A Look At West Pharmaceutical Services (WST) Valuation After Recent Share Price Consolidation

West Pharmaceutical Services, Inc. WST | 0.00 |

Event Overview and Recent Stock Moves

West Pharmaceutical Services (WST) has drawn fresh attention after recent trading, with the stock closing at US$314.50. Short term performance has been mixed, with a 0.9% daily decline and a 2.6% slide over the past week.

While the 1 day share price return is down 0.9% and the 7 day share price return is down 2.6%, the 90 day share price return of 27.9% and 1 year total shareholder return of 40.4% point to momentum that has cooled slightly in the very short term but remains strong over a longer window.

If this kind of move has you rethinking your watchlist, it can be useful to compare West Pharmaceutical Services with other healthcare focused opportunities using our screener for 39 healthcare AI stocks

With West Pharmaceutical Services trading at US$314.50, a 40.4% 1 year total return and a reported intrinsic value premium, the key question is whether the recent strength leaves upside on the table, or if the market is already pricing in future growth.

Price-to-Earnings of 40.9x: Is it justified?

West Pharmaceutical Services is trading on a P/E of 40.9x, which sits above several benchmarks and signals that the stock is priced for relatively strong earnings.

The P/E ratio compares the current share price to the company’s earnings per share, so a higher P/E usually reflects higher expectations for future profits or a willingness to pay more for each dollar of current earnings.

In this case, analysts are forecasting earnings growth of 10.16% per year, with recent earnings up 16.2% over the past year and net profit margins at 16.8%, slightly higher than last year’s 16.1%. The market may be assigning a premium because earnings growth over the past year has also outpaced the Life Sciences industry, which recorded 5.2%.

That premium stands out when you line it up against other yardsticks. The current 40.9x P/E is higher than the global Life Sciences industry average of 35.1x and slightly ahead of the peer average of 39.3x. It is also well above the estimated fair P/E of 21.2x. This level indicates where the market could potentially shift if sentiment or growth expectations cool.

Result: Price-to-Earnings of 40.9x (OVERVALUED)

However, there are pressure points, including a P/E that sits well above the estimated fair level and a 3 year total return that is down 8.9%.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Another View: Cash Flows Paint a Different Picture

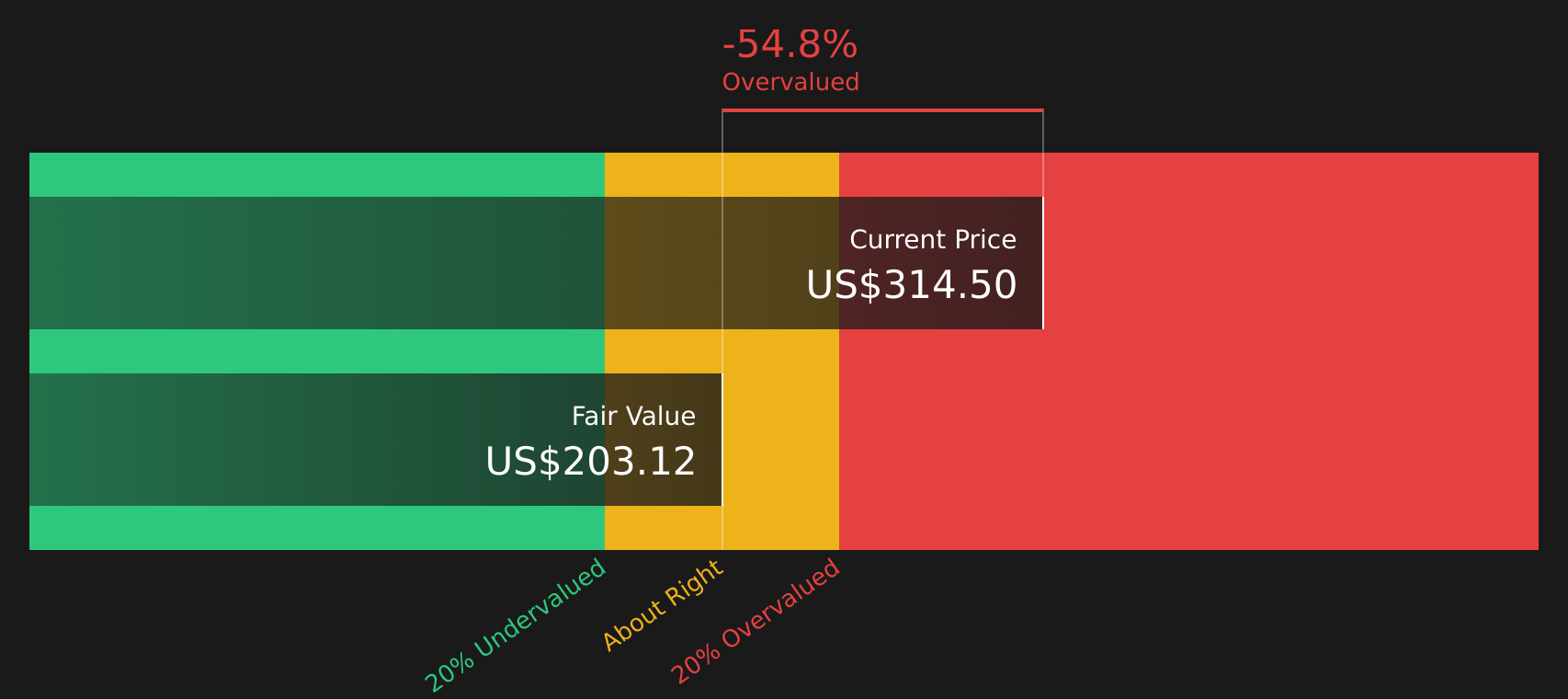

That rich 40.9x P/E already suggested West Pharmaceutical Services is priced generously, but our DCF model goes further. On this view, the stock at $314.50 sits above an estimated future cash flow value of $202.45, pointing to an overvalued reading rather than untapped upside.

For you as an investor, that gap raises a practical question: Is the market fairly rewarding West Pharmaceutical Services for its quality earnings profile and 16.2% recent earnings growth, or leaning too hard into optimism compared with what the cash flow math supports?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out West Pharmaceutical Services for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 49 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If the mixed signals in this valuation feel a bit conflicting, that is a cue to move quickly and test the numbers yourself against your own expectations, then weigh them up against the 2 key rewards

Looking for more investment ideas?

Once you are done assessing West Pharmaceutical Services, do not stop there. Broaden your watchlist with other focused stock ideas tailored to different investing styles.

- Target resilient cash generators by scanning companies with strong fundamentals using the solid balance sheet and fundamentals stocks screener (46 results).

- Hunt for potential mispricing by checking stocks flagged as 49 high quality undervalued stocks before others catch on.

- Look for a stream of income ideas by reviewing companies in the 9 dividend fortresses while yields and balance sheets still appear appealing.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.