A Look At WisdomTree (WT) Valuation After Record AUM Strong Q1 Results And Atlantic House Acquisition

WisdomTree Investments Inc WT | 0.00 |

WisdomTree (WT) is in focus after reporting first quarter 2026 results that included record assets under management, higher quarterly revenue, a completed Atlantic House acquisition, and fresh progress in tokenized products and partnerships.

At a share price of $16.62, WisdomTree has seen strong momentum build recently, with a 30 day share price return of 15.02% and a year to date share price return of 32.85%. The 1 year total shareholder return of 83.82% and 3 year total shareholder return of 164.10% point to sustained interest around its record AUM, Atlantic House acquisition and tokenization efforts.

If this kind of business model shift has your attention, it can be a good moment to widen your search and check out our screener of 25 cryptocurrency and blockchain stocks

With record AUM, a growing digital asset platform, the Atlantic House acquisition and a share price that already reflects strong recent returns, the key question is whether WT is still mispriced or if the market is already banking on further growth.

Most Popular Narrative: 11.7% Undervalued

Against the current share price of $16.62, the widely followed narrative points to a fair value of $18.82, built on detailed revenue and earnings forecasts.

The acquisition of Ceres Partners positions WisdomTree to capitalize on growing investor demand for private market and alternative asset exposures, particularly in underpenetrated, income-generating sectors like U.S. farmland, supporting future AUM and fee revenue growth.

WisdomTree's early investments in blockchain, tokenization, and stablecoin-powered digital asset infrastructure are enabling new product and revenue streams (such as tokenized funds and scalable net interest income), aligning them with the expanding adoption of digital finance, which is likely to boost both top line and margin expansion.

Curious what sits behind that $18.82 fair value and 8.7% discount rate assumption? The narrative leans on faster revenue expansion, higher margins and a lower future earnings multiple than many would expect. The full story connects these moving parts into one valuation case.

Result: Fair Value of $18.82 (UNDERVALUED)

However, this depends on analysts being correct about tokenization and digital assets gaining traction, as well as fee compression not eroding ETF and model portfolio economics.

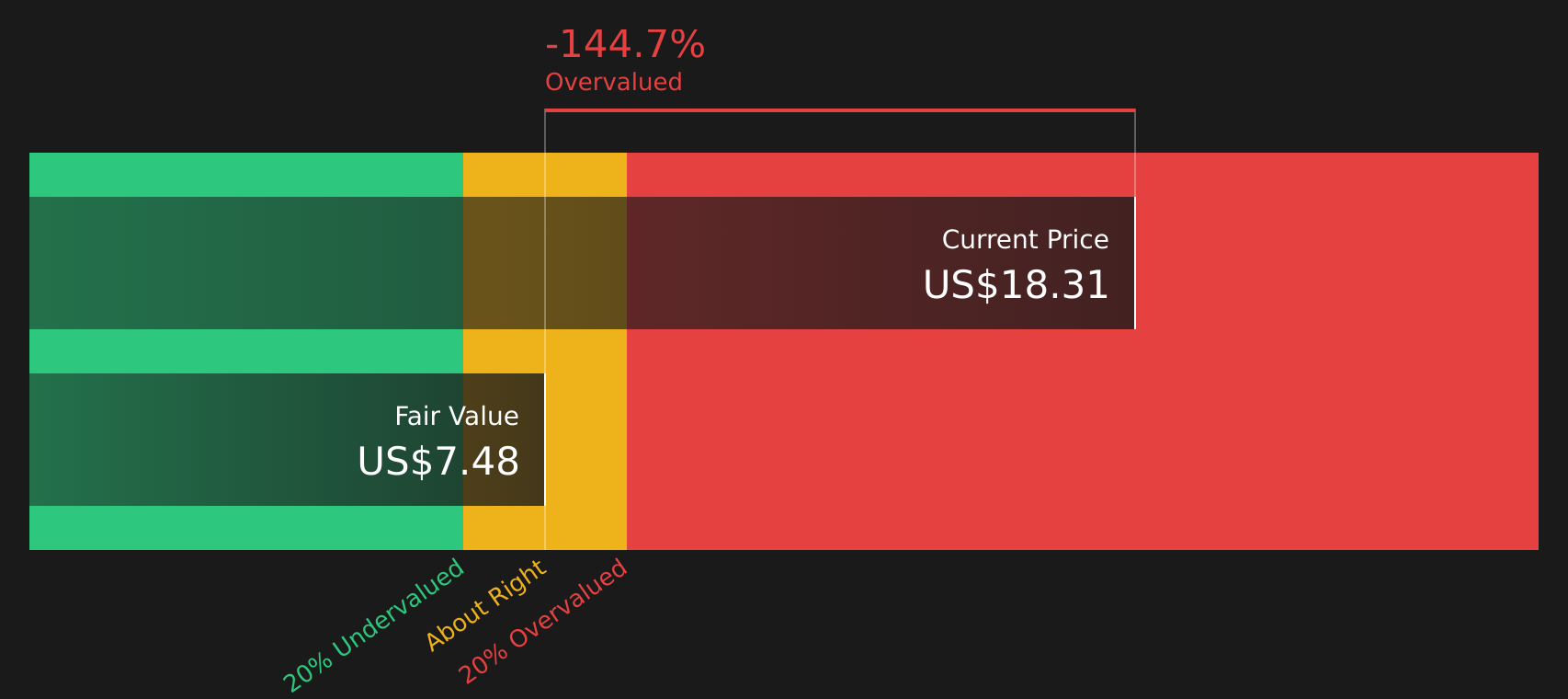

Another Angle: Cash Flow Model Paints A Tougher Picture

The popular narrative has WisdomTree at an $18.82 fair value, but the Simply Wall St DCF model points in a different direction. On that cash flow view, WT at $16.62 is trading well above an estimated value of $7.44, which frames the stock as overvalued instead of undervalued.

Put simply, the market price is closer to analyst earnings forecasts than to our DCF cash flow assumptions. This raises a practical question for you as an investor: which story do you trust more, the earnings trajectory or the underlying cash generation.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out WisdomTree for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 50 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Mixed messages in the data so far? Make time to review the numbers for yourself, weigh both sides, and see the full picture with 3 key rewards and 1 important warning sign

Ready for more investment ideas?

If WT has sharpened your thinking, do not stop here; broaden your radar now with a few focused stock ideas built from the Simply Wall St screener.

- Target quality at a discount by scanning companies that look attractively priced relative to their fundamentals with the 50 high quality undervalued stocks.

- Strengthen your income stream by finding companies with higher yields that aim to combine consistent payouts with resilient business models using the 13 dividend fortresses.

- Prioritize resilience by focusing on companies that pair lower risk scores with sturdier balance sheets through the 69 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.