another Take: Price-To-Sales Paints a Tougher Picture

The narrative fair value of $12.00 points to upside, but the current P/S of 5.7x is far richer than the US Capital Markets industry at 3.5x, the peer average at 1x, and even the 3.3x fair ratio. This signals real valuation risk if sentiment tightens.

Next Steps

With sentiment clearly split between valuation upside and real risks, it makes sense to check the numbers yourself and decide where you stand. To balance the cautious and optimistic views, take a closer look at the 3 key rewards and 1 important warning sign

Looking for more investment ideas?

If Webull does not quite fit your plan, broaden your watchlist with other stocks that match the kind of risk and return profile you prefer.

- Target potential value opportunities by scanning 46 high quality undervalued stocks that combine quality fundamentals with pricing that may not fully reflect their underlying businesses.

- Prioritize resilience by reviewing 64 resilient stocks with low risk scores where balance sheets and risk scores point to companies built to handle tougher conditions.

- Spot future standouts early by using the screener containing 22 high quality undiscovered gems before attention and pricing fully catch up.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.