A Look At Wynn Resorts (WYNN) Valuation After Strong Q1 2026 Results And Macau Expansion Plans

Wynn Resorts, Limited WYNN | 0.00 |

Earnings jump and Macau expansion plan put Wynn Resorts (WYNN) in focus

Wynn Resorts (WYNN) is back on investors' radar after reporting higher first quarter 2026 revenue and net income than a year earlier, alongside a new expansion project at Wynn Palace in Macau.

The company posted first quarter sales of US$1,467.61 million and total revenue of US$1,856.76 million, compared with US$1,314.95 million and US$1,700.40 million respectively in the prior year period. Net income came in at US$120.45 million versus US$72.75 million a year ago.

Basic earnings per share from continuing operations were reported at US$1.17 compared with US$0.69 a year earlier, while diluted earnings per share from continuing operations were US$1.04 versus US$0.69.

Alongside the earnings update, Wynn Resorts confirmed a quarterly dividend of US$0.25 per share, payable on May 29, 2026, with an ex dividend and record date of May 18, 2026.

Management also highlighted a planned US$900 million to US$950 million investment in The Enclave, a new all suite hotel tower at Wynn Palace in Macau. This project is expected to increase room capacity by 25% and suite count by 50%. It sits alongside ongoing work on the Wynn Al Marjan resort in the UAE, which faces some logistical and geopolitical related delays and is now expected to open in 2027.

For context, Wynn Resorts generated total revenue of US$7,137.924 million and net income of US$327.334 million over its most recent full year, with operations spanning Las Vegas, Macau and Encore Boston Harbor.

Wynn Resorts' latest earnings beat and new Macau investment come as the stock trades at US$106.85, with a 30 day share price return of 6.39% but a 90 day share price return of 9.42%. Over the longer term, the 1 year total shareholder return of 24.53% contrasts with a 5 year total shareholder return of 10.01%, suggesting recent momentum is stronger than the longer run record.

If this kind of recovery story has your attention, it can be useful to see what else is moving in the casino and leisure space, including 18 top founder-led companies

With Wynn delivering stronger Q1 numbers, fresh Macau expansion plans and the stock sitting at US$106.85, the key question is whether recent gains leave upside on the table or if the market is already pricing in future growth.

Most Popular Narrative: 24% Undervalued

At a last close of $106.85 versus a narrative fair value of $140.61, the current price sits well below what the most followed storyline implies, and that gap rests on very specific views about future growth and cash generation.

The imminent launch of Wynn Al Marjan Island, with first mover advantage and limited near term competition in a potentially multi billion dollar new market, is a major forward catalyst that is currently underappreciated by investors and could drive a meaningful step change in both consolidated revenue and EBITDAR.

Curious what earnings path supports that higher fair value, and how margin expansion plus a richer future P/E multiple fit together to justify it.

Result: Fair Value of $140.61 (UNDERVALUED)

However, this depends on Macau remaining resilient and on large projects like Wynn Al Marjan Island performing as expected, because weaker regional demand or lower returns could quickly erode that upside story.

Another Angle on Wynn's Valuation

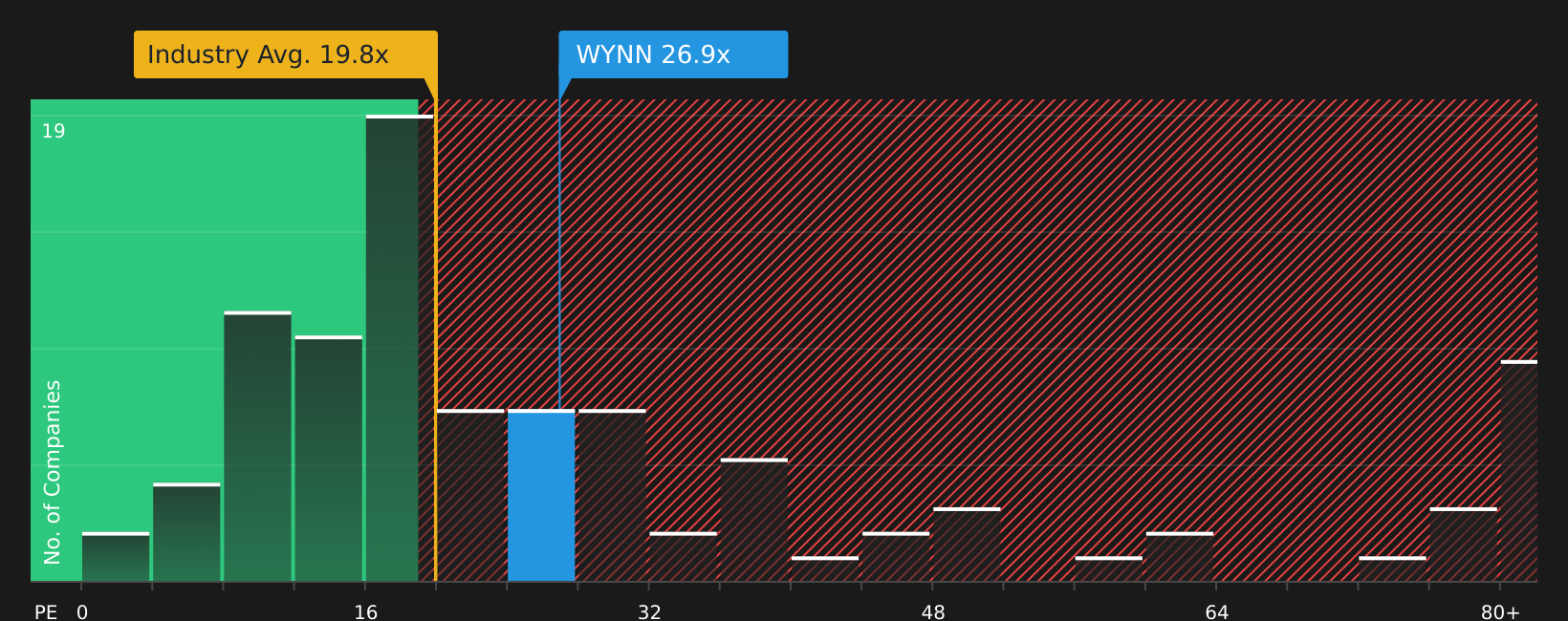

The popular narrative points to a fair value of $140.61. However, Wynn trades on a P/E of 33.5x versus a fair ratio of 30.3x and a US Hospitality average of 20.6x, so investors are already paying a clear premium. The key consideration is whether that premium still feels comfortable to you.

Next Steps

After all this, do you feel the story is leaning too positive or too cautious? Are you ready to act quickly and test the data yourself with 2 key rewards and 3 important warning signs

Ready to find your next idea?

If Wynn has sharpened your appetite for opportunities, do not stop here. Use the Simply Wall St screener to broaden your watchlist before the crowd catches on.

- Target stability first by checking out companies in the 72 resilient stocks with low risk scores that aim to keep risk scores on the lower side.

- Hunt for quality at a reasonable price with the 51 high quality undervalued stocks that focuses on strong businesses trading below their assessed value.

- Spot resilient cash generators and potential compounding machines using the solid balance sheet and fundamentals stocks screener (44 results) that highlights stocks with sturdier financial footing.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.