A Look At ZIM Integrated Shipping Services (ZIM) Valuation As Short Interest Declines And Sentiment Shifts

ZIM Integrated Shipping Services Ltd. ZIM | 26.30 | +1.35% |

Why ZIM’s Short Interest Shift Matters Now

A sharp shift in sentiment is hitting ZIM Integrated Shipping Services (ZIM), with short interest as a share of float falling 14.99%, even though 15.54% of shares remain sold short.

At a share price of $22.06, ZIM has recently seen a 60.79% 90 day share price return and a very large 5 year total shareholder return of about 7x, suggesting momentum that aligns with falling short interest and shifting views on risk and growth potential.

If this kind of sharp sentiment swing has your attention, it may be a good moment to broaden your watchlist and check out fast growing stocks with high insider ownership.

Short interest is easing, the share price has surged and models suggest roughly a 40% intrinsic discount. Yet the last analyst target sits below today’s US$22.06 level, so is there real value here or is the market already pricing in the next leg of growth?

Most Popular Narrative: 95.1% Undervalued

According to one widely followed narrative, ZIM Integrated Shipping Services could justify a fair value far above the last close of $22.06, framing the current price as a steep discount.

Largest uncertainty for the CORE INDONESIA ZIM INT. revenue is the Panama Canal bottleneck. PBR stock is down similarly (Brazil). This risk is quickly becoming a much overstated narrative. There are only 220 million shares, which is why ZIM has sustainable total returns. While not a big cap stock, there is no risk at all from general economic international stagflation because of 19% lower average strength of the USA currency relative to others, which was ten percent higher under Joe Biden. High flyer, high PE big caps can range from 1 billion to a hundred billions of outstanding shares. News (not old news), Apr 5, 2025, Gatun Lake has reached historic highs with ample rainfall.

Want to see how a high margin profile, aggressive revenue assumptions and a compact share count combine into that fair value estimate? The valuation hinges on bold growth, firm profitability and a future earnings multiple more often linked with fast growing names. Curious which specific inputs are doing the heavy lifting in that $452.35 figure? The full narrative lays out every step behind that call.

Result: Fair Value of $452.35 (UNDERVALUED)

However, that bullish setup still leans on optimistic revenue growth assumptions and a future P/E that may not hold if shipping demand or pricing weakens.

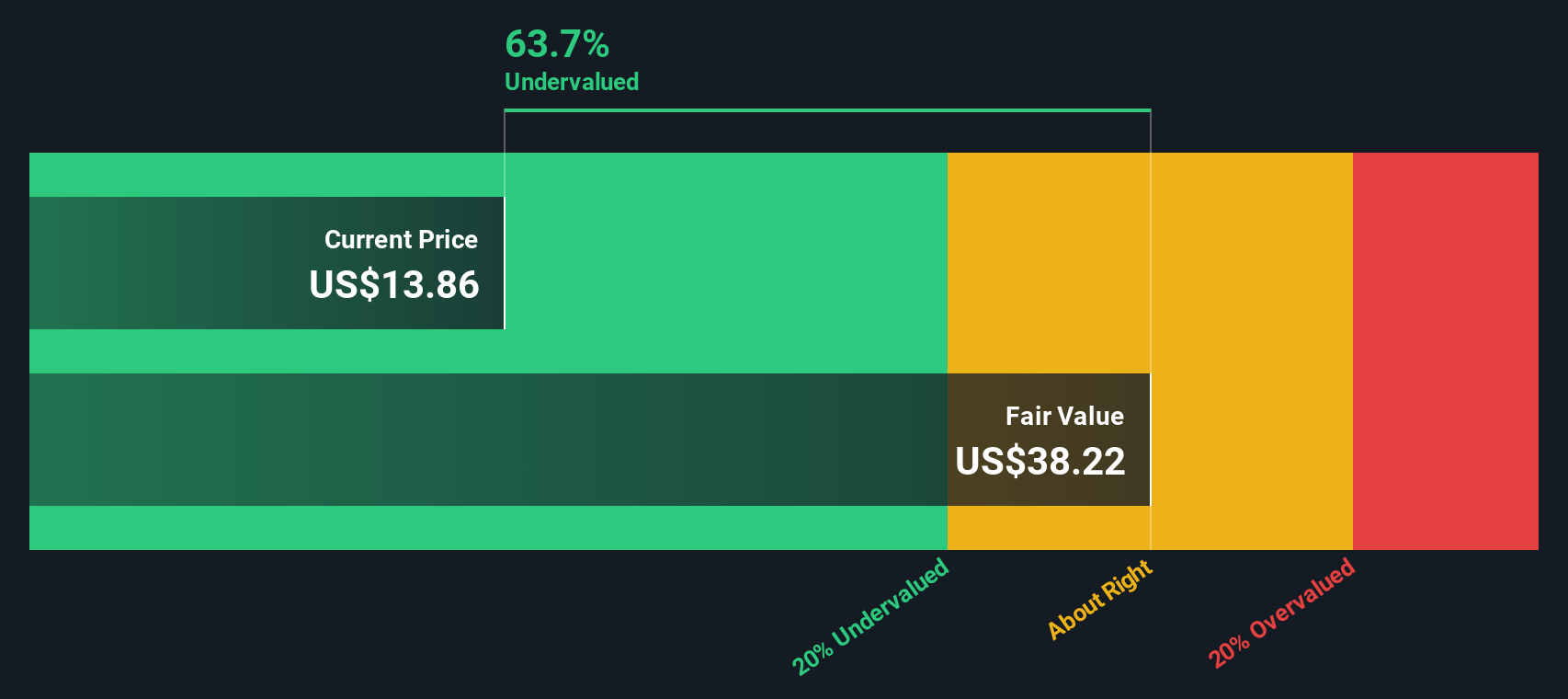

Another Angle On Value

That $452.35 fair value hinges on very bullish growth and profitability. Our DCF model lands in a very different place, with ZIM at $22.06 trading about 39.7% below an estimated future cash flow value of $36.56, which still points to undervaluation but on a far more modest scale. Which story seems closer to what you think is realistic?

Build Your Own ZIM Integrated Shipping Services Narrative

If you see the numbers differently or prefer to test your own assumptions, you can build a personalised ZIM view in just a few minutes, starting with Do it your way.

A great starting point for your ZIM Integrated Shipping Services research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If ZIM has sharpened your focus, do not stop here, you might miss other opportunities that fit your style just as well or even better.

- Spot potential bargains early by scanning these 3522 penny stocks with strong financials that pair low share prices with stronger financial foundations than you might expect.

- Ride the AI wave in a more focused way by checking out these 24 AI penny stocks leading real projects in automation, data analysis and machine learning.

- Target income first by zeroing in on these 12 dividend stocks with yields > 3% that already offer yields above 3% and can help anchor a returns focused portfolio.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.