A Look At Yeti Holdings (YETI) Valuation As Analysts Lift Price Targets Without New Company Developments

YETI Holdings YETI | 36.36 | -1.97% |

Recent analyst updates on YETI Holdings (YETI), with several firms reaffirming Buy or Neutral views while lifting their valuation assumptions, have pushed the stock further onto investors’ radar despite a lack of new company specific headlines.

The current share price of US$50.77 follows a 90 day share price return of 50.47% and a 1 year total shareholder return of 36.11%, suggesting momentum has been building over both shorter and longer horizons.

If YETI’s recent run has you thinking about where else growth stories might emerge, this could be a good moment to check out fast growing stocks with high insider ownership.

With the share price now at US$50.77 and trading above the average analyst target of about US$43.57, the key question is whether YETI is still undervalued or if the market is already pricing in future growth.

Most Popular Narrative: 22.5% Overvalued

Compared with the fair value estimate of US$41.43 from the most followed narrative, YETI’s last close at US$50.77 sits well above that level. This puts the current rally against a more cautious valuation backdrop that relies on steady earnings progress rather than aggressive growth.

The analysts have a consensus price target of $36.533 for YETI Holdings based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $53.0, and the most bearish reporting a price target of just $32.0.

Curious what justifies paying above that fair value line? The narrative leans on measured revenue growth, slightly higher margins, and a lower future earnings multiple than many leisure peers. The full story sits in the detailed assumptions behind those numbers.

Result: Fair Value of $41.43 (OVERVALUED)

However, this depends on drinkware demand stabilising and competitors easing up on promotions, and both could easily move the story in the opposite direction.

Another View: DCF Points the Other Way

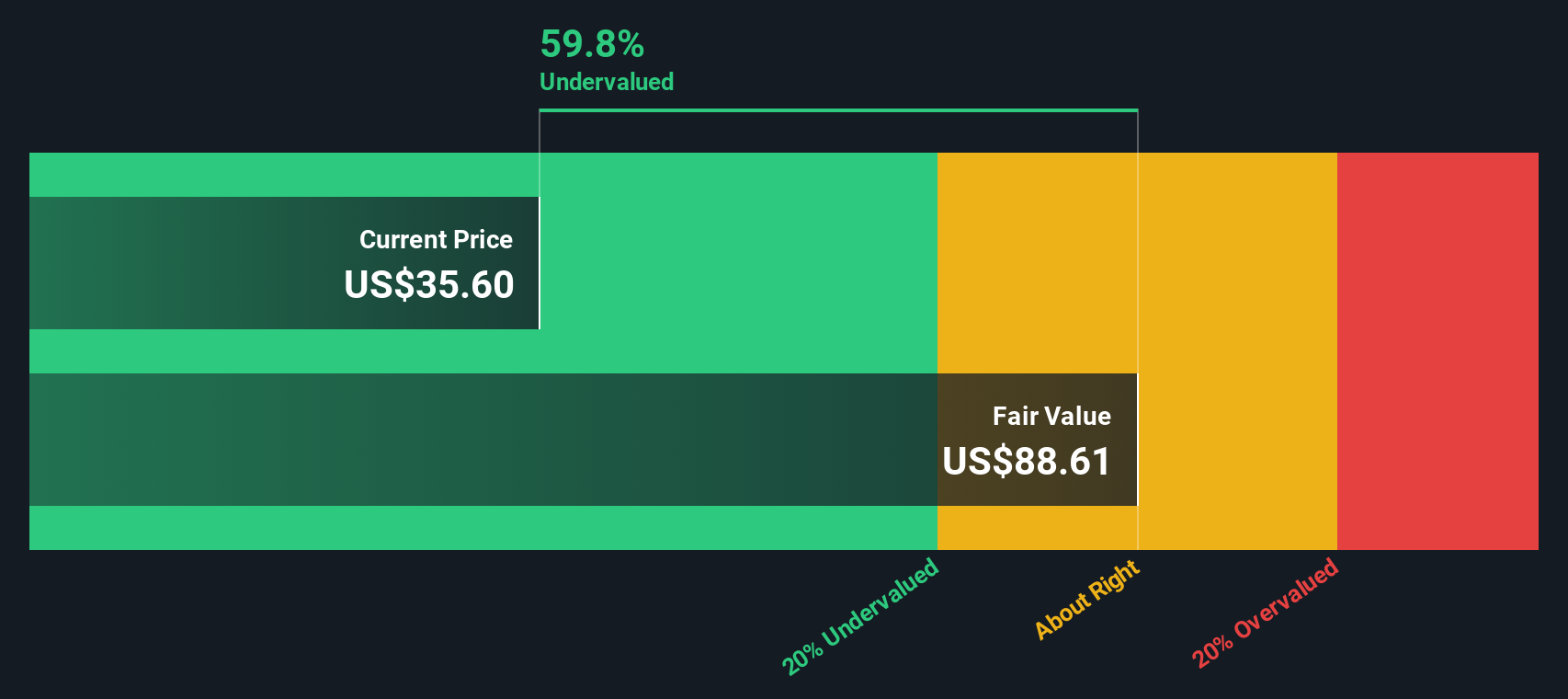

The first narrative and analyst targets frame YETI as 22.5% overvalued around US$41.43 per share. Our DCF model tells a very different story, with a fair value estimate of US$93.95, which is about 46% above the current US$50.77 price. When two methods disagree this much, which one do you trust more?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out YETI Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 863 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own YETI Holdings Narrative

If you are not fully on board with these views or you would rather test the numbers yourself, you can build your own narrative in just a few minutes, starting with Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding YETI Holdings.

Looking for more investment ideas?

If YETI has caught your attention, do not stop there. Broaden your watchlist with a few focused stock ideas that could help inform your next move.

- Target reliable income potential by checking out these 12 dividend stocks with yields > 3% that might suit a portfolio built around regular cash returns.

- Spot potential mispricings early by scanning these 863 undervalued stocks based on cash flows where market expectations and cash flow profiles do not fully line up.

- Position yourself for the next wave of technology by reviewing these 24 AI penny stocks that are tied to real business models, not just headlines.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.